Abstract

Certain developed countries have experienced the ‘peak car’ phenomenon. While this remains to be confirmed longitudinally, it looks certain that future mobility in Europe and elsewhere will be shaped by a particular technological development: driverless or autonomous transport. The ‘autonomous car’ ignites the imagination, yet the research and debate on this topic largely focus on the ‘autonomous’ and not adequately on the ‘car’ element. Like any new technological development, autonomous transport presents ample opportunities to better our mobility system, but similarly it carries risks and can lead into a future mobility that exacerbates, rather than relieves, current deficiencies of our mobility systems, including its high carbon and high cost characteristics. Now it is high time to explore these, before we lock ourselves into the autonomous car future. Using Low Carbon Mobility (LCM) as a guiding framework to assess mobility patterns and based on an extensive literature review, this paper aims to explore where there is a gap between the likely and desirable outcomes when developing the autonomous car and suggest how we might reduce it. Moreover, enhancing on global empirical evidence and forecasts about the opportunities and threats emerging from ICT deployment in transport and initial evidence on the development of the autonomous car, the paper concludes that a desirable outcome will only come if technological development will be accompanied by a social change. A change where public and sharing will be seen as superior to private and individual transport, could make the autonomous car a blessing.

Similar content being viewed by others

Introduction

The ‘peak car’ phenomenon caught the transport and mobility research community by surprise. In several countries, travel surveys at national level suggest that car use in recent years has stopped growing and even declined [1, 2], including countries such as the US which is the champion of private car reliance. Other countries where such a phenomenon has been observed include France, Germany, Great Britain, Japan and Norway. Researchers are beginning to recognise a drop in licensing in Australia, North America, Japan, and most of Europe and are pondering the implications of this for future mobility trends and for current transport policy [3] (see also Special Issue of Transport Reviews, Vol. 33 Is. 3).

Even if still limited to relatively few countries and a trend spanning a relatively short period of time (10–20 years), the observed changing propensity of people to drive can mark a dramatic change in the way we as a society prefer to move. Stokes [4] argues that given what is known about ‘peak car’ we cannot forecast with any certainty future levels of car use, and a number of different futures are plausible, which could lead to a rise, a fall, or stability in levels of car travel. While intriguing, the ‘peak car’ phenomenon, especially in the countries already experiencing it, is likely to be a short lived phenomenon due to an imminent development in transport technology, which will mark the next transport revolution.Footnote 1 This new technology is the Autonomous Vehicle (AV), also known as the self-driven or driverless car.

According to the US Department of Transportation’s National Highway Traffic Safety Administration (NHTSA): “self-driving vehicles are those in which operation of the vehicle occurs without direct driver input to control the steering, acceleration, and braking and are designed so that the driver is not expected to constantly monitor the roadway while operating in self-driving mode”[6]. Their automation can be defined according to five levels (see [6] for details). Currently we are at levels 2–3 but the vision is to reach level 4 within the next two decades and this forms the basis of this paper. In this context, it is important to understand that for a vehicle to qualify as fully autonomous, it should be able to navigate itself in real traffic within roads which have not been specifically adapted for its use, but this does not mean that there will not be broader modifications to road infrastructure to accommodate the AVs. Through the use of V2I (vehicle-to-infrastructure)Footnote 2 and V2V (vehicle-to-vehicle)Footnote 3 communication which will require adaptation of both road infrastructure and vehicles, AVs will be able to navigate in complex urban environments.

Given the fact that 54 % of the global population currently lives in cities and is responsible for 64 % of total kilometres travelled or 10 billion trips daily, along with the projection that 66 % of the global population will live in cities by 2050 increasing urban kilometres travelled threefold [2, 8], the AV is in every aspect a ‘game changer’ that can modify beyond recognition our transport and mobility system and as a consequence our life. Combined with the ‘peak car’ phenomenon, which can for example be observed in London, where private transport mode use has peaked around 2001 and has been decreasing since [9], AVs could further secure—even enhance—private car mobility by navigating autonomously within our citiesFootnote 4. At the same time, AVs offer a unique opportunity to de-privatise car use. We see the former option as a curse and the latter as a blessing and debate them from different perspectives in this paper. Society in general and transport planners in particular must prepare for the forthcoming era. During these preparations there are choices to be made and there are opportunities to seize, alongside many pitfalls to avoid. This paper adopts Low Carbon Mobility as the theoretical framework to achieve its objective, employing an extensive literature review and a contrast of the likely and desirable outcomes of a mobility system relying on AV technology.

The remainder of the paper is structured as follows: the second section provides background facts and reviews contemporary schemes along with an overview of potential challenges to be faced by the automotive industry; the third section summarises benefits and threats of AVs deployment, whilst the fourth section provides evidence from London regarding approaches and attitudes towards compact urban development and electric or shared vehicles. This paves the way for the fifth section which elaborates the key argument of this paper shedding light on whether the autonomous car is a panacea or not, distinguishing likely from desirable outcomes and offering recommendations for policy makers, practitioners as well as suggestions for future research.

The wider context surrounding autonomous cars

Moving towards low carbon mobility

Our mobility can be described as high-carbon, where carbon serves as a proxy to a wide range of environmental impacts associated with the way we travel and other negative conditions such as obesity and sedentary lifestyle inherited by our reliance and use of the private car. Low carbon mobility, on the other hand, is defined as mobility that results in substantially lower levels of carbon emissions and can be considered as the ultimate goal for transport policy, planning as well as research [10]. Hardly anyone will argue against the need to move towards low carbon mobility, but there is hardly any agreement on the optimal way to achieve it.

Givoni [11] suggests three generic pathways to reach low carbon mobility (summarised below and in Table 1) and these can also be seen as three different contexts to adopt and absorb AVs into the transport system. The assumptions underpinning the suggested pathways are that the current high carbon mobility can be explained as follows: governments’ key concern is to secure economic growth; investment in transport infrastructure is believed to be a key factor in facilitating such growth; and currently an increase in demand for transport (freight and passenger) is directly linked with increasing emissions. In principle, to achieve low carbon mobility these three elements (economic growth, demand for transport, and emissions from transport) need to be decoupled.

Currently the AV, and most of the research surrounding it, is probably the most outstanding example of Pathway A, where all efforts are focused on technological developments to decouple mobility from emission of Green House Gases (GHG) and air pollutants. Even if the AV technology as such is not addressing the environmental impact of transport, it is seen as offering the possibility to ‘green’ transport (see Benefits and threats of future mobility patterns section for more elaboration). In Pathway B, low carbon mobility is achieved by decoupling economic growth from the demand for transport—largely by focusing on localization and on reducing distances travelled (the global element of society will remain—hence glocalization). Since accessibility may be increased either by increasing velocity (i.e., quicker access to destinations) or proximity (i.e., closer location of destination), it is obvious that corresponding decisions can lead to different outcomes. In the US for example it has been found that solely by doubling urban density within metropolitan regions, vehicle kilometres travelled (VKT) can be reduced by up to 25 % if employment locations are also concentrated spatially [12]. Therefore, a new lifestyle approach is advocated in Pathway C, which questions the merit of constantly pursuing economic growth. Focusing instead on improving well-being, which means decoupling wellbeing from economic growth, can act as the means to secure low carbon mobility.

