Abstract

This paper fills the gap in the study of the impact of Chinese companies' environmental performance (EP) on greenwashing based on the listed companies in China from 2010 to 2018. The relationship between EP and greenwashing is analyzed based on legitimacy theory and signal theory. From the empirical analysis, it is found that there exists a negative correlation between EP and greenwashing which supports the signal theory. Based on resource-based theory analysis, the impacts of environmental subsidies and political connections on the relationship between environmental performance and greenwashing are also analyzed. EP of enterprises receiving environmental protection subsidy has a greater inhibition effect on greenwashing. The negative effect of EP on greenwashing of state-owned enterprises is bigger than that of non-state-owned enterprises. This study can provide reference for government departments in deepening the reform of government environmental subsidies and environmental governance of state-owned enterprises.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Organizations faced with new institutional demands often respond symbolically but do not actually implement them. For example, listed companies disclose the planned capital expenditure for environmental protection in their financial reports, but the actual amount of subsequent expenditure is often less than this value (Patten, 2005). Companies have internal environmental management committees or formal governance guidelines, but they do not really work. Enterprises actively participate in the voluntary environmental protection projects of third-party organizations and disclose such information to the public, but in fact, the final environmental performance of enterprises is not significantly improved (Iatridis & Kesidou, 2018). Even after the occurrence of environmental crisis, enterprises selectively emphasize or partially disclose their environment-friendly behaviors to divert the attention of critics (Marquis & Toffel, 2012).

The above-mentioned behaviors are defined as decoupling; the behavioral deviation is caused by the excessive development of symbolic environmental behaviors and the neglect of matching substantive environmental behaviors. In the environmental protection actions of enterprises, the relationship between symbolic environmental behavior and substantive environmental behavior is superficial and connotation. For example, although the ISO14001 certification of enterprises is often considered to be more symbolic than substantive results, some enterprises in the sensitive period of public opinion will postpone the publication of the newly obtained ISO14001 certification (Carlos & Lewis, 2018). However, participation in ISO14001 certification is not environmental behavior decoupling. It will be considered as environmental behavior decoupling only when the organization participating in certification does not fully implement the relevant standards. Some scholars have made relevant definitions for this scenario. For example, Kim and Lyon (2015) used the difference between the amount of emission reduction previously promised by the enterprise and the actual amount of subsequent emission reduction to determine whether the enterprise has implemented the emission reduction plan and whether the enterprise is decoupled in a multi-year follow-up survey (Kim & Lyon, 2015). The phenomenon of environmental responsibility greenwashing belongs to the field of environmental information disclosure research. Environmental performance is an important reason for greenwashing (Guo et al., 2017), in this study selected Chinese companies are used as research samples to study the impact of environmental performance on greenwashing. At the same time, government factors play a pivotal role in the behavior of environmental responsibility information disclosure of Chinese companies. Therefore, this paper also studies the role of government factors in environmental performance and greenwashing.

From the perspective of resource-based theory, legitimacy theory and signal theory, the current literature examines the impact of greenwashing on financial performance driven by external pressure and profit (Berrone et al., 2017; de Freitas Netto et al., 2020). These theories have contributed to the understanding of environmental performance and sustainability reporting (Bose et al., 2021; Cormier et al., 2005). Legitimacy theory describes the key idea that changes the organizational and management practice. This does not necessarily occur through rational internal decision-making processes, but may also be the result of external influences (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). Mandatory influence from institutions such as regulators, parent companies or other powerful actors manifests itself in the legal obligation of an organization to comply with certain prescribed rules and regulations (Bose et al., 2018; Scott, 2013).

Access to resources and pressure from powerful stakeholders are the key driving forces for CSR (Social Responsibility Report) disclosure (Belal & Owen, 2007; Bose et al., 2018; Hou et al., 2016). Decision makers in this regard behave rationally and make positive choices by calculating a trade-off between the expected benefits and the possible legal penalties for non-compliance (Ingram & Clay, 2000).

Based on the literature, the research takes Chinese companies as the research samples and there are many researches reported on greenwashing and corporate financial performance (Gou, 2013), company market value (Du, 2015), and there are few research studies on the impact of environmental performance on greenwashing behavior. As mentioned above, greenwashing belongs to the scope of environmental information disclosure. Environmental performance and environmental information disclosure are mutually causal (Delmas et al., 2007; Du, 2015; Huang & Chen, 2014; Kim & Lyon, 2015; Peng et al., 2008; Shi & Xu, 2018). There are three main impacts of environmental performance on environmental information disclosure: positive, negative and nonlinear. In this work, the relationship between EP and greenwashing through panel data from the driving factors of environmental regulation and government subsidies will be analyzed and discussed. Therefore, driven by factors such as political connection and access to government subsidies for scarce resources, how does EP affect greenwashing will be studied?

In particular, we investigate these practices in China as they occurred into regulatory guidance on listed companies’ engagement in environmental activities, using China as a context. In 2010, the regulator of Ministry of Environmental Protection in China introduced a set of initiatives, known as the “Environmental Information Disclosure Guidelines for Listed Companies”, guiding all listed companies toward adopting and practicing this approach in their business operations. In the study the impact of the influence of environmental regulatory (government subsidies) and political connection coupled with the nature of enterprise property right on the level of environment information disclosure through developing a greenwashing index is analyzed. This is done by using 244 listed firm-year observations from 2010 to 2018. The ordinary least squares (OLS) regression method was employed to estimate the research model proposed in this work. To ensure the results were not influenced by endogeneity, methods proposed by Hausman were employed (Hausman, 1978). The main contributions of this study are as follows: (1) Based on the institutional background of China's environmental pollution control system, we study the influence of EP on greenwashing, and expand the research on Chinese enterprises' greenwashing. (2) The impact of environmental performance under environmental regulatory factors (government subsidy resources) on greenwashing is discussed. (3) This paper studies the influence of political affiliation on the relationship between environmental performance and greenwashing.

The next section introduces the institutional background of environmental information disclosure in China. Section 3 develops the theoretical analysis and hypotheses. Section 4 will outline the methodology of this work followed by results and supplementary analysis of Sect. 5, and finally, the findings of the study is concluded in Sect. 6 along with future research directions.

2 Environmental information disclosure in China

China issued a series of environmental disclosures for listed companies. In 2006, Shenzhen Stock Exchange issued social Responsibility Guidelines for Listed Companies. The fifth chapter in this document focuses on environmental protection and sustainable development, including staff training referring to environment protection, use of environmentally friendly materials and process improvement of environmentally friendly production process. This document also focused on industrial waste, energy saving, and cyclic utilization. Compared with the previous regulations, the “Measures on Environmental Information Disclosure” released by the State Environmental Protection Administration of China in 2007 added new contents that includes the Environmental protection policy, Environmental strategy and planning. In 2008, the Shanghai Stock Exchange published more detailed “Guidelines on Environmental Information Disclosure of Listed Companies”, which set requirements for companies in heavy thermal power generation, steel, cement, electrolytic aluminum, mineral development and other industries with a large impact on the environment. This document emphasizes pollution monitoring and control, the operation of environmental protection facilities and the type, quantity, concentration of pollutants discharged by the company must be published in time. The above documents mainly encourage the disclosure of environmental information and are not mandatory.

