Abstract

This paper investigates how individuals evaluate delayed outcomes with risky realization times. Under the discounted expected utility (DEU) model, such evaluations depend only on intertemporal preferences. We obtain several testable hypotheses using the DEU model as a benchmark and test these hypotheses in three experiments. In general, our results show that the DEU model is a poor predictor of intertemporal choice behavior under timing risk. We found that individuals are averse to timing risk and that they evaluate timing lotteries in a rank-dependent fashion. The main driver of timing risk aversion is nothing but probabilistic risk aversion that stems from the nonlinear treatment of probabilities.

Similar content being viewed by others

Notes

Throughout this paper, we will refer to those situations where the decision maker has more than one possible delay as risky timing or risky delays since we investigate delays with known (objective) probabilities.

In another study, Leclerc, Schmitt and Dubé (1995) focused on risky decision making for waiting times, examining those situations where time itself is a resource. That is, they were interested in the value of time. In the current study, we are interested in the changes in an outcome’s value as time changes. Thus, our problem is about time preferences rather than the utility for time.

We assume that x is a desirable outcome, that is, the decision maker’s utility u(.) is an increasing function of x.

We will refer to a generalized discounted utility model where the discount function can take any form as a discounted expected utility (DEU) model hereafter.

To see this, consider the following inequalities: \( pD{\left( {t_{1} } \right)} + {\left( {1 - p} \right)}D{\left( {t_{2} } \right)} \geqslant \alpha D{\left( {t_{1} } \right)} + {\left( {1 - \alpha } \right)}D{\left( {t_{2} } \right)} \), since p ≥ α and \( \alpha D{\left( {t_{1} } \right)} + {\left( {1 - \alpha } \right)}D{\left( {t_{2} } \right)} > D{\left( {\alpha t_{1} + {\left( {1 - \alpha } \right)}t_{2} } \right)} \), due to convexity of D(.). These two inequalities together would imply \( pD{\left( {t_{1} } \right)} + {\left( {1 - p} \right)}D{\left( {t_{2} } \right)} - D{\left( {\alpha t_{1} + {\left( {1 - \alpha } \right)}t_{2} } \right)} > 0 \) for all p ≥ α.

At the time of the experiment, 1 New Turkish Lira was approximately 0.625 Euro.

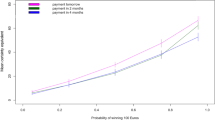

The scenario that we used in the loss domain was similar. In that scenario, participants were asked to imagine that they were going to pay a tax and they could choose between the two timing options.

Our interpretation of the Likert scale is strictly ordinal. We use the scale to allow subjects to express indifference between the two options and to check for within-subject consistency.

Experimental instructions are available from the authors upon request.

We imposed a concave utility function u(x) = x 0.88 to calculate the average monthly discount rates. We used the formula \( {\left( {e^{{ - r_{i} T}} } \right)}X^{{0.88}} = {\text{PV}}^{{0.88}}_{i} \) where T is the number of months, X is the delayed amount, PV i is the present value by participant i and r i is the average monthly discount rate of participant i.

This follows from variability ordering. For L 1, L 2 ≥ 0 such that E[L 1 ] = E[L 2 ], L 1 is more variable than L 2 if and only if E[h(L 1 )] ≥ E[h(L 2 )] for all convex h (Ross 1996).

If L 1 and L 2 are nonnegative random variables with distributions F and G, respectively, then L 1 is more variable than L 2 if and only if \( {\int_a^\infty {{\left( {1 - F{\left( x \right)}} \right)}{\text{d}}x \geqslant } }{\int_a^\infty {{\left( {1 - G{\left( x \right)}} \right)}{\text{d}}x} } \) for all ≥ 0 (see Ross 1996).

References

Ahlbrecht, Martin, and Martin Weber. (1997). “An Empirical Study on Intertemporal Decision Making Under Risk,” Management Science 43, 813.

Benzion, Uri, Amnon Rapoport, and Joseph Yagil. (1989). “Discount Rates Inferred from Decisions: An Experimental Study,” Management Science 35, 270–284.

Birnbaum, Michael H. (1992). “Violations of Monotonicity and Contextual Effects in Choice-based Certainty Equivalents,” Psychological Science 3, 310–314.

Chesson, Harrell, and W. Kip Viscusi. (2000). “The Heterogeneity of Time-risk Tradeoffs,” Journal of Behavioral Decision Making 13, 251–258.

Chesson, Harrell, and W. Kip Viscusi. (2003). “Commonalities in Time and Ambiguity Aversion for Long-term Risks,” Theory and Decision 54, 57–71.

Dasgupta, Partha, and Eric Maskin. (2005). “Uncertainty and Hyperbolic Discounting,” American Economic Review 95(4), 1290–1299.