The LCM framework corresponds well with the automobile dependence and ‘peak car’ arguments [3, 13], which promote a paradigm change in transport planning. The ‘peak car’ theory suggests that “trends in car ownership and use in developed economies […] have passed a turning point and are now in long term decline” [14]. Metz [15] stated that urbanization and socio-demographics will play a key role in the future determining car use as showcased in developed cities which have reached that level, for example London. Focusing on developed countries with available data, only Finland, Israel and The Netherlands experienced small increases (<1 % annually) in the driving license registrations of young people, whereas all other developed countries experienced decreases [16]. Ageing and the role of young adults at an age eligible to acquire a driving license are key factors influencing synchronous trends in France, Germany, the US and the UK, and will continue to do so in the future [17, 18]. Despite it being unclear why the ‘peak car’ phenomenon is observed in developed countries whilst developing countries are projected to increase their car ownership levels (Fig. 1), it is certainly clear that AVs have the potential to revert such trends and reintroduce car use for all age groups irrespectively on whether they own a license or not [17, 20]. How the latter trend is managed in the future could alter car traffic forecasts currently based on the ‘predict and provide’ model and have a substantial impact on car use. In trying to explain ‘peak car’, attention seems to focus on lifestyle and attitudinal factors [3], and this is likely to be critical in aligning the likely and the desirable outcomes of the development of the AV.

Global passenger car ownership trends—Source: [19]

The AV’s anticipated potential

The potential annual quantified benefits from the use of AVs has been estimated at US$1.3 trillionFootnote 5 for the USA, which will come from productivity gains (US$507bn), reduction in accident costs (US$488bn),fuel cost savings due to route optimization (US$158bn), reduction in congestion related fuel loss (US$11bn). This equals around 75 % of the total transport related GDP according to the United States Department of Transportation. Such savings could generate funds to be used for other policy aims since they could reach 8 % of US GDP. Extrapolated at a global scale, this could yield global annual savings of US$5.6 trillion. Of equal importance could be the productivity gains which could be over US$500 billion annually since total time spent driving in the US is around 75 billion hours per year [21]. Reductions in transport costs of about 90 % have been cited in the past [22], so such figures may be remarkable but not surprising.

This anticipated potential has triggered global interest about AVs and autonomous cars in particular. Suggestions vary from conceptual ones such as SuperLev [23] to experimental ones such as the Google self-driving car and initiatives to date including some pilot vehicles. SuperLev is an innovative suggestion simulated in Brazil which aims to make autonomous public transport more convenient and user friendly. It consists of a system of autonomous vehicles which travel in a group similarly to a train to achieve aerodynamic efficiency, but they can leave the group moving in separate directions at particular points on the main line. Travel speed can be up to three times higher compared to conventional rail services, whereas infrastructure costs would be three times less than conventional underground rail services. It is based on the application of superconducting levitation by the use of contactless mechanical components which convert torque into movement through magnets [24, 25], and it increases efficiency while reducing fuel consumption and emissions. Ultimately, its gains are achieved by allowing vehicles to travel together while still having the autonomy to reach specific destinations individually [23].

Equally futuristic plans were in place for the new city of Masdar in Abu Dhabi where the 2getthereFootnote 6 Personal Rapid Transit (PRT),Footnote 7 one of the first forms of autonomous public transport realised, was initially planned to be used across the city. Yet, due to the global economic crisis and after revisiting transport plans and requirements for grid connected vehicles [27], the plan was amended to offer PRT only as a pilot scheme, but there is still a commitment to deliver a public transport fleet serving the city centre which will only use ‘clean’ energy [28, 29]. Despite the first PRT having been introduced in Morgantown, West Virginia in 1975, it is only in the past few years that three small test schemes have been launched in Masdar, Heathrow airport and Suncheon in South Korea [30, 31]. Following this trend, a 6-month pilot scheme has been launched in The Netherlands in 2015 linking Ede train station with Wageningen University [32], whilst LUTZ has been launched in Milton Keynes [33] and GATEway has created a consortium of local authorities, companies and research institutions to explore the technological, cultural, societal and legal challenges of AVs in Greenwich [34]. Similarly, Gothenburg aims to have 100 self-driven cars in 2017 through Drive Me. Consequently, it is apparent that AVs have a significant potential which is already being tested worldwide.

While not questioning the merits of the above estimates and research, there is a need to be aware of a technological optimism bias [35]—in part influenced by commercial opportunities—and acknowledge risk and uncertainty, in large parts stemming from likely unintended effects (see section Choosing between the blessing and the curse).

The industry perspective

As anticipated, the automotive industry could be transformed within the next decade due to this evolution, so corporations have also been exploring autonomous mobility. Interestingly though, those focusing on autonomous cars vary significantly, from traditional car manufacturing firms (e.g., Audi, Renault, Volkswagen, Volvo) to newly established ones manufacturing electric cars (e.g., Tesla) or global software firms (e.g., Apple, Google) with no prior experience in this industry. Expectations at the moment are for fully autonomous cars to be deployed after 2019 [36–39].

It appears that future cars will consist of two major components: hardware and software. Integrating processes, assembling materials and providing user support could resemble the contemporary format of the Information and Communication Technology (ICT) industry, e.g., smartphones [21]. The software element explains the rationale behind autonomous car initiatives by software corporations, but it also highlights the need for common international frameworks, first to test such vehicles and then to make them available for public use. Coordinating diverse objectives and at the same time meeting wider policy targets arises as future challenges [17, 40].

Finding solutions to such challenges is of high importance since widespread use of AVs can trigger innovation in other industries too, such as sensor use, semiconductors, computer vision, 3D measurement, remote control algorithms, and human gestures tracking. Thus, autonomous systems including AVs have been included in the ‘eight great technologies’ of manufacturing in the UK [41]. More broadly though, there are potential impacts on several auto industries. Freight transport will be among the ‘early adopters’ of AVs and a conservative estimate of the respective benefits to this industry is US$168bn annually, whilst TV media and telecommunication industries are also anticipated to benefit [21]. It is crucial to stress here though that regional, national and international subsidies offered for car manufacturing and car use, namely export and fuel subsidies, could be diverted to target AVs and facilitate their wider use. Nonetheless, the market structure can affect outcomes, depending on whether it is a private monopoly, perfect competition or publicly supplied [42]. At the same time, especially from the low carbon mobility perspective, it must be questioned if such subsidies should not go elsewhere in the transport system (e.g., subsidizing electric bicycles) or even other sectors (e.g., health, education). Nonetheless, how this can be achieved remains a challenge since oil rich countries still subsidise—with over US$291 billion per year globally—fuel use, heavily benefitting (61.3 %) the top income quintile [2]. To address such challenges, it has been proposed in the UK to introduce a Minister for driverless cars as responsibility is currently shared among two Ministers. Moreover, a national strategy of deployment assessing wider impacts through pilot trials in Bristol, Coventry, Greenwich and Milton Keynes has been established, which will augment collaboration between industry, academia and government agencies [43, 44]. Individual states are leading change in the US, with four states aside the District of Columbia having introduced legislation allowing AVs on their roads [45] and opening up opportunities for the global automotive industry. The fundamental question still pending though is what the main benefits and threats of investment in AVs are, and how these are shared across society.

Autonomous cars might be ‘green’, mainly by being ‘electric’ thus an important contributor to low carbon mobility. However, even if this is a possible and most desirable outcome, it is by no means guaranteed, although it is often taken for granted. Developing the Electric Vehicle (EV) technology, even if done in parallel to the development of AVs, is a fundamentally different technology and a different technological development trajectory that has its own formidable challenges. It might align, or it might not, with AVs’ development. Thus, it might turn out to be that the autonomous car will not be electric—an outcome most likely determined by the industry. If we assume that the autonomous cars will be electric, the source of electricity used to power them may not be from an environmentally friendly source. Likewise, electric cars’ battery autonomyFootnote 8 and safe disposal at the end of battery life are contemporary concerns of the automotive industry. Finally, vested interests and fossil fuel subsidies may distort markets [2] and the potential uptake of such otherwise environmentally friendly initiatives, such as the electric autonomous cars.

