Abstract

This paper comprises a survey of a half century of research on international monetary aggregate data. We argue that since monetary assets began yielding interest, the simple sum monetary aggregates have had no foundations in economic theory and have sequentially produced one source of misunderstanding after another. The bad data produced by simple sum aggregation have contaminated research in monetary economics, have resulted in needless “paradoxes,” and have produced decades of misunderstandings in international monetary economics research and policy. While better data, based correctly on index number theory and aggregation theory, now exist, the official central bank data most commonly used have not improved in most parts of the world. While aggregation theoretic monetary aggregates exist for internal use at the European Central Bank, the Bank of Japan, and many other central banks throughout the world, the only central banks that currently make aggregation theoretic monetary aggregates available to the public are the Bank of England and the St. Louis Federal Reserve Bank. No other area of economics has been so seriously damaged by data unrelated to valid index number and aggregation theory. In this paper we chronologically review the past research in this area and connect the data errors with the resulting policy and inference errors. Future research on monetary aggregation and policy can most advantageously focus on extensions to exchange rate risk and its implications for multilateral aggregation over monetary asset portfolios containing assets denominated in more than one currency. The relevant theory for multilateral aggregation with exchange rate risk has been derived by Barnett (J Econom 136(2):457–482, 2007) and Barnett and Wu (Ann Finance 1:35–50, 2005).

Similar content being viewed by others

Notes

In aggregation theory measurement error refers to the tracking error in a nonparametric index number’s approximation to the aggregator function of microeconomic theory, where the aggregator function is the subutility or subproduction function that is weakly separable within tastes or technology of an economic agent’s complete utility or production function. Consequently, aggregator functions are increasing and concave and need to be estimated econometrically. On the other hand, state space models use the term measurement error to mean un-modeled noise, which is not captured by the state variable or idiosyncratic terms. In this paper, measurement error refers to this latter definition, which can be expected to be correlated with the former, when the behavior of the data process is consistent with microeconomic theory. But it should be acknowledged that neither concept of measurement error can be directly derived from the other. In fact the state space model concept of measurement error is more directly connected with the statistical (“atomistic”) approach to index number theory than to the more recent “economic approach,” which is at its best when data is not aggregated over economic agents.

Subsequently Barnett (1987) derived the formula for the user cost of supplied monetary services. A regulatory wedge can exist between the demand and supply-side user costs, if non-payment of interest on required reserves imposes an implicit tax on banks.

Our research in this paper is not dependent upon this simple decision problem, as shown by Barnett (1987), who proved that the same aggregator function and index number theory applies, regardless of whether the initial model has money in the utility function, or money in a production function, or neither, so long as there is intertemporal separability of structure and certain assumptions are satisfied for aggregation over economic agents. The aggregator function is the derived function that has been shown in general equilibrium always to exist, if money has positive value in equilibrium, regardless of the motive for holding money.

The multilateral open economy extension is available in Barnett (2007).

To be an admissible quantity aggregator function, the function u must be weakly separable within the consumer’s complete utility function over all goods and services. Producing a reliable test for weak separability is the subject of much intensive research, most recently by Barnett and de Peretti (2008).

In Eq. (4), it is understood that the result is in continuous time, so the time subscripts are a short hand for functions of time. We use t to be the time period in discrete time, but the instant of time in continuous time.

Diewert (1976) defines a ‘superlative index number’ to be one that is exactly correct for a quadratic approximation to the aggregator function. The discretization (7) to the Divisia index is in the superlative class, since it is exact for the quadratic translog specification to an aggregator function.

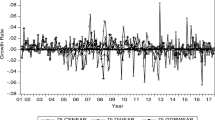

The Federal Reserve Bank of St. Louis Divisia database, which we use in this paper, is not risk corrected. In addition, it is not adjusted for differences in marginal taxation rates on different asset returns or for sweeps, and its clustering of components into groups was not based upon tests of weak separability, but rather on the Federal Reserve’s official clustering. The St. Louis Federal Reserve Bank is in the process of revising its MSI database, perhaps to incorporate some of those adjustments. Regarding sweep adjustment, see Jones et al. (2005). At the present stage of this research, we felt it was best to use data available from the Federal Reserve for purposes of replicability and comparability with the official simple sum data. As a result, we did not modify the St. Louis Federal Reserve’s MSI database or the Federal Reserve Board’s simple sum data in any ways. This decision should not be interpreted to imply advocacy by us of the official choices.