In 2010, the Ministry of Environmental Protection of China further published the “Guidelines on Environmental Information Disclosure of Listed Companies”, which was mandatory and more detailed in terms of the content of environmental information disclosure. Listed companies “should” publish environmental reports on the website of the Ministry of Environmental Protection, China Environment News and company websites. The new content of Environmental information disclosure mainly includes the implementation of the Environmental impact assessment of construction projects in accordance with the law and the “three Simultaneous” acceptance system (Environmental auditing), the organizational structure of the company's internal Environmental management and the related responsibilities of its personnel (Establishment of the environmental protection department); Environmental protection honors; Environmental mark certification and Environmental management system certification (Environmental Certification); Other Environmental information includes Environmental organizations' participation in promoting Environmental protection, Ecological Restoration, Environmental charity, and other Environmental public welfare projects. Other environmental information disclosure indicators including Green supplier selection, Green Business development, Green office, Green marketing, Environmental cost accounting clean energy use are also included which can be found in this paper (Gou, 2013). The sources of all environmental information indicators are shown in Table 1.

3 Theoretical analysis and hypothesis

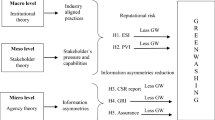

This section mainly covers the theoretical analysis and the hypothesis of the proposed work. Firstly, since 2008, when “Southern weekly” published the greenwashing list of Chinese enterprises for the first time, the greenwashing phenomenon has attracted attention from all sides. The degree of greenwashing of enterprises is influenced by EP, poor EP often leads companies to greenwash. The relationship between EP and greenwashing is discussed; secondly, the degree of greenwashing is also influenced by external factors such as government factors over time. It is worth exploring how the environmental factors affect the relationship between EP and greenwashing.

3.1 Institutional influences

Institutional theory is widely used to study environmental issues and practices of firms (Bansal & Clelland, 2004; Bansal & Kistruck, 2006; Delmas & Burbano, 2011; Lounsbury, 2001; Walls & Hoffman, 2013). As an open system, the boundaries between the enterprise and the surrounding environment are blurred and permeate each other. The development of the enterprise is not only subjected to the pressure related to technology and resources, but also the pressure related to the surrounding institutions, beliefs and customs (Bromley & Powell, 2012; Testa et al., 2018).

Firms do not always passively conform to institutional influences and in the pioneering work by Oliver (1991) a type of strategic response of firms is developed to study the institutional influences (Oliver, 1991). Complete conformity or compromise by firms is observed to the extent that the firm’s goals, interests and resource base are congruent with the institutional actors’ influences (García-Sánchez et al., 2020; Khan & Mir, 2019; Oliver, 1991; Scott, 2013). By complying with institutional influences, firms expect greater economic returns (e.g., greater access to scarce resources) and social legitimacy (Julian & Ofori Dankwa, 2008; Khan et al., 2020). Firms can also avoid institutional pressure by concealing inconsistencies, responding symbolically (decoupling) or buffering pressure by reducing the extent to which firms are subject to external scrutiny (Goodrick & Salancik, 1996; Khan et al., 2020). When compliance with institutional requirements conflicts with firms' efficiency requirements and when institutional actors have conflicting expectations, symbolic responses and firms' buffering behavior can be observed (Khan et al., 2020; Meyer & Rowan, 1977). Legitimacy is a core concept of institutional theory, which refers to whether an organization's behavior conforms to certain social systems and cognitive norms (Meyer & Rowan, 1977; Ruef & Scott, 1998; Suchman, 1995). In order to be recognized, enterprises should not only comply with legal requirements or market demand, but also comply with mainstream norms and values of society (Alrazi et al., 2015). If stakeholders do not recognize the activities of the enterprise, then the enterprise will face legitimacy pressure. Previous studies reported that, an important motivation for enterprises to adopt green behaviors is to be recognized by various stakeholders (Berrone et al., 2017). Delgado-Ceballos et al. (2012) found that stakeholders can influence environmental behavior of enterprises through various channels, including environmental regulations, environmental reports of NGOs, social media monitoring, and resistance of customers and suppliers to non-environmental products (Delgado-Ceballos et al., 2012). Generally, green behavior has become an important way for enterprises to cope with external pressure (Berrone et al., 2013). The greater the pressure of legitimacy that companies obtain from stakeholders, the more likely they are to adopt green strategies (Murillo Luna et al., 2008).

3.2 Hypothesis of corporate environmental performance and greenwashing

This section focuses on the theories related to the study of corporate environmental responsibility, which mainly include two groups: legitimacy theory and signaling theory. According to the legitimacy theory, enterprises choose to disclose corporate environmental information in order to obtain legitimacy, and environmental information disclosure is a function of social and political pressure faced by enterprises. For enterprises with poor environmental performance, their legitimacy is more threatened by society than those with good performance, so they need to disclose more environmental information to relieve pressure from stakeholders (Yang et al., 2020). When taking Australian enterprises as research objects, Clarkson et al. (2014) found that polluting enterprises do face greater social pressure and disclose more symbolic environmental information. Main reasons are as follows: good corporate environmental performance does not bring environment “premium” to enterprise, namely, the stakeholders will not pay more to buy the product or the price of the stock due to the good enterprise environmental performance; enterprises with poor environmental performance will not suffer additional social pressure or legal punishment when they obtain legitimacy through greenwashing. Enterprises with poor EP will be encouraged to continue to whitewash their environmental information disclosure if the public's environmental awareness is weak and their false information disclosure cannot be exposed or punished. From the perspective of legitimacy theory, the worse the environmental performance, the more inclined enterprises are to greenwash.

However, according to the signal theory, only enterprises with good environmental performance will try to disclose more environmental information in order to distinguish themselves from enterprises with poor EP and reduce greenwashing by delivering “good news”. One research found that investors regarded the environmental information disclosure of enterprises as a proof to judge the environmental management ability of enterprises (Amiraslani et al., 2013). The better the EP of enterprises, the stronger the competitiveness, thus there is a significant positive correlation between EP and environmental information disclosure. According to signal theory, good EP will bring corresponding “environmental premium” to enterprises, so as to encourage enterprises with good EP to disclose more substantial environmental information; enterprises with poor EP will attract public attention by greenwashing environmental information disclosure, which will cause enterprises to face additional litigation and punishment, thus inhibiting their continued “green” environmental information behavior. Therefore, the difference in social background is an important reason for the inconsistency of empirical results. There is a positive correlation when taking American companies as samples and a negative correlation between Australian companies when taking Australian companies as samples (Clarkson et al., 2008, 2014). In China, with the development of public responsibility awareness, corporate environmental responsibility has become the focus of attention of the government and the public. Cadmium pollution in the Longjiang River in Guangxi in 2012 (http://www.gov.cn/jrzg/2013-07/17/content_2450010.htm) was a water pollution incident that was concerned about and promoted throughout the entire process by the public. ConocoPhillips was sued by hundreds of farmers for the oil spill in Bohai Bay in 2011 (http://news.sohu.com/20141210/n406831271.shtml), and was punished by the government with 1.683 billion yuan in oil spill compensation, which also reflects the strong sanctions imposed by the government on the harsh environmental behavior of the company.

Under the background of the current strict ecological system constraints in China, only companies that actively carry out environmental management have the ability and willingness to disclose more environmental information. If companies with poor EP want to “camouflage” green environmental information, they not only will be severely punished by the government, their acquisition of legitimacy will also face a crisis of public trust. In other words, companies with good EP are more willing to disclose their true efforts in fulfilling their environmental responsibilities (Delmas & Montes Sancho, 2010; Khan et al., 2020; Lyon & Montgomery, 2015). The first hypothesis proposed in this study is:

H1

Companies with better environmental performance tend to reduce greenwashing.