Benefits and threats of future mobility patterns

Global megatrends such as urbanization, globalization, population growth and aging, increasing social disparities, along with a decrease of European Union fossil fuel reserves as part of the world share to a shrinking 1.3 %—projected to be exhausted by 2030—are influencing emerging mobility patterns, largely based on technological advancements and ICT connectivity [19]. These are anticipated to shape decisively the future of transport and AVs in particular, offering benefits but also establishing threats if not taken into account and addressed at an early stage [35, 46]. Since no comprehensive tests, models or deployment have taken place at a large scale to date, it is not possible currently to extrapolate any trend at sufficient confidence levels [47]. Therefore this section reviews contemporary and upcoming patterns to offer an overview of the potential future mobility outlook and the respective impact groups (Table 2).

Benefits

Safety is of paramount importance when assessing the benefits of autonomous cars given that there are more than a million road fatalities globally each year [48]. An anticipated outcome of AVs is less traffic accidents due to reduced human intervention and also increased personal safety due to the option to monitor one’s journey through GPS and connected devices. The latter may be evident in both private cars and public transport [49], though there are ethical concerns regarding the algorithms to be used for accident prevention. The deriving benefits by even a small improvement in safety levels would be noteworthy for users, city and government authorities, insurance companies as well as healthcare and policing services. In addition, AVs can allow drivers not used to local driving customs to drive anywhere globally e.g., a British driver to drive in Germany (driving left/right side of the road); someone used to driving with automatic gears to drive a rented AV when on holidays i.e., no exclusion due to the use of manual gearbox in that country; adjustment to local customs and legislation e.g., driving in Mediterranean or Middle East countries where driving seems more aggressive compared with northern European countries.

Another common expectation driving research behind autonomous cars is the minimum—if any—requirement for human interaction during travel which minimises driving disutility, increasing comfort and offering the opportunity to engage with other work or leisure activities while on board. Better use of travel time in AVs can be useful both for urban and interurban trips, but naturally agglomeration effects would be more evident in urban areas. If these effects contribute to lowering transport costs per AV anywhere between US$2000 and US$4000 [20], then this can be useful for New Economic Geography [50, 51] analyses which have transport as an integral component and may be used as a relevant theoretical framework. Other benefits for users will be the opportunity to use an autonomous car virtually anywhere in the world with minimal need for local adjustments, along with the ability to use an autonomous car without any age restrictions and the observed link to road fatalities. The U shaped curve (Fig. 2) essentially demonstrates that there is a higher risk of young and elderly drivers—compared to middle aged drivers—to be involved in fatal accidents the more they drive. Fatality rates with AVs will not be dependent on age, hence the flat line in cases 1–4. Depending on the actual safety rate (red dotted line) of AVs (when operational and according to the technological case realised), this fatality risk could be slightly reduced (e.g., cases 3–4), significantly reduced (case 2) or even eliminated (case 1) for all users, including the young and elderly.

Fatality rates per distance driven using conventional vehicles and self-driving vehicles as a function of driver/user age – Source: [48]

Through the use of social media and smartphone applications, cities can capitalize on the reduced demand for parking converting parking spaces to other useful and perhaps profitable land uses. The underlying assumption here is that due to the wider use of AVs—and particularly shared AVs—the total car fleet within a city will decrease. Having a smaller car fleet decreases demand for parking. This could be due to more efficient use of a single vehicle by different household members which will reduce the need for parking of this single vehicle—increasing its total VKT (Vehicle Kilometers Travelled), but reducing the total kilometers travelled per user. In short, the ‘shared’ AV car is expected to be travelling most of the day, unlike the ‘owned’ car which is parked most of the day. Astonishingly, the average car in the US remains parked for 96 % of the time [52] and space used for car parking in CBDs (Central Business Districts) can take up to 80 % of CBD land area [53] highlighting the potential of this transformation. Additionally, it has been estimated that in Singapore for example, the total current mobility needs of the city can be accommodated by approximately 1/3 of the current passenger vehicle fleet if it was replaced with a fleet of shared autonomous vehicles [54]. Such a move would hugely impact congestion and may also introduce environmental benefits through eco-driving, reduced idling or platooning of AVs which improves fuel efficiency and reduces the average travel time [55]. Equally, accessibility will be improved and transport related social exclusion arising from lack of access to car driving (e.g., due to disability which prevents driving or lack of a valid driving license) may be eliminated.

Furthermore, city and regional authorities will benefit by the installation and use of city dashboards, namely intelligent operation centers,Footnote 9 which will enhance traffic management by converting data collected through V2x technology to useful information. Being aware of bottlenecks and upcoming traffic will allow authorities to direct traffic and emergency response vehicles accordingly minimising delays within the overall transport network. Databases will expand continuously due to daily travel, which will allow local authorities to use Big Data observing trends and patterns in near real-time. Sharing such data in innovative ways under predefined conditions through Open Data platforms [57] can create value and generate revenues for local and regional authorities.

Moreover, gamification is another channel which can meet wider policy targets such as fuel saving, whilst at the same time opening up new markets for software development and marketing through individual or collective incentives [58–60]. At the moment it is estimated that about 5 billion devices are connected and this volume is anticipated to increase to around 25 billion by 2020, with automotive related devices constituting a major component [61]. Despite earlier similar forecasts not having been realised [62], it is obvious that new business opportunities are arising concurrently for the transport and logistics sectors. European industry in particular is orientated to playing a leading role in this emerging landscape. The long anticipated Galileo launch and its in-car satellite navigation system [63], the EU Research and Innovation Framework Programme H2020 priorities about ‘smart’ and ‘green’ transport, along with relevant national policies e.g., in The Netherlands or the UK (see The wider context surrounding autonomous cars section), will be instrumental in supporting European business development.

Threats

Urbanization trends in the 21st century may leave certain European and global regions unable to adjust their transport systems due to shrinking population (e.g., Detroit, Riga, Vilnius) which can result in lack of essential—but sometimes costly—‘smart’ infrastructure to accommodate AVs. Similarly, there is a risk of autonomous cars or shared transport services to be offered at high cost. The latter can face consumer resistance to purchase and may lead to social exclusion of lower income groups relying on car travel, since it has been estimated that the annual individual savings would average US$500 which will not offset the predicted incremental annual cost of AV use [64–66]. “Motorists spend on average US$2000 for fuel and US$1000 for insurance per vehicle-year. If AVs reduce fuel consumption by 10 % and insurance cost by 30 %, the total annual savings will average US$500” [64]. Thus, cost is a key dimension to focus on when deploying AVs and it can mainly be reduced through widespread adoption or a policy package approach [67] to achieve economies of scale. On an aggregate urban level, the pursuit of increased comfort during journeys [68] can lead to the selection of routes with less intersections or other characteristics, ultimately resulting in increased congestion and energy use. If autonomous cars are not going to be 96 % of their time parked, there may be adverse effects on congestion or energy use as more kilometres may be driven per car [69]. What is crucial to point out here is that the criteria and authority deciding on the optimal route are vital, as it may eventually mean that users will not have complete autonomy to select their travel route which may reduce their comfort and incentive to use autonomous cars. However, as Kitchin et al. [70] have stressed, taking such decisions solely based on data acquired through city dashboards could be risky since such information may be valuable but often not comprehensive. Data acquired through city dashboards may not be fully accurate due to the fact that not all travellers are using ICT and due to problems potentially faced by the technology used resulting in missing or inaccurate data.

