Abstract

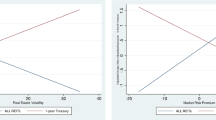

Yield spreads between mortgage pass-through and U.S. Treasury securities may reflect differences in taxation, phenomena affecting relative supply and demand, and compensation for default, call, and marketability risks on mortgage instruments. Our research empirically models differences in yields between pass-throughs and comparable-maturity Treasuries. We find that interest-rate volatility and the term structure of rates, factors often cited in the mortgage pricing literature as affecting the mortgage call premium, are the primary determinants of movements in these spreads. Moreover, these effects have grown in importance in recent years as exercise of the prepayment option has increased. We also find evidence that liquidity and credit concerns affect the pricing of pass-through securities.

Similar content being viewed by others

References

Arak, Marcelle, Goodman, Laurie, and Jonson, Judith. “Predicting GNMA-Treasury Spreads.” Mortgage Banking (January1986).

Black, Deborah G., Garbade, Kenneth D., and Silber, William L. “The Impact of the GNMA Pass-Through Program on FHA Mortgage Costs”. The Journal of Finance 36(2) (May 1981).

Brennan, Michael J., and Schwartz, Eduardo S. “Determinants of GNMA Mortgage Prices.” AREUEA Journal 13(3) (Autumn1985).

Brooks, S., and Quick, P. “CHOs and Secondary Mortgage Markets.” U.S. Department of Housing and Urban Development, 1985. (Mimeo)

Cholewicki, Victor. “CMOs Transform Mortgage Credit Markets.” Mortgage Banking (February1985), 61-6.

Cook, Timothy Q., and Hendershott, Patric H. “The Impact of Taxes, Risk and Relative Security Supplies on Interest Rate Differentials.” Journal of Finance 33(4) (September1978).

Duca, John, and Rosenthal, Stuart. “An Empirical Test of Credit Rationing in the Mortgage Market.” Journal of Urban Economics (1989, forthcoming).

Edelstein, Robert, and Rosen, Kenneth. “Collateralized Mortgage Obligations: Cheaper Mortgage Money by the Slice?” Paper presented at the American Economics Association Meetings, December 1985.

Hendershott, Patric H. “Mortgage Pricing: What Have We Learned So Far?” AREUEA Journal 14(4) (Winter 1986).

Hendershott, Patric H., and Shilling, James D. “The Impact of the Agencies on Conventional Fixed-Rate Mortgage Yields.” Journal of Real Estate Finance and Economics 2(2) (June1989), 101–115.

Hendershott, Patric H., Shilling, James D., and Villani, Kevin E. “Measurement of the Spreads Between Yields on Various Mortgage Contracts and Treasury Securities.” AREUEA Journal 11(4) (Winter 1983).

Hendershott, Patric H., and Van Order, Robert. “Pricing Mortgages: An Interpretation of the Models and Results.” Journal of Financial Services Research 1(1) (1987), 19–55.

Jameson, Mel, Dewan, S., and Sirmans, C.F. “Price and Welfare Effects of Unbundling Financial Innovations: The Case of Collateralized Mortgage Obligations.” Department of Finance Working Paper #8724-89, Louisiana State University, November 1987.

Kau, James B., Keenan, Donald C, Muller, Walter J., III, et al. “Option Theory and Fixed-Rate Mortgages.” Occasional Paper No. 34, Housing, Real Estate and Urban Land Studies Program, Anderson Graduate School of Management, UCLA, June 1988.

Milonas, Nikolaos T. “The Prepayment Option in the GNMA-Treasury Bond Spread.” Housing Finance Review 6(4) (Winter1987), 261–278.

Roll, Richard. “Collateralized Mortgage Obligations: Characteristics, History, Analysis.” Goldman Sachs report, April 1986.

Villani, Kevin E. “Pricing Mortgage Credit.” In Richard Aspinwall and Robert A. Eisenbeis, eds., Handbook for Banking Strategy. New York: Wiley, 1985.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Rothberg, J.P., Nothaft, F.E. & Gabriel, S.A. On the determinants of yield spreads between mortgage pass-through and Treasury securities. J Real Estate Finan Econ 2, 301–315 (1989). https://doi.org/10.1007/BF00177950

Issue Date:

DOI: https://doi.org/10.1007/BF00177950