3.3 The impact of government subsidy on the relationship between EP and greenwashing

In order to encourage enterprises' environmental protection behaviors, the government will implement preferential policies or financial subsidies to enterprises meeting the requirements and encourage enterprises to take the initiative in environmental protection, mostly in the form of environmental protection subsidies and emission permits (Jefferson et al., 2013; Zhao et al., 2009).

The government subsidies have two kinds of effects, one is an incentive effect, and the other is crowding out effect. Researchers who hold the view of incentive effect believe that government subsidies can stimulate enterprise innovation by alleviating financing constraints of enterprises, sharing the risk of innovation failure, and bridging the gap between private and social rates of return (Clausen, 2009). The spillover effect of subsidies will make future green R&D activities face lower fixed costs and have a positive impact on the profitability of non-subsidized projects (Alecke et al., 2012; Boeing et al., 2016). The incentive effect of government subsidies can encourage enterprises to upgrade green production processes and strengthen green environmental management, so as to improve their environmental performance and actively disclose real environmental information.

Researchers who hold the view of crowding-out effect believe that due to information asymmetry, the government finds often difficult to identify which projects are worthy of government subsidies, so it is possible to invest funds in inefficient projects, and there is adverse selection in advance. In the absence of effective regulation, enterprises may invest the subsidy funds for non-R&D purposes, resulting in post-mortem ethical risk (Antonelli & Crespi, 2013). At the same time, the government officials who allocate subsidies are inclined to invest the subsidy funds in projects with high-expected success rate, high return rate and fast income due to the consideration of political performance. However, these projects often do not face financing constraints, and government subsidies squeeze out enterprises' own green R&D expenditure (Catozzella & Vivarelli, 2016).

Environmental subsidies are government funds to help enterprises improve their environmental protection policies, involving ecological conservation, or the protection, defense or shelter of natural resources (Ren et al., 2019). Governments use environmental sustainability schemes to encourage companies to substantially improve their environmental sustainability. In order to ensure the effectiveness of environmental protection subsidy policy, the government has formulated a series of policies to ensure the effective operation of environmental protection subsidy policy. For example, during the 12th Five-Year Plan period of China (2011–2015), an environmental system was established focusing on waste treatment, energy conservation and emission reduction, elimination of outdated production capacity and technological upgrading (Lin et al., 2015; Ren et al., 2019). This policy has continued to work effectively. In October 2020, The State Council issued the Development Plan for the New Energy Vehicle Industry (2021–2035), encouraging the research and development of high-quality patents in the field of new energy vehicles. China strives to achieve international leading level in key technologies of new energy vehicles and build quality brands by 2035 (Li, 2020). In this context, in order to encourage new energy vehicle enterprises to break through technical difficulties, China adopts government subsidies and other policy tools to support enterprise innovation and development. Among them, the government subsidy as the government free expenditure, has a strong fund specificity.

In view of the implementation background of the above environmental subsidy policies in China, this paper argues that environmental subsidy can effectively motivate enterprises to improve environmental performance and reduce greenwashing behavior. Therefore, the following hypothesis is proposed:

H2

For companies enjoying environmental protection subsidies, their environmental performance has a stronger negative impact on greenwashing behavior.

3.4 The impact of the nature of enterprise property rights on the relationship between EP and greenwashing

Economic system in China is unique where the public economy is the main source and the non-public economy is in a secondary position. According to different environmental governance motivations, there will be a big difference in environmental performance of enterprises with different property rights properties.

The state-owned enterprises are inextricably linked with the government, its executives assigned by government agencies both have government service background and has strong political association (Greenstone et al., 2012). However, on-state owned enterprises do not have these natural political advantages, in the face of various environmental pressure, non-state-owned enterprises when it governs the environment considering the pressures of the state environmental protection laws and regulations and enterprise strategic investment vision are often based on economic considerations and pay attention to the cost effectiveness of environmental governance (Harjoto et al., 2015).

In essence, political connection is a special relationship between government and enterprise, through which enterprises can obtain relevant resources such as government subsidies and support. Senior executives (For example chairman, general managers) at state-owned enterprises (SOES) are appointed by the State-owned Assets Supervision and Administration Commission (SASAC). Based on the special situation of China's state-owned enterprises, under the dual pressure of meeting environmental demands and economic development, state-owned enterprises have an incentive to reduce greenwashing to cope with external pressure (Bose et al., 2021).

As China proposes to build an ecological civilization, the country is attaching more and more importance to the environmental performance of SOES social responsibility. In particular, Chinese governments at all levels include environmental performance in the evaluation mechanism for official promotion. As managers appointed by the government to state-owned enterprises, they will also pay more attention to environmental performance for their own political career. According to the resource dependence theory, the operation of an enterprise needs to obtain resources from the social system. This is an important goal for the survival and long-term development of an enterprise to obey social norms, be interdependent with the surrounding environment, and relieve the constraints of external key resources (Hillman et al., 2009). Existing literature shows that the establishment of political connection can help enterprises strengthen effective communication with government departments, comprehensively and timely understand environmental policy guidance. In addition, because of their special social influence, politically connected executives can help enterprises acquire more high-quality social resources. At the same time, based on the high political sensitivity of senior executives, SOES will actively show their due sense of social responsibility and moral model, and actively perform green innovation behaviors to promote their green development and improve their environmental performance.

H3

Compared with private enterprises, state-owned enterprises with better EP tend to reduce greenwashing.

4 Methodology

This part mainly includes three sections: sample selection and data source, variable selection and definition, description and model setting.

4.1 Data sources and sample selection

Chinese listed A-share companies that issued independent reports from 2010 to 2018 were selected from the China Stock Market & Accounting Research Database (CSMAR) and matched with “the list of government environmental protection subsidies” issued by the Ministry of Environmental Protection of China every year. Stata15.0 was used to finally sort out the unbalanced panel data consisting of 1278 samples. The greenwashing data is obtained by manual sorting and other data are obtained from CSMAR database (see Table 2).

4.2 Definition of variables

(1) Dependent variable

The measurement method of greenwashing has not been unified yet. The authors define it as the ratio between the score of symbolic behavior and the score of substantive behavior plus 1 which is named “GreenIndex” by authors [see Eq. (1)]. In the denominator, the score of substantive behavior plus 1 is due to the fact that the score of substantive behavior is all 0. The meaning of greenwashing index is the “false-green” degree of each unit of substantial environmental behavior.

Here, \({\mathrm{symbolic}}_{k}\) represents the total score of 22 symbolic indicators, while \({\mathrm{substantial}}_{k}\) represents the total score of 22 substantive indicators.

Symbolic behavior and substantive behavior are two sub-indicators of greenwashing. The authors adopts the principle of collecting greenwashing data (Lyon & Montgomery, 2015; Walker & Wan, 2012). There are a total of 22 indicators to measure greenwashing [see Appendices 1, 2, Eqs. (2) and (3)].

\({x}_{ki}\) represents the score of enterprise k on the i index. When the enterprise has substantial action on the i indicator, the value is 1, otherwise it is 0.

\({x}_{ki}\) represents the score of enterprise k on the i index. When the enterprise has symbolic behavior on the i indicator, the value is 1, otherwise 0.

In order to ensure the accuracy of the selected data, each member of the research team collates the same batch of sample data in advance to compare the score differences between symbolic indicators and substantive indicators, and then discusses the judgment indicators with large differences until the scores of each member of the team are the same. The authors spent significant time sorting out the data from the independent annual reports, social responsibility reports, environmental responsibility reports and official websites of all Listed A-share companies in China, and finally obtained the greenwashing data of 980 companies from 2010 to 2018. Where 244 companies were finally selected for the analysis through data matching. In the following two paragraphs, the meanings of symbolic indicators and substantive indicators are briefly introduced with examples. Readers may refer to this article (Walker & Wan, 2012) for specific definitions.