Arising complexities may be even higher at a national level since identifying and assigning responsibility for car accidents may become more fuzzy, increasing insurance premiums [71]. Given also that the average car age in the EU-15 area was 7.5 years in 2004—i.e., before the Eurozone crisis—with cars in Luxemburg being changed every 3 years on average, whereas in Greece they were changed every 13 years [72], the transition period when both conventional and autonomous cars will be used may have to be over a decade. Therefore, the lack of coordination and common legislation could be a major threat regarding accident liability [73] or fuelling the digital divide and deriving social and spatial exclusion. Governments will also have to consider seriously unintended consequences such as privacy, surveillance and data management issues linked with ICT for transport [74, 75]. A contemporary case in the USFootnote 10 identified the threat of wireless hacking to gain unauthorised control of AVs (or even existing NHTSA Level 1–2 vehicles), which triggered approval of the Security and Privacy in Your (SPY) Car Act of 2015 at a national level [78]. The storage, management and use of mobility data either generated by autonomous cars, by V2I sensors or by smartphone apps are still at an embryonic stage and initiatives such as the Privacy Impact Assessment [79] should be used more widely at European or international levels to identify and address such concerns.

From a business perspective, it is imperative to have in place reliable ICT infrastructure since autonomous cars require high quality communication networks with high transmission capacity equipment aside from a high market penetration rate to achieve optimal performance. Although mapping issues [80] may be overcome while technology matures, a key barrier in developing such networks may be the parallel development of competing technologies which would mean inefficient use of resources due to a lack of common international standards. Additionally, businesses should ensure that evolving services address the needs of the so called ‘invisible groups’ [81], those social groups which are not the majority or the average, since those needs are rarely taken into account at the design phase [82] despite them constituting more than 15 % of the global population [83].

A threat which is often neglected and is at the core of this paper is the risk of autonomous cars leading to the renaissance of the private car against the ‘peak car’ theory and at the expense of public and NMT (non-motorized transport). The latter risk is particularly relevant for small and medium sized cities of less than 500,000 inhabitants which form more than 90 % of the cities in Europe [84]. If these vehicles are offered dedicated lanes to travel at the early deployment stages and in combination with ICT advancements, such evolution could lead to the resurgence of sprawled development and its interconnected impacts [47, 85]. Such impacts include higher obesity levels or other negative health impacts intertwined with lower levels of walking and cycling [86] which may exacerbate social segregation between those able to afford AVs and those who will not.

On the whole, it is yet unclear whether AVs will deepen or revert the ‘peak car’ phenomenon based on the aforementioned evidence. If aggregate vehicle kilometres travelled within a city are reduced due to technological improvements (e.g., advanced V2x navigation) or car sharingFootnote 11 and early findings of simulations such as in Singapore can be confirmed, then ‘peak car’ may become widespread with a lasting impact. On the contrary, if AVs introduce higher demand for longer commuting trips (better use of travel time increasing well being) [88] and if the car sharing element results in more aggregate vehicle kilometres travelled, then ‘peak car’ may be reverted even in developed countries where it has been detected. There are benefits in either case though, since on one hand commuting time can be reduced increasing working or leisure time. On the other hand employers may benefit by increased productive time of their employees while on transit or employees may benefit by more leisure options while commuting (Fig. 3).

AVs may be even used to sleep while on transit. The Stained Glass Driverless Sleeper Car (or mini Cathedral) by Dominic Wilcox, commissioned by MINI and Dezeen.com. Images by Sylvain Deleu

Choosing between the blessing and the curse

According to Stokes [4] who broadly abides to the ‘peak car’ theory for the UK, various scenarios are possible for the future. His analysis predicts a minor increase of the overall car use per person of less than 1 % by 2019 and then a 3 % decline compared to 2013 levels by 2036. Additionally, he suggests that a larger proportion of older (+65) women (>60 %) will have access to a car as a driver in 2036 compared to less than 40 % in 2012. This increase from <40 % to >60 % is important as it will increase accessibility for elderly women who may feel excluded nowadays as they cannot drive. This can increase inclusion and gender equity as driving licenses have to be renewed periodically after the age of 65 in several countries. Going back to the ‘peak car’ phenomenon we reiterate Stokes’ (2013) main conclusion that given what is known about ‘peak car’ we cannot forecast future levels of car use at sufficient confidence levels. An important point to take into account from this phenomenon in some developed countries is that car travel does not have to rise perpetually, even at times when there is no evidence to suggest we travel less. Even more important, the ‘peak car’ phenomenon presents a unique opportunity to shape and influence not only future mobility levels (how much we travel) but also how we travel. Hence it can be said with high certainty that AVs will have a decisive effect on future mobility.

Burns [89] ends his praise for the driverless cars by saying: “We must bring together technology, systems design methods and business models to supply better mobility at low cost to consumers and to societies” (p: 182). This is an attractive proposition with which it is almost impossible to disagree. But it is the exact same thinking that brought the mobility benefits of the ‘with-driver’ private car and the high-carbon mobility with it, the one we now try so hard to move away from. If it is hard to get people out of their cars it can be expected to be harder to get people out of their autonomous cars given the higher number of available options to use travel time for work or leisure. Travel time will then be seen as useful time, namely not wasted time decreasing travel utility. If we will choose to go down the road we now try so hard to escape, the AVs will with high certainty be a curse.

At the same time and as noted previously, AVs offer a unique opportunity to de-privatise car use through sharing [90]. This could have a transformative impact on our mobility. Even more so if sharing will be in the form of more than one individual or groups using the car interchangeably (sharing can take place temporally and spatially). Using AVs to boost car sharing has the potential to reduce environmental impacts [2, 55, 64]. Yet, this is often taken as given not considering at all any unintended consequences, especially overlooking the potentially large rebound effect stemming from overcoming the reality of wasting time while in the car (or, put in other words, the potential to use time more productively while in the car) especially when trying to find a parking space. Given that transport is the sector with the highest growth in terms of energy use and that 96 % of all transport uses fossil fuel [91, 92], fuel resources and green transport are intertwined. Akyelken et al. [93] describe a continuum that runs from car owning on one hand, through car and bike sharing, to public transport on the other—the ultimate and full sharing mobility service. The AV opens up the opportunity for new ‘green’ autonomous public transport. Building up on the use of driverless trains (e.g., Docklands Light Railway in London), this may take many different forms (see The wider context surrounding autonomous cars section) transforming public transport to a stronghold of our transport and mobility system. Hence the AV can certainly be a blessing.

Whether the AV locks us further in or out of the ‘car based society’ depends on the choices we make as a society, not solely on a specific technological development. For the AV to be a blessing and not a curse, technological development has to be intertwined with societal change in the way we view cars and our mobility. If societal change would make it possible to perceive public and sharing as superior to private and individual transport, then autonomous vehicles could definitely be seen as a blessing for future mobility.