References

Anderson R, Jones B, Nesmith T (1997a) Introduction to the St. Louis monetary services index project. Fed Reserve Bank St. Louis Rev 79(1):25–30, January/February

Anderson R, Jones B, Nesmith T (1997b) Building new monetary services indexes: concepts data and methods. Fed Reserve Bank St. Louis Rev 79(1):53–82, January/February

Barnett WA (1978) The user cost of money. Econ Lett 1:145–149. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 1. North Holland, Amsterdam, pp 6–10

Barnett WA (1980) Economic monetary aggregates: an application of aggregation and index number theory. J Econom 14:11–48. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 1. North Holland, Amsterdam, pp 6–10

Barnett WA (1982) The optimal level of monetary aggregation. J Money Credit Bank 14:687–710. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 7. North Holland, Amsterdam, pp 125–149

Barnett WA (1983) Understanding the New Divisia monetary aggregate. Rev Public Data Use 11:349–355. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 4. North Holland, Amsterdam, pp 100–108

Barnett WA (1984) Recent monetary policy and the Divisia monetary aggregates. Am Statist 38:162–172. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 23. North Holland, Amsterdam, pp 563–576

Barnett WA (1987) The microeconomic theory of monetary aggregation. In: Barnett WA, Singleton K (eds) New approaches to monetary economics. Cambridge U. Press. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 3. North Holland, Amsterdam, pp 49–99

Barnett WA (1997) Which road leads to stable money demand? Econ J 107:1171–1185. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 24. North Holland, Amsterdam, pp 577–592

Barnett WA (2000) A reply to Julio J. Rotemberg. In: Belongia MT (ed) Monetary policy on the 75th anniversary of the federal reserve system. Kluwer, Boston, pp 232–244 (1991). Reprinted in Barnett WA, Serletis A (eds) The theory of monetary aggregation. North Holland, Amsterdam

Barnett WA (2007) Multilateral aggregation-theoretic monetary aggregation over heterogeneous countries. J Econom 136(2):457–482. doi:10.1016/j.jeconom.2005.11.004

Barnett WA, de Peretti P (2008) A necessary and sufficient stochastic semi-nonparametric test for weak separability. Macroeconomic Dyn in press

Barnett WA, Hahm JH (1994) Financial firm production of monetary services: a generalized symmetric Barnett variable profit function approach. J Bus Econ Stat 12:33–46. Reprinted in Barnett WA, Binner J (eds) (2004) Functional structure and approximation in econometrics, chapter 15. North Holland, Amsterdam, pp 351–380

Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation. Contributions to economic analysis monograph series. Elsevier, Amsterdam

Barnett WA, Wu S (2005) On user costs of risky monetary assets. Ann Finance 1:35–50. doi:10.1007/s10436-004-0003-6

Barnett WA, Xu H (1998) Stochastic volatility in interest rates and nonlinearity in velocity. Int J Syst Sci 29:1189–1201. doi:10.1080/00207729808929608

Barnett WA, Zhou G (1994a) Partition of M2+ as a joint product: commentary. Fed Reserve Bank St. Louis Rev 76:53–62

Barnett WA, Zhou G (1994b) Financial firm’s production and supply-side monetary aggregation under dynamic uncertainty. Fed Reserve Bank St. Louis Rev March/April, 133–165. Reprinted in Barnett WA, Binner J (eds) (2004) Functional structure and approximation in econometrics, chapter 16. North Holland, Amsterdam, pp 381–427

Barnett WA, Offenbacher EK, Spindt PA (1984) The New Divisia monetary aggregates. J Polit Econ 92:1049–1085. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 17. North Holland, Amsterdam, pp 360–388

Barnett WA, Hinich MJ, Weber WE (1986) The regulatory wedge between the demand-side and supply-side aggregation-theoretic monetary aggregates. J Econom 33:165–185. Reprinted in Barnett WA, Serletis A (eds) (2000) The theory of monetary aggregation, chapter 19. North Holland, Amsterdam, pp 433–453

Barnett W, Fisher D, Serletis A (1992) Consumer theory and the demand for money. J Econ Lit 30:2086–119. Reprinted in Barnett and Serletis (2000, ch. 18)

Barnett WA, Liu Y, Jensen M (1997) CAPM risk adjustment for exact aggregation over financial assets. Macroeconomic Dyn 1:485–512

Barnett WA, Chae U, Keating J (2006) The discounted economic stock of money with VAR forecasting. Ann Finance 2(2):229–258. doi:10.1007/s10436-006-0038-y

Barnett WA, Chauvet M, Tierney HLR (2008) Measurement error in monetary aggregates: a markov switching factor approach. Macroeconomic Dyn in press

Batchelor R (1989) A monetary services index for the UK. Mimeo, Department of Economics, City University, London