A substantive environmental practice is used to describe the actual actions or measures taken by an enterprise to improve the environment. It usually involves environmental details and contains quantitative data that require more words to convey the substance of its actions to improve the environment. For example (Excerpts from 2011 CSR of Huolinhe Opencut Coal Industry Corporation Limited of Inner China): “By 2011, company A had invested 46,358,800 RMB in mine ecological management, carried out ecological environmental management of 14,011.15 MU (unit of measurement of land area in China) of land, and the reclamation rate could reach more than 95%. In 2011, the reclamation rate of the land dump that can be reclaimed has achieved the target of 100% reclamation rate. The area of the land dump that can be reclaimed has been determined to be 402.7 MU, and the investment has reached 1.6333 million RMB, meeting the requirements of relevant regulations”.

Symbolic environmental practice describes the measures that enterprises attach importance to environmental protection or will take to protect the environment. The following is extracted from a corporate social responsibility report (Excerpts from 2017 CSR of Jiangsu Lianfa Textile Co., Ltd of China): “Through the selection of environment-friendly dyes, resource recycling, energy conservation and emission reduction and a series of measures, it has truly realized clean production.” The content shows the measures taken by the enterprise to protect the environment, but it does not explain the specific environmental protection effect after taking these measures, does not specify the specific name of the technology adopted and how much reduction of various types of waste discharge, it is just a kind of verbal description, confusing the public.

(2) Independent variable

In this paper, environmental capital expenditures per unit of business income measures the environmental performance of an enterprise. Sewage charge is a kind of tax levied by the national government based on various factors, such as the characteristics of the industry and the types of pollutant discharged by enterprises, which is suitable for the research of enterprises in different industries. The more environmental protection funds are spent, the more capable enterprises are to improve production and technology, reduce resource consumption, effectively control pollutant discharge, and the better their environmental performance will be. Therefore, this paper takes the ratio of environmental protection funds to operating income as a proxy variable for the environmental performance of enterprises, and determines the corresponding amount by manually sorting out and inquiring the financial statements of enterprises.

(3) Control variables

Based on the articles (Seifert et al., 2004; Walker & Wan, 2012), enterprise’s scale, redundant resources, enterprise solvency, operation ability, annual dummy variable and pollution industry dummy variable are selected. The specific variables are shown in Table 3.

4.3 Model setting

Equation (4) is used to verify hypothesis H1, H2, and H3. The model is set as follows:

GreenIndex represent the greenwashing index, EP represents the enterprise environmental performance, and corresponding coefficient is \({\alpha }_{1}\). Control variables included are year and the industry, \({\alpha }_{0}\) is the intercept term, and \(\varepsilon\) is the disturbance term. To overcome the possible cross-section correlation, time series correlation and heteroscedasticity problems of panel data, D–K (Driscoll–Kraay) standard error method was used for estimation.

5 Results

This section includes descriptive statistics and multicollinearity, hypotheses testing, and model robustness analysis. The first part mainly analyzes the main performance characteristics of the data and eliminates the model setting errors caused by excessive multicollinearity to explain the rationality of the selected variables. The second part discusses the test of hypothesis H1 to hypothesis H3. In the last part, the robustness of the constructed model is verified by replacing explained variables, using two-stage least square method (2SLS) and adding macroeconomic variables to ensure the correctness and reliability of the conclusion.

5.1 Descriptive analysis and multicollinearity analysis

Descriptive statistics are conducted to explore the distribution trend of data and find out extreme outliers, so as to avoid the impact of extreme outliers on the econometric model. Multicollinearity problems can lead to bias in the conclusions being studied.

5.1.1 Descriptive statistics

In 2006, the State Council of China issued a document titled “The Decision of the State Council on Implementing the Scientific Outlook on Development and Strengthening Environmental Protection” (http://www.gov.cn/zwgk/2005-12/13/content_125736.htm). Based on which the Shanghai Stock Exchange issued “The Guidance on Strengthening environmental Protection Supervision and Administration of Listed Companies” (http://www.gov.cn/zwgk/2008-02/25/content_900324.htm) in 2008. All listed companies are required to write independent annual report, social responsibility report, etc. in accordance with this guidance. As can be seen from in Table 4, the minimum value of GreenIndex is 0.500, the maximum value is 6, and the mean value is 1.566, indicating that most of the samples have a symbolic total score greater than the substantive one, and there is a large difference in the environmental behavior of enterprises. It indicates that enterprises compile social responsibility reports or sustainable development reports according to official guidance documents, but exaggerate some of their unimplemented environmental protection behaviors, showing obvious “greenwashing” behavior. The minimum value and maximum value of EP are 0 and 11.767%, and the average value is 0.223%. The mean value of Ind is 0.689, indicating that the sample of polluting industries is dominant.

5.1.2 Multicollinearity analysis

It can be seen from Table 5 that, except for the logarithmic correlation coefficient of total assets and earnings reserve (0.840), which exceeds 0.5, all other correlation coefficients are less than 0.3. All variance inflation factors in Table 6 are less than 10, indicating that there is no serious multicollinearity among variables, which meets the requirements of the econometric model for independent variables.

5.2 Model hypothesis testing

Column (1)–(5) in Table 7 successively put the control variables and explanatory variables in order to test the robustness of the constructed model as shown in Sect. 4. EP is negatively related to GreenIndex, and the hypothesis H1 is verified.

5.3 Hypothesis testing of market incentive environmental regulation and property right

This part mainly introduces the empirical results of Market Incentive Environmental Regulation (MIER) and property right of enterprises. This section analyze the reasons for different hypothesis to draw different conclusions.

The enterprises receiving environmental protection subsidies and those not receiving environmental protection subsidies were analyzed using regression, and the regression results are presented in Table 8. In Table 8, the govsub value is 1, which represents the enterprise receiving government environmental protection subsidies; otherwise, the value is 0. The column (1) shows the regression results of enterprises receiving environmental protection subsidies, while column (2) shows the regression results of enterprises not receiving environmental protection subsidies. In Table 8, the absolute value of GreenIndex coefficient in column (1) is larger than that in column (2). 0.0895 is bigger than 0.0648. Hypothesis H2 is verified, it indicates that the government's environmental protection subsidy to enterprises is more conducive to the improvement of enterprises' environmental performance and the reduction of greenwashing behavior. The reason is that the crowding out effect of environmental subsidies is always smaller than the incentive effect, which shows that China's current environmental subsidy policy is very effective.

Table 8 shows the regression results of enterprise properties in columns (3) and (4). In column (4), the coefficient of EP is negative (− 0.126). Hypothesis H3 is verified, compared with non-state-owned enterprises, state-owned enterprises tend to be in the same camp with the government. In the field of environment, they receive more attention from stakeholders and face greater legal pressure. State-owned enterprises (SOES) have stronger political background and are more likely to comply with environmental laws and regulations and conscientiously fulfill their environmental protection responsibilities. In the long run, due to China's special economic system, state-owned enterprises are in a competitive position and easy to obtain monopoly profits. Environmental protection investment is characterized by large investment, low rate of return and long recovery time (Ren et al., 2019). Only state-owned enterprises with strong economic strength can increase environmental protection investment. They are willing to allocate more redundant resources to environmental protection to meet the standards of environmental laws and regulations.

