Abstract

This paper presents a new heuristic for generating scenarios for two-stage stochastic programs. The method uses copulas to describe the dependence between the marginal distributions, instead of the more common correlations. The heuristic is then tested on a simple portfolio-selection model, and compared to two other scenario-generation methods.

Similar content being viewed by others

Notes

For some available codes, see, for example, http://www.mathfinance.cn/tags/copula.

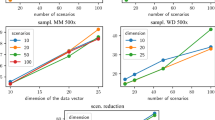

This assumes that we match all the possible pairs; more generally, we can replace \({n}^2\) by the number of matched bivariate copulas. For example, if we specify copulas only for pairs of margins \((i,j)\) with \(|i-j|\le k\), for some fixed \(k\), the heuristic becomes \({\fancyscript{O}\!\left( {n}\,{S}^2\right) }\).

Except for distributions with limited support, where such a correction might give infeasible values.

References

Bouyé E, Durrleman V, Nikeghbali A, Riboulet G, Roncalli T (2000) Copulas for finance: a reading guide and some applications. Working paper, Crédit Lyonnais, Paris, 2000. Available at SSRN: http://ssrn.com/abstract=1032533

Dupačová J, Consigli G, Wallace SW (2000) Scenarios for multistage stochastic programs. Annals Oper Res 100(1–4):25–53. doi:10.1023/A:1019206915174

Forrest J, Lougee-Heimer R (2005) CBC user guide. In: Greenberg HJ, Smith JC (eds) Tutorials in Operations research, INFORMS, chapter \(10\), pp 257–277

Høyland K, Kaut M, Wallace SW (2003) A heuristic for moment-matching scenario generation. Comput Optim Appl 24(2–3):169–185. doi:10.1023/A:1021853807313

Hu L (2006) Dependence patterns across financial markets: a mixed copula approach. Appl Financial Econ 16(10):717–729. doi:10.1080/09603100500426515

Hultberg TH (2007) FLOPC++ an algebraic modeling language embedded in C++. In: Waldmann K-H, Stocker UM (eds) Proceedings operations research, vol 2006. Springer, Heidelberg, pp 187–190. doi:10.1007/978-3-540-69995-8_31

Kaut M, Wallace SW (2007) Evaluation of scenario-generation methods for stochastic programming. Pac J Optim 3(2):257–271

Kaut M, Wallace SW (2011) Shape-based scenario generation using copulas. Comput Manag Sci 8(1–2):181–199. doi:10.1007/s10287-009-0110-y

Longin F, Solnik B (2001) Extreme correlation of international equity markets. J Finance 56(2):649–676

Makhorin A (2013a) GNU linear programming kit—reference manual, version 4.48. Free Software Foundation, Inc, Boston

Makhorin A (2013b) GNU linear programming kit—modeling language GNU mathProg, version 4.48. Free Software Foundation, Inc, Boston

Nelsen RB (1998) An introduction to copulas. Springer, New York

Patton AJ (2004) On the out-of-sample importance of skewness and asymmetric dependence for asset allocation. J Financial Econ 2(1):130–168. doi:10.1093/jjfinec/nbh006

Rockafellar RT, Uryasev S (2000) Optimization of conditional value-at-risk. J Risk 2(3):21–41

Romano C (2002) Calibrating and simulating copula functions: an application to the italian stock market. Working paper 12, Centro Interdipartimale sul Diritto e l’Economia dei Mercati

Sklar A (1996) Random variables, distribution functions, and copulas-a personal look backward and forward. In: Rüschendorff L, Schweizer B, Taylor M (eds) Distributions with fixed marginals and related topics, vol 28 of Lecture Notes—monograph, pp 1–14. Institute of Mathematical Statistics, Hayward. URL: http://www.jstor.org/stable/4355880

Vaagen H, Wallace SW (2008) Product variety arising from hedging in the fashion supply chains. Int J Prod Econ 114(2):431–455. doi:10.1016/j.ijpe.2007.11.013

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kaut, M. A copula-based heuristic for scenario generation. Comput Manag Sci 11, 503–516 (2014). https://doi.org/10.1007/s10287-013-0184-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10287-013-0184-4