Likewise, AVs can have an important role in either sprawled or compact development, but building up on current use and experience with the private car, they will more likely contribute to sprawl and its effect on, for example, increasing per capita energy consumption by private passenger transport [94, 95].Footnote 12 Recent evidence for the USA has shown that sprawled development imposes external costs of around US$400bn annually on residents of sprawled areas and residents of other areas [85]. Comparing Atlanta and Los Angeles, which experience almost 90 % private motorised transport within their territory, with Berlin, London, Mumbai or Hong Kong, where the respective share is less than 1/3, showcases the different role of the private car in cities worldwide [2]. Consequently, we must seriously weigh the benefits alongside the threats of AVs and this is achieved here by evaluating a survey about sharing transport modes in London.

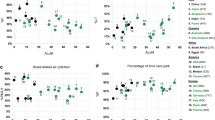

Corresponding to a previous survey (n > 2000) in the US and the UK about the intention to use AVs where 49 % were positive [98], a recent survey (n = 1023) concluded that Londoners are currently concerned about low carbon mobility and are willing to use shared transport modes including bicycles and electric cars. Nevertheless, the high sample proportion (58 %) willing to use a shared EV scheme may be translated as a willingness to stop using the bicycle sharing scheme. Therefore, there might be a risk of a reversal to higher car use in the future [99].

Evidence suggests that ‘smart growth’ community residents typically own 10–30 % fewer vehicles, drive 20–40 % less, and use alternative transport modes 2–10 times more than in car-dependent locations [85]. Are AVs ‘smart’ just because they are based on advanced technology? Will they still be ‘smart’ in the context of moving towards low carbon mobility if used privately and not publicly? What the discussion above mainly aims to demonstrate and highlight is that AVs, and technological development in general, are not a policy and cannot be a policy. The widespread use of AVs, like any technological development, is one important policy measure (or tool) in whatever transport and mobility policy we choose to promote as part of a wider strategy, and this is how they should be seen. Even with the promising advances in the development of the AV, there are still very hard and challenging policy decisions to make and options to choose from.

How to proceed from here

In the high-carbon mobility business-as-usual scenario and with the AV fully developed and becoming the central element in the mobility and transport system, it is likely that for the first time in history we will break from the one-hour per day (on average) travel time budget [15, 100]. If we could sleep, meet, work and eat in the AV while travelling, then travel time will become a utility, not a disutility. The implications are immense, not only for value of travel time estimation, and encompass probably every aspect of life, physical and social.

While there are undoubtedly good reasons for the excitement associated with the development of the AV, policy and research alike must take a cautious approach towards its development. Governments—national and regional—will have to take steps to critically examine transport policy strategy in light of the AV evolution. More importantly, research that goes well beyond the technical, safety, regulatory and commercial aspects of AV development and deployment must be carried out. The social aspects of adopting the AV and especially who will be able to access it and who will not; the travel behaviour implication of eliminating the need to drive; the infrastructure investment and the land use alterations required; all need to be carefully assessed within a research framework which is free from any commercially vested interests.

In fact, the contemporary goal of most transport policy plans to shift people out of their cars into walking, cycling and public transport still applies. But the potential for this shift is much larger with the AV. Even if the focus is currently on the autonomous car, the autonomous public transport [101] offers much more potential and AVs could prove to be the key success factor for a transport system that relies on public transport. Gains can even be extended if such autonomous public transport is integrated with higher levels of walking and cycling especially for the last mile travel [86]. The AV technology in a way does not make a big difference for transport policy, but at the same time it can make it much easier or harder to achieve the transport policy goals we set. Since the AV is imminent, the choice will have to be made and the sooner we make an informed and realistic decision on the role of the AV in the future mobility and transport system, the better. Otherwise we will find ourselves on the road we so hard try to get off from today.

As alluded to above, in many respects and despite its revolutionary flavour, the AV does not change much when it comes to deciding on the main principles for transport policy. Revising Table 1, the choice between pathways A, B or C remains the same and is still challenging both options, namely with and without the introduction of AVs. These choices must be made now, otherwise we are sure to continue on the business-as-usual pathway of high-carbon mobility. Surely it will be inevitable to have a transition period of AVs, semi-autonomous and manual cars coexisting on roads as with the uptake of any other new technology. Thus planning should be cautious taking into account the benefits and threats (see Benefits and threats of future mobility patterns section) until the use of AVs gains broader momentum and we make up our minds about their public or private element [44] and until effective legal frameworks evolve.

In a post-economic-crisis Europe, it is important to prioritise environmental targets whilst minimising costs and the need for new infrastructure. Also with the AV we will have to decide if we fight climate change and reduce air pollution; if we support European business to become a global leader in this field or if we allocate funds to other sectors; if we preserve, increase or reduce travel speed (overall within the transport system) and if we plan our cities for people or for (autonomous) cars. Applying a package approach [67] could allow several targets to be met, ensuring that we meet not only the likely but also the desirable outcomes. Those desirable outcomes should allow benefits to be dispersed across different impact groups and geographical locations across Europe and elsewhere.

For that reason, research on AVs should be multidisciplinary and inclusive, addressing dissimilar issues ranging from vehicle navigation and the effects of V2V on fuel efficiency to public acceptability and legal barriers while testing autonomous public transport in practice. Designing and assessing all aspects of AV trials such as those taking place in Michigan or Trikala is an indispensable step in testing innovative technologies, whereas promoting future collaborations between research, industry and government will only be beneficial, allowing a synergetic development model to emerge which can be replicated in more sectors. In essence, these efforts will inform decisions about the long-term impacts of new technologies on transport and urban form, the evaluation of these impacts and the kinds of governance which work successfully for the transport system [19, 40, 55, 68, 102–104].

The role of government in a pre-AVs era is critical and should focus, as it should always do, on policy, particularly transport policy and land use policy in this case. Governments should also observe the market, providing useful frameworks or regulations where needed, allowing however core profit driven actors to enter and reap any investment risks or rewards. Nevertheless, governments should find ways to incentivize AV development in alignment with its broader policy, which should remain achieving low carbon mobility.

Notes

A substantial change in the way we travel and move freight that takes place over a relatively short period of time, about 25 years [5].

“V2I is the wireless exchange of critical safety and operational data between vehicles and highway infrastructure, intended primarily to avoid or mitigate motor vehicle crashes but also to enable a wide range of other safety, mobility, and environmental benefits”[7].

V2V is a technology installed in selected cars allowing them to communicate with each other, i.e., vehicle-to-vehicle, using a system similar to wi-fi. It operates complementary to V2I.

And as likely between our cities. However for brevity we focus our discussion mainly on cities.

This is the base scenario and this figure can range between US$0.7 trillion and US$2.2 trillion per year. Additionally, this figure presents a one sided estimate as it focuses solely on the benefits, not including the costs and benefits of OEMs and the initial cost of purchasing an AV.

2getthere had served more than a million passengers in 2014. More information about PRT in Masdar available here: http://www.2getthere.eu/projects/masdar-prt

PRT is one of the first AV forms operationalized and it is a good choice to test it in the Middle East, since religious and/or cultural reasons justify currently the need to travel in small groups. According to ATRA [26], Personal rapid transit systems attempt to eliminate negative impacts of time delay and emissions due to regular public transport stops and acceleration/deceleration by moving non-stop small groups of travellers in automated vehicles on fixed tracks. When NHTSA Level 4 automation of AVs will be available (which is a key assumption of this paper), PRTs will be ahead of the SuperLev suggestion i.e., travelling solely on fixed tracks and will be able to move anywhere within the transport network.

Battery autonomy refers to the capability of an electric car’s battery to power the vehicle without charging.