There are other factors contributing to the decline in greenwashing by state-owned enterprises. As China proposes to build an ecological civilization, the country is attaching more and more importance to the environmental performance of SOES social responsibility. In particular, Chinese governments at all levels include environmental performance in the evaluation mechanism for official promotion. As managers appointed by the government to state-owned enterprises, they will also pay more attention to environmental performance for their own political career. According to the resource dependence theory, the operation of an enterprise needs to obtain resources from the social system. Existing literature shows that the establishment of political connection can help enterprises strengthen effective communication with government departments, comprehensively and timely understand environmental policy guidance (Chen & Hamilton, 2020; Hillman et al., 2009). In addition, because of their special social influence, politically connected executives can help enterprises acquire more high-quality social resources. At the same time, based on the high political sensitivity of senior executives, SOES will actively show their due sense of social responsibility and moral model, and actively perform green innovation behaviors to promote their green development and improve their environmental performance, the greenwashing behavior of SOES is reduced.

5.4 Robustness test

The authors examined the robustness of the proposed models in Eq. (4) in three ways. Firstly, as mentioned above, in this paper, EP lag period was used as a tool variable, and 2SLS method was used to conduct robustness test. Secondly, the dependent variable was replaced and the ratio of environmental capital expenditure to total operating cost was used as the dependent variable for robustness test. Thirdly, in view of the correlation between business status and economic development status of enterprises, the authors added macroeconomic variables to construct a new control variable group for robustness test of the model. To further test the robustness of the constructed equation, the authors incorporated macroeconomic variables into the model, including GDP (lngdp), technology market turnover (pat), electricity consumption (lnelec), population density (lnintensity), volume of goods transported (lngrocery), provincial tax revenue (lntax), and urban greening rate (lngreen). The larger the scale of production, the more resources the city consumes, scientific and technological progress will promote the production process improvement or a variety of cleaner production technology, so the GDP and technology market turnover (pat) are selected (Grossman & Krueger, 1992), which represent the production scale and technical level of the region. There is a significant positive correlation between energy consumption and environmental pollution, and emissions are related to the use of fossil fuels (Jalil & Mahmud, 2009). In consideration of the impact of energy consumption on economic development and the availability of urban energy consumption data, electricity consumption (lnelec) is adopted to represent energy consumption in this paper, as there is a great correlation between industrial electricity consumption and total energy consumption level (Tu et al., 2019). The rapid concentration of population has brought about a series of urban problems such as traffic congestion, resource shortage and environmental deterioration, so population density (lnintensity) and volume of goods transported (lngrocery) are selected (Brownstone & Golob, 2009). Local tax competition will affect investment and industrial agglomeration, and then affect environmental quality (Wu & Shen, 2013), provincial tax revenue (lntax) is chosen to represent the tax level. The higher the greening rate of a place, the better the environmental quality, which also shows the local government's serious attitude toward environmental protection, urban greening rate (lngreen) is selected. The authors use the 2010 CPI deflator to offset tax, GDP, and technology market turnover, and take a logarithmic approach to tax, GDP, population density, electricity consumption, volume of goods transported. Then, the ratio of sewage charge to operating income and the ratio of sewage charge to operating cost are used as the dependent variable to test the robustness, and most conclusions are found to be robust.

(1) 2SLS robustness test of MIER and property right

Results of the Hausman endogeneity test is shown in Table 9. The influence of endogeneity of explanatory variables was excluded. In this paper, the lagging one-phase variables of EP were used as instrumental variables, and the OLS and 2SLS (two stage least square) methods were used to carry out The Hausman endogeneity test (Groves et al., 1994). The lag period of endogenous variables is generally highly correlated with the endogenous variables of the current period and satisfies the correlation assumption; the lag period of endogenous variables has occurred and is not related to the disturbance term of the current period, and meets the exogenous conditions. In Table 11, first two columns represent the regression results without adding macro variables, Hausman value is 10.88, and the corresponding p value is 0.7611. The null hypothesis that the explanatory variable is exogenous is accepted. In the regression results after adding macroeconomic variables in the list (3) and (4), the Hausman value is 8.03, and the corresponding p value is 0.9971. The null hypothesis that the explanatory variable is exogenous is accepted. Table 10 shows the 2SLS robust regression results of MIER and Property Right which also support H2 and H3 (Tables 11, 12).

(2) Robustness test of the ratio of environmental capital expenditure to total operating cost (RETO)

(3) Robustness test of the ratio of environmental capital expenditure to operating cost by adding macroeconomic variables (RETOM)

6 Conclusions and recommendations

By manually collating the green washing data of Shanghai and Shenzhen A-share listed companies from 2010 to 2018, the authors constructed a panel data metering model of enterprise environmental performance and green washing. In the full-sample regression, the authors analyze the influence of environmental performance on greenwashing based on the legitimacy pressure and signal theory. The conclusion shows that the better the environmental performance is, the more it can reduce the greenwashing behavior of enterprises, which supports the signal theory. In addition, based on resource-based theory, we consider the impact of government subsidies and political connections on the relationship between environmental performance and greenwashing. We adopted 2SLS and added macroeconomic control variables to conduct robustness tests, which further verified the correctness of the conclusion. The empirical results show that the environmental performance of enterprises receiving environmental protection subsidies has a greater inhibitory effect on greenwashing. The reason is that in the context of the current Chinese government subsidy policy, the government subsidy has a leading role in the incentive effect, which exceeds the crowding effect. Compared with private enterprises, the environmental performance of state-owned enterprises has a more obvious negative impact on greenwashing. The reasons are that state-owned enterprises have easy access to political resources based on political background and the promotion mechanism of Chinese officials plays a positive role in urging state-owned enterprises to improve their environmental performance.

This study makes recommendations based on the above conclusions. First, compared with state-owned enterprises, non-state-owned enterprises do not have a natural political background and are in a weak position in market competition. They do not have enough funds to invest in the field of environmental protection, and their environmental performance does not show behaviors that inhibit greenwashing. When formulating environmental protection policies, it is necessary to distinguish between private enterprises and state-owned enterprises. This study recommends that China open up certain monopoly areas, allow private enterprises to participate in competition, and gain a share of the monopoly industry (Huang, 2019). Only after improving financial performance can there be sufficient motivation and ability to fulfill environmental responsibilities, and reduce greenwashing behavior.

Secondly, the regression results of state-owned enterprises show that there is a significant negative relationship between environmental performance and green bleaching. It shows that under the current official promotion and green assessment system, state-owned enterprise executives have gradually paid attention to green development, which has effectively improved environmental performance and reduced greenwashing (Tang & Bae, 2021). However, in view of the frequent occurrence of ecological and environmental problems in China, it is recommended that the government continue to deepen the reform of state-owned enterprises, increase the proportion of ecological performance indicators in the official promotion mechanism, and urge decision-makers of state-owned enterprises to earnestly fulfill their environmental obligations.

Thirdly, compared with the enterprises that do not enjoy environmental subsidies, the inhibition effect of environmental performance on greenwashing does not improve significantly. It is necessary to further refine the policy of environmental subsidies, increase the detailed rules of environmental subsidies, and restrain enterprises from “cheating subsidies and changing the use of environmental funds” (Ren et al., 2019).

