Abstract

A main focus in economics research is understanding the time series of prices of goods and assets. While statistical models using only the properties of the time series itself have been successful in many aspects, we expect to gain a better understanding of the phenomena involved if we can model the underlying system of interacting agents. In this article, we consider the history of Bitcoin, a novel digital currency system, for which the complete list of transactions is available for analysis. Using this dataset, we reconstruct the transaction network between users and analyze changes in the structure of the subgraph induced by the most active users. Our approach is based on the unsupervised identification of important features of the time variation of the network. Applying the widely used method of Principal Component Analysis to the matrix constructed from snapshots of the network at different times, we are able to show how structural changes in the network accompany significant changes in the exchange price of bitcoins.

Export citation and abstract BibTeX RIS

Content from this work may be used under the terms of the Creative Commons Attribution 3.0 licence. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. Introduction

The growing availability of digital traces of human activity provide unprecedented opportunity for researchers to study complex phenomena in society [1–6]. Data mining methods that preform unsupervised extraction of important features in large datasets are especially appealing because they enable researchers to identify patterns without making a priori assumptions [6, 7]. In this article, we use Principal Component Analysis (PCA) [8] to study the dynamics of a network of monetary transactions. We aim to identify relevant changes in network structure over time and to uncover the relation of network structure and macroeconomic indicators of the system [9–12].

In traditional financial systems, records of everyday monetary transactions are considered highly sensitive and are kept private. Here, we use data extracted from Bitcoin, a decentralized digital cash system, where the complete list of such transactions is publicly available [13–15]. Using this data, we construct daily snapshots of the transaction network [16], and we select the subgraph spanned by the most active users. We then represent the series of networks by a matrix, where each row corresponds to a daily snapshot. We carry out PCA on this dataset identifying key features of network evolution, and we link some of these variations to the exchange rate of bitcoins.

2. Methods

2.1. The Bitcoin dataset

Bitcoin is a novel digital currency system that functions without central governing authority, instead payments are processed by a peer-to-peer network of users connected through the internet. Bitcoin users announce new transactions on this network, and each node stores the list of all previous transactions.

Bitcoin accounts are referred to as addresses and consist of a pair of public and private keys. One can receive bitcoins by providing the public key to other users, and sending bitcoins requires signing the announced transaction with the private key. Using appropriate software1 , a user can generate unlimited number of such addresses; using multiple addresses is usually considered a good practice to increase a userʼs privacy. To support this, Bitcoin transactions can have multiple input and output addresses; bitcoins provided by the input addresses can be distributed among the outputs arbitrarily.

Due to the nature of the system, the record of all previous transactions since its beginning are publicly available to anyone participating in the Bitcoin network. We installed a slightly modified version of the open-source bitcoind client and downloaded the list of transactions from the peer-to-peer network on 3 March 2014. From these records, we recovered the sending and receiving addresses, the sum involved and the approximate time of each transaction. Throughout the paper, we only analyze transactions which happened in 2012 or 2013. We made the dataset and the source code of the modified client program available on the projectʼs website [17] and through our online database interface [18, 19].

2.2. Extracting the core network

To study structural changes in the network and their connection with outside events, we extract the subgraph of the most active Bitcoin users. As a first step, we apply a simple heuristic approach to identify addresses belonging to the same user [15]. We call this step the contraction of the graph. For this, we identify all transactions with multiple input addresses and consider addresses appearing in the same transaction to belong to the same user. Since initiating a transaction requires signing it with the private keys of all input addresses, we expect that these are controlled by the same entity. Note that this procedure will fail to contract addresses that belong to the same user, but are used completely independently. However, this is the most widely accepted method [14, 15, 20]. Therefore each node v in the transaction network represents a user, and each link  represents that there was at least one transaction between users u and v during the observed two-year period.

represents that there was at least one transaction between users u and v during the observed two-year period.

We identify the active core of the transaction graph using two different approaches: (i) we include users who appear in at least 100 individual transactions and were active for at least 600 days, i.e. at least 600 days passed between their first and last appearance in the dataset. We call these long-term users, and we refer to the extracted network as the LT core. (ii) We simply include the 2000 most active users. All users are considered, hence the resulting network is referred to as AU core. In both cases, we take the largest connected component of the graph induced by the selected nodes. Furthermore, we exclude nodes which are associated with the SatoshiDice gambling site2 . In 2012, this site and its users produced over half of all Bitcoin activity, which is not related to the normal functioning of the system.

In the case of long-term users, the LT core consists of  nodes and

nodes and  edges; these users control a total of 1 894 906 Bitcoin addresses which participated in 4 837 957 individual transactions during the examined two year period. In the case of most active users, the AU core has

edges; these users control a total of 1 894 906 Bitcoin addresses which participated in 4 837 957 individual transactions during the examined two year period. In the case of most active users, the AU core has  nodes and

nodes and  edges; the users in this subgraph have a total of 3 326 526 individual Bitcoin addresses and participated in a total of 12 900 964 transactions during the two years. The total number of Bitcoin transactions in this period is 27 930 580, meaning that the two subgraphs include

edges; the users in this subgraph have a total of 3 326 526 individual Bitcoin addresses and participated in a total of 12 900 964 transactions during the two years. The total number of Bitcoin transactions in this period is 27 930 580, meaning that the two subgraphs include  and

and  of all transactions respectively.

of all transactions respectively.

