Abstract

Genuine Savings has emerged as a widely-used indicator of sustainable development. This approach to conceptualising what sustainability is about has strong links to work published by Anil Markandya and colleagues over 20 years ago. In this paper, we use long-term data stretching back to 1870 to undertake empirical tests of the relationship between Genuine Savings (GS) and future well-being for three countries: Britain, the USA and Germany. Our tests are based on an underlying theoretical relationship between GS and changes in the present value of future consumption. Based on both single country and panel results, we find evidence supporting the existence of a cointegrating (long run equilibrium) relationship between GS and future well-being, and fail to reject the basic theoretical result on the relationship between these two macroeconomic variables. This provides some support for the GS measure of weak sustainability.

Similar content being viewed by others

Notes

Also referred to as Adjusted Net Savings or Comprehensive Investment.

Note that Pearce et al. (1989) use these terms rather differently: they define weak sustainability as a situation where, across a portfolio of projects and over time, the net environmental cost of implementing the portfolio is zero or negative. For strong sustainability, they require this non-positive condition to hold for every time period: see Chapter 5. It is interesting that by the time the “new blueprint” was published Barbier and Markandya (2013), the difference between weak and strong sustainability revolves around the substitutability of different forms of capital for each other. Thus, weak sustainability takes rule (1) as being the relevant rule; strong sustainability takes rule (2).

Pearce and Atkinson state: “To do this we adopt a neoclassical stance and assume the possibility of substitution between ‘natural’ and ‘man-made’ capital” (page 104).

Note that our British data goes back to 1760, but for the present paper we restrict our attention to the period from 1870 onwards, since that allows a comparison on a like-for-like basis between the three countries.

We do not include a wealth dilution term in the calculations of per capita GS in this paper.

We are not convinced that the theory makes clear what one does about new discoveries in GS accounting. Clearly, finding an oil deposit increases the known stock of reserves, although it only increases the known economic reserve if the price/cost ratio is bigger than one. However, it does not increase the finite stock in the ground. Depletion, however, clearly reduces both the known stock and the un-known stock. For all of the non-renewable resources included in the database for Germany, the USA and Britain, we use production (ie extraction) in year t as the measure of depletion in that year. Finding new resources in year t might affect production, and thus measured depletion in years \(t\,+\,1, t\,+\,2 {\ldots }\), but we do not include this in the depletion term for year t.

The output measure in the TFP is conventional GDP and not alternative “Green” adjusted variants nor does our TFP calculation incorporate “green” capital (e.g. see Mota et al. 2010 for discussion).

Note that we have adopted a slightly different convention to calculating the consumption variable here compared to Greasley et al. (2014). In the present paper, we add up the discounted values of differences between pairs of years (t) and (\(t\,+\,1\)) over the requisite time interval, as per Ferreira et al. (2008). Greasley et al. took the present value of the difference between the first year and the last year of each interval. This actually makes little difference to the results.

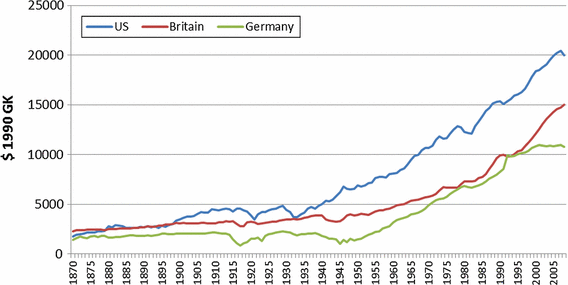

Fig. 3

Consumption per capita, US, Britain and Germany 1870–2008

Given that estimation is effectively bi-variate the potential issue of potential multiple cointegrating vectors is ruled-out.

The second approach considered estimates the model using FMOLS and applies the Hansen (1992) test for cointegration. The results, not presented here due to space considerations, confirm all the qualitative conclusions on cointegration (and hence robustness) of Table 4 above and re-establish the weak sustainability conclusion, over the 50 year horizon, for the GSTFP variant with the non-rejection of \({\upbeta }_{0}=0\) and \({\upbeta }_{1}=1\) jointly; and \({\upbeta }_{1}=1\). Although other methods provide similar results, those reported are based upon the optimal method for the particular circumstance, i.e., when potential endogeneity exists we report IV method results etc. Reporting potentially sub-optimal method results in addition to those regarded as econometrically optimal appears redundant.

In this case, utilizing FMOLS and Hansen (1992) does not resolve the issue, as it did with the US. This is likely due to the size of the discontinuity experienced by Germany vis a vis the US: contrasting the effects of World War Two on Germany with those of the Great Depression on the USA.