Authors consider the following research directions for this study: First, greenwashing is not only found in heavy pollution industries, but also in other industries (Ren et al., 2019). Secondly, this paper only studies the influence of environmental subsidies and political connections on the relationship between environmental performance and greenwashing, and does not consider the influence of legitimacy pressures such as mandatory environmental regulation and public pressure on this relationship, which will be a major direction of future research (de Freitas Netto et al., 2020; DiMaggio & Powell, 1983). Thirdly, more and more Chinese companies are implementing internationalization strategies. In order to meet the requirements of the host country's legitimacy, the influence of Chinese enterprises' internationalization behavior on enterprises' “green cleaning” is a new research direction (Marquis et al., 2016; Testa et al., 2018).

References

Alecke, B., Reinkowski, J., Mitze, T., & Untiedt, G. (2012). Does firm size make a difference? Analysing the effectiveness of R&D subsidies in East Germany. German Economic Review, 13(2), 174–195.

Alrazi, B., De Villiers, C., & Van Staden, C. J. (2015). A comprehensive literature review on, and the construction of a framework for, environmental legitimacy, accountability and proactivity. Journal of Cleaner Production, 102, 44–57.

Amiraslani, H., Latridis, G. E., & Pope, P. F. (2013). Accounting for asset impairment: A test for IFRS compliance across Europe. Citeseer.

Antonelli, C., & Crespi, F. (2013). The “Matthew effect” in R&D public subsidies: The Italian evidence. Technological Forecasting and Social Change, 80(8), 1523–1534.

Bansal, P., & Clelland, I. (2004). Talking trash: Legitimacy, impression management, and unsystematic risk in the context of the natural environment. Academy of Management Journal, 47(1), 93–103.

Bansal, P., & Kistruck, G. (2006). Seeing is (not) believing: Managing the impressions of the firm’s commitment to the natural environment. Journal of Business Ethics, 67(2), 165–180.

Belal, A. R., & Owen, D. L. (2007). The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement-based study. Accounting, Auditing & Accountability Journal, 20(3), 472–494.

Berrone, P., Fosfuri, A., & Gelabert, L. (2017). Does greenwashing pay off? Understanding the relationship between environmental actions and environmental legitimacy. Journal of Business Ethics, 144(2), 363–379.

Berrone, P., Fosfuri, A., Gelabert, L., & Gomez Mejia, L. R. (2013). Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strategic Management Journal, 34(8), 891–909.

Boeing, P., Mueller, E., & Sandner, P. (2016). China’s R&D explosion—Analyzing productivity effects across ownership types and over time. Research Policy, 45(1), 159–176.

Bose, S., Khan, H. Z., & Monem, R. M. (2021). Does green banking performance pay off? Evidence from a unique regulatory setting in Bangladesh. Corporate Governance: An International Review, 29(2), 162–187.

Bose, S., Khan, H. Z., Rashid, A., & Islam, S. (2018). What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pacific Journal of Management, 35(2), 501–527.

Bromley, P., & Powell, W. W. (2012). From smoke and mirrors to walking the talk: Decoupling in the contemporary world. Academy of Management Annals, 6(1), 483–530.

Brownstone, D., & Golob, T. F. (2009). The impact of residential density on vehicle usage and energy consumption. Journal of Urban Economics, 65(1), 91–98.

Carlos, W. C., & Lewis, B. W. (2018). Strategic silence: Withholding certification status as a hypocrisy avoidance tactic. Administrative Science Quarterly, 63(1), 130–169.

Catozzella, A., & Vivarelli, M. (2016). The possible adverse impact of innovation subsidies: some evidence from Italy. International Entrepreneurship and Management Journal, 12(2), 351–368.

Chen, Z., & Hamilton, T. (2020). What is driving corporate social and environmental responsibility in China? An evaluation of legacy effects, organizational characteristics, and transnational pressures. Geoforum, 110, 116–124.

Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4–5), 303–327.

Clarkson, P. M., Overell, M. B., & Chapple, L. (2014). Environmental reporting and its relation to corporate environmental performance. Abacus, 47(1), 27–60.

Clausen, T. H. (2009). Do subsidies have positive impacts on R&D and innovation activities at the firm level? Structural Change and Economic Dynamics, 20(4), 239–253.

Cormier, D., Magnan, M., & Van Velthoven, B. (2005). Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions? European Accounting Review, 14(1), 3–39.

de Freitas Netto, S. V., Sobral, M. F. F., Ribeiro, A. R. B., & Da Luz Soares, G. R. (2020). Concepts and forms of greenwashing: A systematic review. Environmental Sciences Europe, 32(1), 1–12.

Delgado-Ceballos, J., Aragón-Correa, J. A., Ortiz-de-Mandojana, N., & Rueda-Manzanares, A. (2012). The effect of internal barriers on the connection between stakeholder integration and proactive environmental strategies. Journal of Business Ethics, 107(3), 281–293.

Delmas, M. A., & Burbano, V. C. (2011). The drivers of greenwashing. California Management Review, 54(1), 64–87.

Delmas, M. A., Montes, M. J., & Montes-Sancho, M. J. (2007). Voluntary agreements to improve environmental quality: Symbolic and substantive cooperation. Strategic Management Journal, 31(6), 575–601.

Delmas, M. A., & Montes Sancho, M. J. (2010). Voluntary agreements to improve environmental quality: Symbolic and substantive cooperation. Strategic Management Journal, 31(6), 575–601.

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 128, 147–160.

Du, X. (2015). How the market values greenwashing? Evidence from China. Journal of Business Ethics, 128(3), 547–574.

García-Sánchez, I., Hussain, N., Khan, S., & Martínez-Ferrero, J. (2020). Do markets punish or reward corporate social responsibility decoupling? Business & Society, 60, 1431–1467. https://doi.org/10.1177/0007650319898839

Goodrick, E., & Salancik, G. R. (1996). Organizational discretion in responding to institutional practices: Hospitals and cesarean births. Administrative Science Quarterly, 41, 1–28.

Gou, Q. W. (2013). Can both substantive and symbolic environmental management get paid?—An empirical study based on China Listing Corporation. Advanced Materials Research, 807–809, 760–763.

Greenstone, M., List, J. A., & Syverson, C. (2012). The effects of environmental regulation on the competitiveness of US manufacturing. No. w18392. National Bureau of Economic Research.

Grossman, G. M., & Krueger, A. B. (1992). Environmental impacts of a North American free trade agreement. CEPR Discussion Papers, 8(2), 223–250.

Groves, T., Hong, Y., McMillan, J., & Naughton, B. (1994). Autonomy and incentives in Chinese state enterprises. The Quarterly Journal of Economics, 109(1), 183–209.

Guo, R., Tao, L., Li, C. B., & Wang, T. (2017). A path analysis of greenwashing in a trust crisis among Chinese energy companies: The role of brand legitimacy and brand loyalty. Journal of Business Ethics, 140(3), 523–536.

Harjoto, M., Laksmana, I., & Lee, R. (2015). Board diversity and corporate social responsibility. Journal of Business Ethics, 132(4), 641–660.

Hausman, J. A. (1978). Specification tests in econometrics. Econometrica: Journal of the Econometric Society, 46, 1251–1271.

Hillman, A. J., Withers, M. C., & Collins, B. J. (2009). Resource dependence theory: A review. Journal of Management, 35(6), 1404–1427.

Hou, M., Liu, H., Fan, P., & Wei, Z. (2016). Does CSR practice pay off in East Asian firms? A meta-analytic investigation. Asia Pacific Journal of Management, 33(1), 195–228.

Huang, R., & Chen, D. (2014). Does environmental information disclosure benefit waste discharge reduction? Evidence from China. Journal of Business Ethics, 129(3), 535–552.

Huang, Y. (2019). Monopoly and anti-monopoly in China today. American Journal of Economics and Sociology, 78(5), 1101–1134.