City dashboards have existed for a number of years already (e.g., Amsterdam, Dublin, Leeds, London). However, the emergence of the ‘smart cities’ notion along with ringfenced funding from local, national or international authorities have allowed organizations to seize the opportunity and develop city and regional corporate solutions. IBM defines such services as “helping government leaders to manage complex city environments, incidents and emergencies with a city solution that delivers operational insights” [56]. The Rio Intelligent Operations Center for Smarter Cities cost US$14 million, which demonstrates that a significant amount of commitment and investment is required for their implementation and success.

Car sharing reduced car ownership levels in a US sample by half [87].

References

Newman P, Kenworthy JR (2011) Peak car use: understanding the demise of automobile dependence. World Transp Policy Pract 17(2):31–42

Rode P, Floater G, Thomopoulos N, Docherty J, Schwinger P, Mahendra A, et al (2014) Accessibility in cities: transport and urban form. Report No.: 03. LSE Cities: London

Goodwin P, van Dender K (2013) “Peak Car”—themes and issues. Transp Rev 33(3):243–254

Stokes G (2013) The prospects for future levels of car access and use. Transp Rev 33(3):360–375

Gilbert R, Perl A (2010) Transport revolutions: moving people and freight without oil, 2nd edn. New Society Publishers, Gabriola Island

NHTSA (2013) U.S. Department of Transportation Releases Policy on Automated Vehicle Development. National Highway Traffic Safety Administration. http://www.nhtsa.gov/About+NHTSA/Press+Releases/U.S.+Department+of+Transportation+Releases+Policy+on+Automated+Vehicle+Development. Accessed 1 May 2015

US DoT (2014) Vehicle-to-Infrastructure (V2I) Communications for safety. Research and Innovative Technology Administration (RITA)—United States Department of Transportation. http://www.its.dot.gov/research/v2i.htm. Accessed 29 April 2015

United Nations (2014) World urbanization prospects—highlights. UN Department of Economic and Social Affairs. Report No. ST/ESA/SER.A/352. http://esa.un.org/unpd/wup/Highlights/WUP2014-Highlights.pdf. Accessed 1 May 2015

TfL (2015) Travel in London Report 7. Transport for London, London. https://tfl.gov.uk/cdn/static/cms/documents/travel-in-london-report-7.pdf. Accessed 1 August 2015

Givoni M, Banister D (2013) Moving towards low carbon mobility. Edward-Elgar, Cheltenham

Givoni M (2013) 13. Alternative pathways to low carbon mobility. In: Givoni M, Banister D (eds) Moving towards low carbon mobility. Edward Elgar Publishing, Cheltenham, p 209

TRB (2009) Driving and the built environment: the effects of compact development on motorized travel, energy use and CO2 emissions. Washington, D.C: Transportation Research Board. Report No.: 298. http://onlinepubs.trb.org/Onlinepubs/sr/sr298.pdf. Accessed 1 July 2015

Newman P, Kenworthy JR (1999) Sustainability and cities: overcoming automobile dependence. Island Press, Washington, D.C

Goodwin P (2012) Three views on Peak Car. Wolrd Transp Policy Pract 17:8–17

Metz D (2013) Peak car and beyond: the fourth era of travel. Transp Rev 33(3):255–270

Delbosc A, Currie G (2013) Causes of youth licensing decline: a synthesis of evidence. Transp Rev 33(3):271–290

Anderson JM, Kalra N, Stanley KD, Sorensen P, Samaras C, Oluwatola OA, et al. (2014) Autonomous vehicle technology: a guide for policymakers. http://public.eblib.com/choice/publicfullrecord.aspx?p=1603024. Accessed 19 July 2015

Fagnant DJ, Kockelman K (2013) Preparing a nation for autonomous vehicles: Opportunities, barriers and policy recommendations for capitalizing on self-driven vehicles. In: Proceedings of the Transportation Research Board. Washington, D.C. pp 1–20. http://www.caee.utexas.edu/prof/kockelman/public_html/TRB14EnoAVs.pdf. Accessed 1 July 2015

Hoppe M, Christ A, Castro A, Winter M, Seppänen T-M (2014) Transformation in transportation? Eur J Futur Res 2(1):1–14

Fagnant DJ, Kockelman K (2015) Preparing a nation for autonomous vehicles: Opportunities, barriers and policy recommendations. Transp Res Part Policy Pract 77:167–181

Morgan Stanley (2013) Autonomous cars: self-driving the new auto industry paradigm. Morgan Stanley Research Global, United States. http://www.wisburg.com/wp-content/uploads/2014/09/%EF%BC%88109-pages-2014%EF%BC%89MORGAN-STANLEY-BLUE-PAPER-AUTONOMOUS-CARS%EF%BC%9A-SELF-DRIVING-THE-NEW-AUTO-INDUSTRY-PARADIGM.pdf. Accessed 1 July 2015

Glaeser EL, Kohlhase JE (2013) Cities, regions and the decline of transport costs. Pap Reg Sci 83(1):197–228

Blumenfeld M. SuperLev (2012) Reducing the impact of transport on the environment. TEDx event: 5 November 2012. University of Leeds, UK. http://tsh.leeds.ac.uk/2012/11/05/tedx-reducing-the-impact-of-transport-on-the-environment/. Accessed 17 March 2015

Diez-Jimenez E, Valiente-Blanco I, Castro-Fernandez V, Perez-Diaz JL (2014) Design and analysis of a non-hysteretic passive magnetic linear bearing for cryogenic environments. Proc Inst Mech Eng Part J J Eng Tribol 228(10):1071–1079

Perez-Diaz J-L, Diez-Jimenez E, Valiente-Blanco I, Cristache C, Alvarez-Valenzuela M-A, Sanchez-Garcia-Casarrubios J (2014) Contactless mechanical components: gears, torque limiters and bearings. Machines 2:312–324

ATRA IG (2013) Advanced transit 2013. http://www.advancedtransit.org/newsroom/viewpoint/. Accessed 1 July 2015

Gilbert R, Perl A (2007) Grid-connected vehicles as the core of future land-based transport systems. Energy Policy 35(5):3053–3060

Masdar (2015) Masdar city at a glance. Masdar Corporate, Abu Dhabi. http://www.masdar.ae/en/masdar-city/detail/masdar-city-at-a-glance. Accessed 2 April 2015

Walsh B (2011) Going green - Masdar City: the world’s greenest city? TIME: 25 January 2011. http://content.time.com/time/health/article/0,8599,2043934,00.html. Accessed 17 March 2015

Tebay A (2013) PRT system to open for Suncheon Bay garden expo. Kojects. http://kojects.com/2013/02/13/prt-system-to-open-in-april-for-suncheon-bay-garden-expo/#more-1411. Accessed 17 March 2015

Ultra Global (2011) Heathrow T5 | Ultra Global PRT. Ulhttp://www.ultraglobalprt.com/wheres-it-used/heathrow-t5/. Accessed 17 March 2015

Kleis R (2015) From station to campus without a driver. RESOURCE: Wageningen. http://resource.wageningenur.nl/en/show/From-station-to-campus-without-a-driver.htm. Accessed 17 March 2015

Transport Systems Catapult (2015) Self-driving vehicles in Milton Keynes. https://ts.catapult.org.uk/blog/-/blogs/self-driving-vehicles-in-milton-keyn-1. Accessed 17 Aug 2015

Crompton H (2015) GATEway. Digital Greenwich: London. http://www.digitalgreenwich.com/driverless-cars/. Accessed 1 May 2015

Thomopoulos N, Givoni M, Rietveld P (2015) Introduction: transport and ICT—chapter 1. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham, pp 1–22