Frederick, Shane, George Loewenstein, and Ted O’Donoghue. (2002). “Time Discounting and Time Preference: A Critical Review,” Journal of Economic Literature 40, 351–401.

Gonzalez, Richard, and George Wu. (1999). “On the Shape of the Probability Weighting Function,” Cognitive Psychology 38(1), 129.

Ho, Joanna L., and Soo Hong Chew. (1994). “Hope: An Empirical Study of Attitude Toward the Timing of Uncertainty Resolution,” Journal of Risk and Uncertainty 8(3), 267–288.

Kacelnik, Alex, and Melissa Bateson. (1996). “Risky Theories—The Effects of Variance in Foraging Decisions,” Integrative and Comparative Biology 36(4), 402–434.

Koopmans, Tjalling C. (1960). “Stationary Ordinal Utility and Impatience,” Econometrica 28, 287–309.

Leclerc, France, Bernd H. Schmitt and Laurette Dubé. (1995). “Waiting Time and Decision Making: Is Time Like Money?” Journal of Consumer Research 22, 110–119.

Loewenstein, George, and Drazen Prelec. (1992). “Anomalies in Intertemporal Choice: Evidence and an Interpretation,” Quarterly Journal of Economics 107(2), 573.

Mazur, James E. (1987). “An Adjustment Procedure for Studying Delayed Reinforcement.” In Michael L. Commons, James E. Mazur, John A. Nevin and Howard Rachlin (eds.), The Effect of Delay and Intervening Events on Reinforcement Value. Hillsdale, NJ: Erlbaum.

Mossin, Jan. (1969). “A Note on Uncertainty and Preferences in a Temporal Context,” American Economic Review 59, 172–174.

Perrakis, Stylianos, and Claude Henin. (1974). “The Evaluation of Risky Investments with Random Timing of Cash Returns,” Management Science 21(1), 79–86.

Perrakis, Stylianos, and Izzet Sahin. (1976). “On Risky Investments with Random Timing of Cash Returns and Fixed Planning Horizon,” Management Science 22(7), 799–809.

Prelec, Drazen. (1998). “The Probability Weighting Function,” Econometrica 66, 497.

Quiggin, John. (1982). “A Theory of Anticipated Utility,” Journal of Economic Behavior and Organization 3, 323–343.

Read, Daniel. (2005). “Monetary Incentives, What are They Good for?” Journal of Economic Methodology 12(2), 265–267.

Ross, Sheldon M. (1996). Stochastic Processes (2nd ed.). New York: Wiley.

Sagristano, Michael D., Yaacov Trope and Nira Liberman. (2002). “Time-dependent Gambling: Odds Now, Money Later,” Journal of Experimental Psychology: General 131(3), 364.

Samuelson, Paul. (1937). “A Note on Measurement of Utility,” Review of Economic Studies 4, 155–161.

Slovic, Paul, Dale Griffin and Amos Tversky. (1990). “Compatibility Effects in Judgement and Choice.” In Robin M. Hogarth (ed.), Insights in Decision Making: A Tribute to Hillel J. Einhorn. Chicago: University of Chicago Press.

Spence, Michael, and Richard Zeckhauser. (1972). “The Effect of the Timing of Consumption Decisions and the Resolution of Lotteries on the Choice of Lotteries,” Econometrica 40(2), 401–403.

Thaler, Richard. (1981). “Some Empirical Evidence on Dynamic Inconsistency,” Economic Letters 8, 201–207.

Tversky, Amos, and Daniel Kahneman. (1981). “The Framing of Decisions and the Rationality of Choice,” Science 211, 453–458.

Tversky, Amos, and Daniel Kahneman. (1992). “Advances in Prospect Theory: Cumulative Representation of Uncertainty,” Journal of Risk and Uncertainty 5, 297–323.

Tversky, Amos, Shmuel Sattath and Paul Slovic. (1988). “Contingent Weighting in Judgment and Choice,” Psychological Review 95(3), 371–384.

Wakker, Peter. (1994). “Separating Marginal Utility and Probabilistic Risk Aversion,” Theory & Decision 36(1), 1.

Wu, George, and Richard Gonzalez. (1996). “Curvature of the Probability Weighting Function,” Management Science 42(12), 1676–1690.

Acknowledgments

The authors would like to thank Onur Boyabatli, Philippe Delquie, participants at the 2006 Workshop on Decision-Making and Utility, the editor and an anonymous referee for their helpful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Onay, S., Öncüler, A. Intertemporal choice under timing risk: An experimental approach. J Risk Uncertainty 34, 99–121 (2007). https://doi.org/10.1007/s11166-007-9005-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11166-007-9005-x