Belongia M (1996) Measurement matters: recent results from monetary economics reexamined. J Polit Econ 104(5):1065–1083. doi:10.1086/262052

Belongia M, Binner J (eds) (2000) Divisia monetary aggregates: theory and practice. Palgrave, Basingstoke

Belongia M, Chrystal A (1991) An admissible monetary aggregate for the United Kingdom. Rev Econ Stat 73:497–503. doi:10.2307/2109574

Belongia M, Ireland P (2006) The own-price of money and the channels of monetary transmission. J Money Credit Bank 38(2):429–445. doi:10.1353/mcb.2006.0025

Chauvet M (1998) An econometric characterization of business cycle dynamics with factor structure and regime switches. Int Econ Rev 39(4):969–996. doi:10.2307/2527348

Chauvet M (2001) A monthly indicator of Brazilian GDP. In: Brazilian Review of Econometrics vol. 21, no. 1

Chrystal A, MacDonald R (1994) Empirical evidence on the recent behaviour and usefulness of simple-sum and weighted measures of the money stock. Fed Reserve Bank St. Louis Rev 76:73–109

Cockerline J, Murray J (1981) A comparison of alternative methods for monetary aggregation: some preliminary evidence. Technical Report #28, Bank of Canada

Diewert W (1976) Exact and superlative index numbers. J Econom 4:115–145. doi:10.1016/0304-4076(76)90009-9

Divisia F (1925) L’Indice monétaire et la théorie de la monnaie. Rev Econ Polit 39:980–1008

Drake L (1992) The substitutability of financial assets in the U. K. and the implication for monetary aggregation. Manchester Sch Econ Soc Stud 60:221–248. doi:10.1111/j.1467-9957.1992.tb00462.x

Fase M (1985) Monetar control: the Dutch experience: some reflections on the liquidity ratio. In: van Ewijk C, Klant JJ (eds) Monetary conditions for economic recovery. Martinus Nijhoff, Dordrecht, pp 95–125

Fisher I (1922) The making of index numbers: a study of their varieties, tests, and reliability. Houghton Mifflin, Boston

Friedman M, Schwartz A (1970) Monetary statistics of the United States: estimation, sources, methods, and data. Columbia University Press, New York

Goldfeld SM (1973) The demand for money revisited. Brookings Pap Econ Act 3:577–638. doi:10.2307/2534203

Hicks JR (1946) Value and capital. Clarendon, Oxford

Hoa TV (1985) A Divisia system approach to modelling monetary aggregates. Econ Lett 17:365–368. doi:10.1016/0165-1765(85)902600-5

Ishida K (1984) Divisia monetary aggregates and the demand for money: a Japanese case. Bank Jpn Monetary Econ Stud 2:49–80

Jones B, Dutkowsky D, Elger T (2005) Sweep programs and optimal monetary aggregation. J Bank Finance 29:483–508. doi:10.1016/j.jbankfin.2004.05.016

Kim CJ, Nelson C (1998) State-space models with regime-switching: classical and Gibbs-sampling approaches with applications. The MIT Press

Lucas RE (1999) An interview with Robert E. Lucas, Jr., interviewed by Bennett T. McCallum. Macroecon Dyn 3:278–291. Reprinted in Samuelson PA, Barnett WA (eds) (2006) Inside the economist’s mind. Blackwell, Malden, MA

Lucas RE (2000) Inflation and welfare. Econometrica 68(62):247–274. doi:10.1111/1468-0262.00109

Serletis A (ed) (2006) Money and the economy. World Scientific

Schunk D (2001) The relative forecasting performance of the Divisia and simple sum monetary aggregates. J Money Credit Bank 33(2):272–283. doi:10.2307/2673885

Swamy PAVB, Tinsley P (1980) Linear prediction and estimation methods for regression models with stationary stochastic coefficients. J Econom 12:103–142. doi:10.1016/0304-4076(80)90001-9

Yue P, Fluri R (1991) Divisia monetary services indexes for Switzerland: are they useful for monetary targeting? Fed Reserve Bank St. Louis. Rev 73:19–33

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Barnett, W.A., Chauvet, M. International Financial Aggregation and Index Number Theory: A Chronological Half-century Empirical Overview. Open Econ Rev 20, 1–37 (2009). https://doi.org/10.1007/s11079-008-9099-z

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-008-9099-z

Keywords

- Measurement error

- Monetary aggregation

- Divisia index

- Aggregation

- Monetary policy

- Index number theory

- Exchange rate risk

- Multilateral aggregation

- Open economy monetary economics