The results for the three countries embed country specific discount rates, reflecting their real long term interest rates. Our findings are somewhat sensitive to the choice of discount rate. If a common 2.5 %/year discount rate (this is a consumption discount rate adopted present day by the UK Treasury, and also the long term real UK interest rate), then the estimated \({\upbeta }_{1}\) in the case of the US gives results, for GS, as B1 \(= 1.04*, 1.17*\), \(-0.03^{+}\) and, for GSTFP, B1 \(=0.5*^{+}\), 0.7*\(^{+}\), 1.25*\(^{+}\) for 20, 30 and 50 year horizons respectively. For Germany, also using a 2.5 discount rate for consumption and TFP, gives B1 for GS as \(1.16*, 1.38*^{+}\), and 0.32 and for GSTFP B1 \(= 0.621*^{+}, 0.880*, 1.23*\) over 20, 30 and 50 year horizons. Where * denotes significantly different from 0 and \(^{+}\) denotes significantly different from 1. US results using a 2.5 % discount rate are higher than those presented in Table 3 whereas the German results using a 2.5 % discount rate are lower than those in Table 5; in both cases reflecting the lower (2.5 vs. 3.5 %)/ higher (2.5 vs. 1.95 %) discount rate. Our preference, like that of Ferreira et al. (2008) is to use country specific discount rates.

References

Allen R (2014) American exceptionalism as a problem of global history. J Econ Hist 74(2):309–350

Arrow KJ, Dasgupta P, Goulder L, Mumford K, Oleson K (2012) Sustainability and the measurement of wealth. Environ Dev Econ 17(3):317–353

Barbier EB, Markandya A (2013) A new blueprint for a green economy. Earthscan, London

Blum M, Hanley N, McLaughlin E (2013) Genuine savings and future well-being in Germany, 1850–2000. Stirling Economics discussion paper series, 2013-13

Bohringer C, Jochem P (2007) Measuring the immeasurable: a survey of sustainability indices. Ecol Econ 63:1–8

Carr W (1991) A history of Germany, 1815–1990, 4th edn. London, Routledge

Carter SB, Gartner SS, Haines MR, Olmstead AL, Sutch R, Wright G (2006) Historical statistics of the United States, earliest times to the present, millennial edn. Cambridge University Press, Cambridge

Chichilnisky G, Heal G, Beltratti A (1995) The green golden rule. Econ Lett 49:174–179

De Long JB, Eichengreen B (1991) The marshall plan: history’s most successful structural adjustment program. NBER working paper no. 3899

Dietz S, Neumayer E (2007) Weak and strong sustainability in the SEEA: concepts and measurement. Ecol Econ 61(4):617–626

Dumke RH (1990) Reassessing the wirtschaftswunder—reconstruction and postwar growth in West-Germany in an international context. Oxf Bull Econ Stat 52:451–491

Engle RF, Granger CWJ (1987) Co-integration and error correction: representation, estimation and testing. Econometrica 55(2):251–276

Feinstein CH, Pollard S (eds) (1988) Studies in capital formation in the United Kingdom, 1750–1920. Oxford University Press

Ferreira S, Hamilton K, Vincent JR (2008) Comprehensive wealth and future consumption: accounting for population growth. World Bank Econ Rev 22:233–248

Ferreira S, Vincent JR (2005) Genuine savings: leading indicator of sustainable development? Econ Dev Cult Chang 53:737–754

Ferreira S, Moro M (2010) On the use of subjective well-being data for environmental valuation. Environ Res Econ 46:249–273

Greasley D, Hanley N, Kunnas J, McLaughlin E, Oxley L, Warde P (2013a) Comprehensive investment and future well-being in the USA, 1869–2000. Stirling Economics Discussion Paper 2013–06

Greasley D, Madsen JB, Wohar ME (2013b) Long-run growth empirics and new challenges for unified theory. Appl Econ 45:3973–3987

Greasley D, Hanley N, Kunnas J, McLaughlin E, Oxley L, Warde P (2014) Testing genuine savings as a forward-looking indicator of future well-being in the (very) long run. J Environ Econ Manag 61:171–188

Greasley D, Oxley L (1996) Discontinuities in competitivemness: the impact of the First World War on British industry. Econ Hist Rev 48:82–100

Greasley D, Oxley L (2010) Clio and the economist: making historians count. J Econ Surv 24:755–774

Hamilton K, Hartwick J (2005) Investing exhaustible resource rents and the path of consumption. Can J Econ 38(2):615–621