Google (2015) Google self-driving car project. https://plus.google.com/+GoogleSelfDrivingCars/. Accessed 23 April 2015

Renault (2015) Renault’s autonomous and connected car http://group.renault.com/en/passion-2/innovation/renault-a-born-innovator/autonomous-and-connected-car/. Accessed 28 April 2015

Reuters (2015) Apple studies self-driving car, auto industry source says. http://www.reuters.com/article/2015/02/14/us-apple-autos-idUSKBN0LI0IJ20150214. Accessed 17 March 2015

Tesla Motors (2014) Tesla’s musk sees fully autonomous car ready in 5 years | Forums http://my.teslamotors.com/fr_CH/forum/forums/tesla%E2%80%99s-musk-sees-fully-autonomous-car-ready-5-years. Accessed 2 April 2015

Thomopoulos N, Givoni M, Rietveld P (2015) Amalgamating ICT with sustainable transport—building on synergies and avoiding contradictions—chapter 12. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham, pp 297–304

Foresight (2013) The future of manufacturing: a new era of opportunity and challenge for the UK. The Government Office for Science, London. https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/255922/13-809-future-manufacturing-project-report.pdf. Accessed 1 May 2015

van den Berg V, Verhoef E (2015) Robot cars and dynamic bottleneck congestion: the effects on capacity, value of time and preference heterogeneity. Tinbergen Institute, Amsterdam. 2http://papers.tinbergen.nl/15062.pdf. Accessed 1 July 2015

TRL (2015) MPs propose a minister for driverless cars. TRL News Hub, Berkshire. http://trl.co.uk/news-hub/transport-news/latest-transport-news/?id=801778692. Accessed 17 March 2015

House of Commons Transport Committee (2015) Motoring of the future: strategy to maximise benefits of new motoring technology needed. House of Commons Transport Committee, London. http://www.parliament.uk/business/committees/committees-a-z/commons-select/transport-committee/news/motoring-future-report/. Accessed 1 July 2015

Waldrop MM (2015) Autonomous vehicles: no drivers required. Nature 518(7537):20–23

Cummings ML, Ryan J (2014) Who is in charge? Promises and pitfalls of driverless cars. Duke University, Durham. http://hal.pratt.duke.edu/sites/hal.pratt.duke.edu/files/u7/TR%20news%20Cummings%20MAR14.pdf. Accessed 1 July 2015

Steven E. P (2013) Implications to public transportation of automated or connected vehicles. Florida Automated Vehicles Summit 13 November 2013, Florida. http://www.tampa-xway.com/Portals/0/Media/AV%20Presentations/11%20-%20Implications%20to%20Public%20Transportation%20of%20Automated%20or%20Connected%20Vehicles.pdf. Accessed 1 July 2015

Sivak M, Schoettle B (2015) Road safety with self-driving vehicles: General limitations and road sharing with conventional vehicles. University of Michigan Report No.: 2015–2. http://www.driverlesstransportation.com/wp-content/uploads/2015/01/UMTRI-2015-2.pdf. Accessed 1 May 2015

Zegras C, Butts K, Cadena A, Palencia D (2015) Spatiotemporal dynamics in public transport personal security perceptions: digital evidence from Mexico City’s periphery. In: Thomopoulos N, Givoni M, Rietveld (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham

Krugman P, Fujita M, Venables A (1999) The spatial economy. MIT Press, Cambridge MA

Krugman P (2010) The new economic geography, now middle-aged. AAG Annual Meeting presentation 16 April 2010, Washington, DC. http://www.princeton.edu/~pkrugman/aag.pdf. Accessed 1 May 2015

Heck S, Rogers M, Cummings J (2014) Resource revolution: how to capture the biggest business opportunity in a century. Melcher Media, New York

Manville M, Shoup D (2004) People, parking and cities. ACCESS Magazine 1(25). https://escholarship.org/uc/item/6nf254fd. Accessed 1 May 2015

Spieser K, Treleaven K (2014) Toward a systematic approach to the design and evaluation of automated mobility-on-demand systems: a case study in Singapore. In: Meyer G, Beiker S (eds) Road vehicle automation. Springer, Heidelberg, pp 229–245

Lu W, Han LD (2015) Impacts of vehicular communication network on traffic dynamics and fuel efficiency - Chapter 7. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham, pp 161–178

Dignan J, Shah N, Tunvall F (2013) Deriving insight from data for smarter urban operations. Ovum. http://www-01.ibm.com/software/city-operations/offers/Intelligent%20Urban%20Operations%20Whitepaper%20-%20IBM_Ovum%20branded%20FINAL.PDF. Accessed 1 July 2015

TfL (2015) Open data users. Transport for London. http://www.tfl.gov.uk/info-for/open-data-users/. Accessed 20 April 2015

Magana VC, Munoz-Organero M (2015) GAFU: using a gamification tool to save fuel. IEEE Intell Transp Syst Mag 7(2):58–70

McCall R, Koenig V, Kracheel M (2013) Using gamification and metaphor to design a mobility platform for commuters. Int J Mob Hum Comput Interact 5(1):1–15

Vardaxoglou G, Baralou E (2014) Studying gamification as a series of dynamic activity systems: a conceptual and empirical study. Proceedings of EGOS Conference, Rotterdam

Gartner (2014) Gartner says 4.9 billion connected “things” will be in use in 2015. http://www.gartner.com/newsroom/id/2905717. Accessed 2 April 2015

Cisco (2015) Internet of things. Cisco; 2011. http://www.cisco.com/web/solutions/trends/iot/overview.html. Accessed 17 March 2015

European Commission (2015) EU successfully launches two Gallileo satellites. EC Internal market, Industry, Entrepreneurship and SMEs. http://ec.europa.eu/growth/tools-databases/newsroom/cf/itemdetail.cfm?item_id=8194&lang=en. Accessed 4 Feb 2015

Litman T (2015) Autonomous Vehicle implementation predictions: implications for transport planning. Proceedings of the 94th Transportation Research Board Annual Meeting, Washington, D.C. pp 1–15. http://trid.trb.org/view.aspx?id=1338043. Accessed on 1 July 2015

Howard D, Dai D (2014) Public perceptions of self driving cars: the case of Berkeley, California. Proceedings of the 93rd Transportation Research Board Annual Meeting, Washington, D.C. pp 1–21. https://www.ocf.berkeley.edu/~djhoward/reports/Report%20-%20Public%20Perceptions%20of%20Self%20Driving%20Cars.pdf. Accessed 1 July 2014

Schoettle B, Sivak M. A (2014) A survey of public opinion about autonomous and self-driving vehicles in the U.S., the U.K., and Australia. http://deepblue.lib.umich.edu/handle/2027.42/108384. Accessed on 30 July 2015

Givoni M (2014) Addressing transport policy challenges through policy-packaging. Transp Res Part Policy Pract 60:1–8

Le Vine S, Zolfaghari A, Polak J (2015) Autonomous cars: the tension between occupant experience and intersection capacity. Transportation Research Part C: Emerging Technologies 52:1–14

UMTRI (2015) Driverless vehicles: fewer cars, more miles. University of Michigan Transportation Research Institute. http://www.umtri.umich.edu/what-were-doing/news/driverless-vehicles-fewer-cars-more-miles. Accessed 1 May 2015

Kitchin R, Lauriault T, McArdle G (2015) Knowing and governing cities through urban indicators, city benchmarking and real-time dashboards. Reg Stud Reg Sci 2(1):6–28