Iatridis, K., & Kesidou, E. (2018). What drives substantive versus symbolic implementation of ISO 14001 in a time of economic crisis? Insights from Greek manufacturing companies. Journal of Business Ethics, 148(4), 859–877.

Ingram, P., & Clay, K. (2000). The choice-within-constraints new institutionalism and implications for sociology. Annual Review of Sociology, 26(1), 525–546.

Jalil, A., & Mahmud, S. F. (2009). Environment Kuznets curve for CO2 emissions: A cointegration analysis for China. Energy Policy, 37(12), 5167–5172.

Jefferson, G. H., Tanaka, S., & Yin, W. (2013). Environmental regulation and industrial performance: Evidence from unexpected externalities in China. Social Science Electronic Publishing.

Julian, S. D., & Ofori Dankwa, J. C. (2008). Toward an integrative cartography of two strategic issue diagnosis frameworks. Strategic Management Journal, 29(1), 93–114.

Khan, H. Z., Bose, S., & Johns, R. (2020). Regulatory influences on CSR practices within banks in an emerging economy: Do banks merely comply? Critical Perspectives on Accounting, 71, 102096.

Khan, S. J., & Mir, A. A. (2019). Ambidextrous culture, contextual ambidexterity and new product innovations: The role of organizational slack and environmental factors. Business Strategy and the Environment, 28(4), 652–663.

Kim, E., & Lyon, T. P. (2015). Greenwash versus brownwash: Exaggeration and undue modesty in corporate sustainability disclosure. Organization Science, 26(3), 705–723.

Li, J. (2020). Charging Chinese future: The roadmap of China’s policy for new energy automotive industry. International Journal of Hydrogen Energy, 45(20), 11409–11423.

Lin, H., Zeng, S. X., Ma, H. Y., & Chen, H. Q. (2015). How political connections affect corporate environmental performance: The mediating role of green subsidies. Human and Ecological Risk Assessment: An International Journal, 21(8), 2192–2212.

Lounsbury, M. (2001). Institutional sources of practice variation: Staffing college and university recycling programs. Administrative Science Quarterly, 46(1), 29–56.

Lyon, T. P., & Montgomery, A. W. (2015). The means and end of greenwash. Organization & Environment, 28(2), 223–249.

Marquis, C., & Toffel, M. W. (2012). When do firms greenwash?: Corporate visibility, civil society scrutiny, and environmental disclosure. Harvard Business School.

Marquis, C., Toffel, M. W., & Zhou, Y. (2016). Scrutiny, norms, and selective disclosure: A global study of greenwashing. Organization Science, 27(2), 483–504.

Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363.

Murillo Luna, J. L., Garcés Ayerbe, C., & Rivera Torres, P. (2008). Why do patterns of environmental response differ? A stakeholders’ pressure approach. Strategic Management Journal, 29(11), 1225–1240.

Oliver, C. (1991). Strategic responses to institutional processes. Academy of Management Review, 16(1), 145–179.

Patten, D. M. (2005). The accuracy of financial report projections of future environmental capital expenditures: A research note. Accounting, Organizations and Society, 30(5), 457–468.

Peng, M. W., Wang, D. Y., & Jiang, Y. (2008). An institution-based view of international business strategy: A focus on emerging economies. Journal of International Business Studies, 39(5), 920–936.

Ren, S., He, D., Zhang, T., & Chen, X. (2019). Symbolic reactions or substantive pro-environmental behaviour? An empirical study of corporate environmental performance under the government’s environmental subsidy scheme. Business Strategy and the Environment, 28(6), 1148–1165.

Ruef, M., & Scott, W. R. (1998). A multidimensional model of organizational legitimacy: Hospital survival in changing institutional environments. Administrative Science Quarterly, 43, 877–904.

Scott, W. R. (2013). Institutions and organizations: Ideas, interests, and identities. Sage Publications.

Seifert, B., Morris, S. A., & Bartkus, B. R. (2004). Having, giving, and getting: Slack resources, corporate philanthropy, and firm financial performance. Business & Society, 43(2), 135–161.

Shi, X., & Xu, Z. (2018). Environmental regulation and firm exports: Evidence from the eleventh Five-Year Plan in China. Journal of Environmental Economics and Management, 89, 187–200.

Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), 571–610.

Tang, K., & Bae, K. S. (2021). Listed local state-owned enterprises and environmental performance: Evidence from China. The Journal of Asian Finance, Economics, and Business, 8(2), 255–262.

Testa, F., Boiral, O., & Iraldo, F. (2018). Internalization of environmental practices and institutional complexity: Can stakeholders pressures encourage greenwashing? Journal of Business Ethics, 147(2), 287–307.

Tu, Z., Hu, T., & Shen, R. (2019). Evaluating public participation impact on environmental protection and ecological efficiency in China: Evidence from PITI disclosure. China Economic Review, 55, 111–123.

Walker, K., & Wan, F. (2012). The harm of symbolic actions and green-washing: Corporate actions and communications on environmental performance and their financial implications. Journal of Business Ethics, 109(2), 227–242.

Walls, J. L., & Hoffman, A. J. (2013). Exceptional boards: Environmental experience and positive deviance from institutional norms. Journal of Organizational Behavior, 34(2), 253–271.

Wu, M. W., & Shen, C. H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance, 37(9), 3529–3547.

Yang, Z., Nguyen, T. T. H., Nguyen, H. N., Nguyen, T. T. N., & Cao, T. T. (2020). Greenwashing behaviours: Causes, taxonomy and consequences based on a systematic literature review. Journal of Business Economics and Management, 21(5), 1486–1507.

Zhao, Y. M., Zhu, F. M., & He, L. L. (2009). Definition, classification and evolution of environmental regulations. China Population Resources and Environment, 19(6), 85–90.

Funding

National Natural Science Foundation of China (Grant No.71972104), China Scholarship Council (Grant No. 202006860022) and the Postgraduate Research and Innovation Program of Jiangsu Province (Grant No. KYCX20_1133).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1: 22 indicators measuring greenwashing

22 indicators | Examples of firm activities taken directly from corporate various reports and its source |

|---|---|

1. Environmental strategy and planning | The company regards environmental protection as the important content of enterprise sustainable development strategy and pays attention to it. To fulfill the responsibility of environmental protection. The company practices environmentally friendly and energy saving development. The company effectively realizes environmental protection and sustainable development through the following measures. Source: 2009 CSR Report of Natural Ingredients Company |

2. Staff training | In order to strengthen environmental protection education, the annual “Six-five” Environment Day and energy conservation publicity week are used to carry out environmental protection publicity work. Various forms such as slogans, boards, questions and answers on energy conservation and environmental protection knowledge are used to promote employees and cultivate their environmental protection awareness. Source: 2012 CSR Report of Huolinhe Opencut Coal Industry Corporation Limited Of Inner of China |

3. Special fund plan | In the dust control of production and transportation roads, 38.4068 million yuan is invested to equip 11 large water sprinklers for dust elimination of production and operation roads. Source: 2012 CSR Report of Huolinhe OpenCut Coal Industry Corporation Limited of Inner Mongolia |

4. Environmental certification | The company has successfully passed the review of ISO/TS16949 quality system certification and obtained ISO14000 environmental protection system certification. Source: 2013 CSR Report of Shenzhen Laibao Hi-Tech Co., Ltd, China |

5. Establishment of the environmental protection department | Air China officially approved the establishment of three full-time environmental affairs positions in the Planning and development Department in 2009. Air China is equipped with part-time energy statisticians in key energy departments. Source: 2009 CSR Report of Air China Limited |