Hoffmann WG, Grumbach F, Hesse H (1965) Das Wachstum der deutschen Wirtschaft seit der Mitte des 19. Springer-Verlag, Berlin, Jahrhunderts

Hamilton K, Clemens M (1999) Genuine savings rates in developing countries. World Bank Econ Rev 13:33–56

Hamilton K, Withagen C (2007) Savings and the path of utility. Can J Econ 40:703–713

Hansen BE (1992) Tests for parameter instability in regressions with I(1) processes. J Bus Econ Stat 10:321–335

Helm D (2015) Natural capital: valuing the planet. Yale University Press, New Haven

Johansen S (1991) Estimation and hypothesis testing of cointegration vectors in gaussian vector autoregressive models. Econometrica 59:1551–1580

Kao C (1999) Spurious regression and residual-based tests for cointegration in panel data. J Econ 90:1–44

Kunnas J, McLaughlin E, Hanley N, Greasley D, Oxley L, Warde P (2014) How should pollution from fossil fuels be included in long-run measures of National Accounts and Sustainable Development indicators? Scand Econ Hist Rev 62(3):243–265

Maddison A (2001) The World economy: a millennial perspective. OECD, Paris

McLaughlin E, Hanley N, Greasley D, Kunnas J, Oxley L, Warde P (2014) Historical wealth accounts for Britain: progress and puzzles in measuring the sustainability of economic growth. Oxf Rev Econ Policy 30:44–69

Mota RP, Domingos T (2013) Assessment of the theory of comprehensive national accounting with data for Portugal. Ecol Econ 95:188–196

Mota RP, Domingos T, Martins V (2010) Analysis of genuine savings and potential green net national product. Ecol Econ 69:1934–1942

Neumayer E (2010) Weak versus strong sustainability: exploring the limits of two paradigms, 3rd edn. Edward Elgar, Cheltenham

Olson M (1982) The rise and decline of nations: economic growth, stagflation and social rigidities. Yale University Press, Yale

Oxley L, McAleer M (1993) Econometric issues in macroeconomic models with generated regressors. J Econ Surv 7(1):1–40

Pearce D, Barbier E, Markandya A (1990) Sustainable development: economics and development in the third World. Earthscan, London

Pearce D, Markandya A, Barbier E (1989) Blueprint for a green economy. Earthscan, London

Pearce DW, Atkinson G (1993) Capital theory and the measurement of sustainable development: an indicator of weak sustainability. Ecol Econ 8:103–108

Pemberton M, Ulph D (2001) Measuring income and measuring sustainability. Scand J Econ 103:25–40

Perron P (1989) The great crash, the oil price shock and the unit root hypothesis. Econometrica 57:1361–1401

Pezzey JCV (2004) One-sided sustainability tests with amenities, and changes in technology, trade and population. J Environ Econ Manag 48:613–631

Pezzey JCV, Hanley H, Turner K, Tinch D (2006) Comparing augmented sustainability measures for Scotland: Is there a mismatch? Ecol Econ 57:70–74

Phillips PCB, Hansen B (1990) Statistical inference in instrumental variables regression with I(1) processes. Rev Econ Stud 57:99–125

Rhode PW (2002) Gallman’s annual output series for the United States, 1834–1909. NBER working paper, Working Paper 8860

Solow R (1986) On the intergenerational allocation of natural resources. Scand J Econ 88:141–149

Tanguy I (2013) Sustainability is compatible with decreasing social welfare. Econ Bull 33:1116–1125

Weitzman M (1997) Sustainability and technical progress. Scand J Econ 99:1–13

World Bank (2006) Where is the wealth of nations? World Bank, Washington, DC

World Bank (2011) The changing wealth of nations. World Bank, Washington, DC

Acknowledgments

Nick Hanley thanks the University of Waikato for hosting him during the writing of this paper. We thank The Leverhulme Trust for funding this work under the project “History and the Future: the Predictive Power of Sustainable Development Indicators” (Grant Number F00241). We also thank three referees and the editor of this special issue for helpful comments on earlier versions of the paper. Thanks also to Giles Atkinson, Kirk Hamilton and Jack Pezzey for many suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Submitted to special issue of Environmental and Resource Economics in honour of Anil Markandya.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Hanley, N., Oxley, L., Greasley, D. et al. Empirical Testing of Genuine Savings as an Indicator of Weak Sustainability: A Three-Country Analysis of Long-Run Trends. Environ Resource Econ 63, 313–338 (2016). https://doi.org/10.1007/s10640-015-9928-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10640-015-9928-7