Hevelke A, Nida-Ruemelin J (2015) Responsibility for crashes of autonomous vehicles: an ethical analysis. Sci Eng Ethics 21(3):619–630

EEA (2005) Average age of the vehicle fleet. European Environment Agency, Copenhagen. http://www.eea.europa.eu/data-and-maps/indicators/average-age-of-the-vehicle-fleet-4. Accessed 1 May 2015

Schellekens M (2015) Self-driving cars and the chilling effect of liability law. Comput Law Secur Rev 31(4):506–517

Herzogenrath-Amelung H, Troullinou P, Thomopoulos N (2015) Reversing the order: towards a philosophically informed debate on ICT for transport - chapter 9. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham

Glancy D (2012) Privacy in autonomous vehicles. St Clara Law Rev 52(4):1171–1239

Markey E (2015) Sens. Markey, Blumenthal introduce legislation to protect drivers from auto security, privacy risks with standards & “cyber dashboard” rating system. Senator Ed Markey. http://www.markey.senate.gov/news/press-releases/sens-markey-blumenthal-introduce-legislation-to-protect-drivers-from-auto-security-privacy-risks-with-standards-and-cyber-dashboard-rating-system. Accessed 28 July 2015

Goldman J (2015) Car hacking arms race starts: Chrysler recalls 1.4 million vehicles—eSecurity Planet. eSecurity Planet. http://www.esecurityplanet.com/network-security/the-car-hacking-arms-race-begins-chrysler-recalls-1.4-million-vehicles.html. Accessed 28 July 2015

US Senate (2015) Security and privacy in your car (SPY Car) Act of 2015. http://www.markey.senate.gov/imo/media/doc/SPY%20Car%20legislation.pdf. Accessed 28 July 2015

Information Commissioner’s Office (2014) Conducting privacy impact assessments code of practice [Internet]. Information Commissioner’s Office, London. https://ico.org.uk/media/for-organisations/documents/1595/pia-code-of-practice.pdf. Accessed 1 May 2015

Qiyang X, Dodds E (2015) Enhancing transport through open geospatial data and crowdsourcing. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham, pp 140–160

Gaisbauer H, Sedmak C (2014) Neglected futures. Considering overlooked poverty in Europe. Eur J Futur Res 2(1):1–8

Pronello C, Camusso C (2015) User requirements for the design of efficient mobile devices to navigate through the public transport network - chapter 3. In: Thomopoulos N, Givoni M, Rietveld P (eds) ICT for transport: Opportunities and threats. Edward Elgar Publishing, Cheltenham, pp 55–93

Matthews B (2013) Accessibility apps for disabled people. COMPASS Final Conference; 13 November 2013, Rome. http://www.fp7-compass.eu/images/CO_Final_Conference/compass%20final%20conference%20matthews%20accessibility%20apps.pdf. Accessed on 1 May 2015

European Commission (2011) Cities of tomorrow: challenges, visions, ways forward. DG Regio, Brussels . http://ec.europa.eu/regional_policy/sources/docgener/studies/pdf/citiesoftomorrow/citiesoftomorrow_final.pdf. Accessed on 1 May 2015

Litman T (2015) Analysis of public policies that unintentionally encourage and subsidize urban sprawl. Victoria Transport Policy Institute - LSE Cities, Victoria. http://files.lsecities.net/files/2015/03/NCE-Cities-Sprawl-Subsidy-Report.pdf. Accessed on 24 March 2015

Woodcock J, Givoni M, Morgan AS (2013) Health impact modelling of active travel visions for England and wales using an integrated transport and health impact modelling tool (ITHIM). PLoS One 8(1), e51462

Martin E, Shaheen S (2011) The impact of carsharing on household vehicle ownership. ACCESS Magazine 38(1). http://www.accessmagazine.org/articles/spring-2011/impact-carsharing-household-vehicle-ownership/. Accessed 1 July 2015

Berliner RM, Malokin A, Circella G, Mokhtarian PL (2015) Travel-based multitasking: modeling the propensity to conduct activities while commuting. Proceedings of the 94th Transportation Research Board Annual Meeting, Washington, D.C. http://trid.trb.org/view.aspx?id=1338990. Accessed on 30 July 2015

Burns L (2013) Sustainable mobility: a vision of our transport future. Nature 497(7448):181–182

Kopp J, Gerike R, Axhausen KW (2015) Do sharing people behave differently? An empirical evaluation of the distinctive mobility patterns of free-floating car-sharing members. Transportation 42(3):449–469

COMPASS (2015) Scarce resources of fossil fuels. Optimised co-modal passenger transport for reducing carbon emissions. http://www.fp7-compass-keytrends.eu/index.php/environment-domain/2-non-categorizzato/45-scarce-resources-of-fossil-fuels#Impacts_on_Mobility_and_Transport. Accessed on 27 April 2015

European Commission (2012) Innovating for a competitive and resource efficient transport system. DG MOVE - European Commission. http://www.transport-research.info

Akyelken N, Anderton K, Mont O, Plepys A, Kaufman D (2013) Mobility report—deliverable 5.1 servicizing policy for resource efficient economy (SPREE) research project. Oxford, UK

Kenworthy JR (2005) Millennium cities database. Union Internationale Transport Publics, Brussels

Newman P, Kenworthy J (2015) The End of automobile dependence: how cities are moving beyond car-based planning. Island Press, Washington D.C

Cox W (2006) War on the dream: how anti-sprawl policy threatens the quality of life. iUniverse, Bloomington

Cox W (2014) New climate report misses point on US cities. New geography. http://www.newgeography.com/content/004534-new-climate-report-misses-point-us-cities. Accessed on 1 May 2015

Accenture (2011) Consumers in US and UK frustrated with intelligent devices that frequently crash or freeze, new Accenture survey finds | Accenture Newsroom. https://newsroom.accenture.com/article_display.cfm?article_id=5146. Accessed on 1 July 2015

WSP - ComRes (2014) Powering ahead—fast track to an all-electric city. WSP, London http://www.wspgroup.com/Globaln/UK/Whitepapers/Cities/WSP_Electric_Cities_Whitepaper.pdf. Accessed on 1 May 2015

Zehavi Y (1982) The travel money budget. Mobility Systems

Ferreras LE (2013) Autonomous vehicles: a critical tool to solve the XXI century urban transportation grand challenge. In: Jones SL (ed) Urban Public Transportation Systems, pp 405–412

Karaseitanidis G, Lytrivis P, Ballis A (2013) Local transport plans reviewed and automated road transport system assessment, CityMobil2 D9.1: cities demonstrating automated road passenger transport, Trikala. http://www.citymobil2.eu/en/upload/Deliverables/PU/D9.1_Trikala.pdf. Accessed on 1 May 2015

UMTRI (2015) U-M’s cityscape will test driverless vehicles. University of Michigan Transportation Research Institute. http://www.umtri.umich.edu/what-were-doing/news/u-ms-cityscape-will-test-driverless-vehicles. Accessed 29 April 2015

Bruun E, Givoni M (2015) Sustainable mobility: six research routes to steer transport policy. Nature 523(7558):29–31

Acknowledgments

The authors are grateful to WSP and ComRes for providing survey data about London. They are also thankful to Dominic Wilcox for providing images of his Stained Glass Driverless Sleeper Car prototype.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Thomopoulos, N., Givoni, M. The autonomous car—a blessing or a curse for the future of low carbon mobility? An exploration of likely vs. desirable outcomes. Eur J Futures Res 3, 14 (2015). https://doi.org/10.1007/s40309-015-0071-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s40309-015-0071-z