6. Environmental risk analysis | Work closely with professional wastewater treatment units to promote wastewater purification and reuse. Eliminate water pollution from wastewater discharge. Source: The 2012 CSR Report of Air China Limited |

7. Green supplier selection | When the supplier uses both environmental and non-environmental materials, the company shall check whether the two types of materials are clearly distinguished in the storage and processing process, to prevent mutual contamination, and will confirm whether the supplier has confirmed the environmental compliance of the incoming materials. Source: 2008 CSR Report of GuoGuang Electric Company Ltd |

8. Environmental auditing | The company will be environmental protection laws, regulations and the implementation of the company's environmental protection management system, “three waste” emissions, environmental accidents, environmental equipment operation management, etc. into the safety and environmental protection responsibility statement for assessment, effectively control the occurrence of environmental pollution accidents. Source: 2014 CSR Report of Hubei Xinyangfeng Fertilizer Co., Ltd |

9. Participation of environmental organizations | Institute of Public and Environmental Affairs, IPE. The Institute of Public and Environmental Affairs (IPE) is a Non-profit environmental organization registered in Beijing. Since its inception in May 2006, IPE has developed and operated two databases, the China Water Pollution Map and the China Air Pollution Map, to promote environmental information disclosure and public participation, and to improve environmental governance mechanisms. Source: http://www.ipe.org.cn/ |

10. Environmental charity | Zhengtai Electric Company invested 70 million yuan to set up Zhengtai public welfare Fund and has been actively participating in green environmental protection activities. Source: 2013 CSR Report of Zhejiang China Electrics Co., Ltd |

11. Green Business development | In December 2013, the company invested 25 million RMB to acquire the distributed photovoltaic power generation project built on the roof of Haining Leather City. Source: 2013 Annual Report of Haining China Leather Market Co., Ltd |

12. Process improvement | Products in the development and design of low energy consumption, low consumption of materials, choose relatively environmentally friendly raw materials. Taking the development of new “MSMX” products as an example, the material utilization rate is increased by 45% and the energy consumption is reduced by 90%. Source: 2012 CSR Report of Suzhou GOOD-ARK Electronics Co., Limited |

13. Industrial waste | Beijing Ground Service Department strengthens the control of 13 items that can be recycled, and consigns a special recycling team to recycle, sort out, repackage and redistribute 13 items that can be reused. Source: 2012 CSR Report of Air China Limited |

14. Energy saving and | CRRC Corporation Limited implements the important national deployment on energy conservation and emission reduction, promotes the construction of energy management information system, increases the intensity of technological transformation, and vigorously promotes energy conservation and emission reduction. Source: 2012 CSR Report of CRRC Corporation Limited |

15. Technological development | The company's “environmental protection large reserve digital circular material yard system achievement transformation Project” was identified as “Beijing High-tech Achievement transformation Project” in 2015, and obtained special fund support. Meanwhile, it was awarded the title of “Beijing High-tech Achievement Transformation Demonstration Enterprise”. Source: 2015 CSR Report of Huadian Heavy Industries Co. Ltd |

16. cyclic utilization | In 2012, 1.88 million tons of reclaimed water was recycled, with a water recycling rate of 85.9%, realizing 90% of wastewater and sewage treatment, saving production costs, reducing pollution discharge and promoting circular economy. Source: 2012 CSR Report of CRRC Corporation Limited |

17. Pollution monitoring and control | The company started and built the second phase of energy and environment monitoring system to realize the standardized statistics and monitoring function of energy consumption throughout the company. Source: 2012 CSR Report of Air China Limited |

18. Green office | Since 2011, the company has implemented paperless office, saving printing costs and reducing paper waste, which can reduce printing costs for the company by about 5 million yuan per year. Source: 2016 CSR Report of SANY HEAVY INDUSTRY CO., Ltd |

19. Ecological restoration | In 2010, a total of 1704.06 mu of land was reclaimed, and the reclamation rate could reach more than 95%, meeting the requirements of environmental protection and water conservation. Source: 2010 CSR Report of Huolinhe Opencut Coal Industry Corporation Limited of Inner Mongolia |

20. Green marketing | A number of series of environmental protection products developed by Oriental Yuhong have been put into use and created value. 87 types of products in four categories, including waterproof rolling material, waterproof coating, rigid waterproof material and adhesive, have passed the environmental label product certification. Source: 2012 CSR Report of Beijing Oriental Yuhong Waterproof Technology Co., Ltd |

21. Environmental cost accounting | A total of 95.44 million RMB was invested in environmental protection. Among them, mine water treatment is 41.34 million RMB, boiler dust removal 1.46 million RMB, Gangshi mountain treatment is 45.81 million RMB, coal dust treatment is 11.03 million RMB. Source: 2011 CSR Report of Shanxi Xishan Coal and Electricity Power Co., Ltd |

22. Clean energy use | The application of ground source heat pump technology and solar photovoltaic power generation system to make the station a national green project. Source: 2016 CSR Report of China Railway Engineering Group Limited |

Appendix 2: Detailed instructions for measuring greenwashing

Code | Environmental items | STS2: Symbolic environmental information disclosure: How firms only discuss their environmental commitment and self-compliment, without any proof | STS1:Substantial environment information disclosure: What concrete actions, or steps they have taken to care for the natural environment |

|---|---|---|---|

1 | Environmental strategy and planning | General description or not mentioned | Digital quantitative description or certificate proof |

2 | Staff training | Non-disclosure General description or not mentioned | Digital quantitative description or certificate proof |

3 | Special fund plan | General description or no mention | Digital quantitative description or certificate proof |

4 | Environmental certification | General description or no mention | Digital quantitative description or certificate proof |

5 | Establishment of the environmental protection department | General description or no mention | Digital quantitative description or certificate proof |

6 | Environmental risk analysis | General description or no mention | Digital quantitative description or certificate proof |

7 | Green supplier selection | General description or no mention | Digital quantitative description or certificate proof |

8 | Environmental auditing | General description or no mention | Digital quantitative description or certificate proof |

9 | Participation of environmental organizations | General description or no mention | Digital quantitative description or certificate proof |

10 | Environmental charity | General description or no mention | Digital quantitative description or certificate proof |

11 | Green Business development | General description or no mention | Digital quantitative description or certificate proof |

12 | Process improvement | General description or no mention | Digital quantitative description or certificate proof |

13 | Industrial waste discharge management | General description or no mention | Digital quantitative description or certificate proof |

14 | Energy saving and efficiency increasing | General description or no mention | Digital quantitative description or certificate proof |

15 | Technological development | General description or no mention | Digital quantitative description or certificate proof |

16 | Cyclic utilization | General description or no mention | Digital quantitative description or certificate proof |

17 | Pollution monitoring and control | General description or no mention | Digital quantitative description or certificate proof |

18 | Green working | General description or no mention | Digital quantitative description or certificate proof |

19 | Ecological restoration | General description or no mention | Digital quantitative description or certificate proof |

20 | Green market | General description or no mention | Digital quantitative description or certificate proof |

21 | Environmental cost accounting | General description or no mention | Digital quantitative description or certificate proof |

22 | Use of clean energy | General description or no mention | Digital quantitative description or certificate proof |

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Zhang, K., Pan, Z., Janardhanan, M. et al. Relationship analysis between greenwashing and environmental performance. Environ Dev Sustain 25, 7927–7957 (2023). https://doi.org/10.1007/s10668-022-02381-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10668-022-02381-9