2.3. Detecting structural changes

To extract important changes in the graph structure, we compare successive snapshots of the active core of the transaction network using PCA. The goal is to obtain a set of base networks, and represent each dayʼs snapshot as a linear combination of these base networks.

We calculate the daily snapshots of the active core, each snapshot is a weighted network, and the weight of link  is equal to the number of transactions that occurred that day between u and v. A snapshot for day t can be represented by an n × n weighted adjacency matrix Wt, where

is equal to the number of transactions that occurred that day between u and v. A snapshot for day t can be represented by an n × n weighted adjacency matrix Wt, where  is the number of nodes in the aggregate network. Since there are

is the number of nodes in the aggregate network. Since there are  links overall, each Wt has at maximum l nonzero elements. We rearrange Wt into an l long vector wt. Note that we include all possible links, even if for that specific day, some are missing. For T snapshots, we now construct the

links overall, each Wt has at maximum l nonzero elements. We rearrange Wt into an l long vector wt. Note that we include all possible links, even if for that specific day, some are missing. For T snapshots, we now construct the  graph time series matrix X such that the tth row of X equals wt [10]. This way, we can consider X as a data matrix with T samples and l features, i.e. we consider each day as a sample, and the activities of possible edges as features.

graph time series matrix X such that the tth row of X equals wt [10]. This way, we can consider X as a data matrix with T samples and l features, i.e. we consider each day as a sample, and the activities of possible edges as features.

To account for the for the high variation of the daily number of transactions, we normalize X such that the sum of each row equals 1. After that, as usual in PCA, we subtract the column averages from each column. As a result, both the row and column sums in the matrix will be zero. We compute the singular value decomposition of the matrix X:

where Σ is a  diagonal matrix containing the singular values (which are all positive), and the columns of the

diagonal matrix containing the singular values (which are all positive), and the columns of the  matrix U and the

matrix U and the  matrix V contain the singular vectors. Since in our case

matrix V contain the singular vectors. Since in our case  , there will be only T nonzero singular values and only T relevant singular vectors; as usual, we keep only the relevant parts of the matrices, this way Σ will be only

, there will be only T nonzero singular values and only T relevant singular vectors; as usual, we keep only the relevant parts of the matrices, this way Σ will be only  and V will be only

and V will be only  [21]. The singular vectors are orthonormal, i.e.

[21]. The singular vectors are orthonormal, i.e.  , where I is the

, where I is the  identity matrix. It is customary to order the singular values and vectors such that the singular values are in decreasing order, so that the successive terms in the matrix multiplication in (1) give decreasing contribution to the result, thus giving a successive approximation of the original matrix. Note that these matrices can also be computed as the eigenvectors of the covariance matrices:

identity matrix. It is customary to order the singular values and vectors such that the singular values are in decreasing order, so that the successive terms in the matrix multiplication in (1) give decreasing contribution to the result, thus giving a successive approximation of the original matrix. Note that these matrices can also be computed as the eigenvectors of the covariance matrices:  and

and  for U and V respectively, and as such, and the columns of U and V span the row and column space of X. In accordance with this, we can interpret the singular vectors based on the interpretation of X. The columns of V can be considered as 'base networks', the matrix element vji provides the weight of edge j in base network i. According to (1), edge weights in the daily snapshots can be calculated as a linear combination of edge weights in the base networks. The singular values give the overall importance of a base network in approximating the whole time series, while the columns of U account for the temporal variation: the matrix element

for U and V respectively, and as such, and the columns of U and V span the row and column space of X. In accordance with this, we can interpret the singular vectors based on the interpretation of X. The columns of V can be considered as 'base networks', the matrix element vji provides the weight of edge j in base network i. According to (1), edge weights in the daily snapshots can be calculated as a linear combination of edge weights in the base networks. The singular values give the overall importance of a base network in approximating the whole time series, while the columns of U account for the temporal variation: the matrix element  provides the contribution of base network i at time t, e.g. the (normalized) weight of edge j on day t is given by:

provides the contribution of base network i at time t, e.g. the (normalized) weight of edge j on day t is given by:

3. Results

Examining the singular values, we find that for both type of core extraction they decay only relatively slowly, i.e. a large number of components are required to obtain a good approximation of the original matrix X (see figure 1). This indicates that the system possibly contains non-Gaussian noise and high dimensional structure. Also, the distribution of edge weights pi(v) in the base networks is fat-tailed; for the first six base networks we find very similar distributions, all well approximated with  for the LT core and

for the LT core and  for the AU core.

for the AU core.

Figure 1. Singular values of X. The inset shows the relative contribution up to the given index. The distribution of singular values is fat-tailed, a high number of components is required to explain the variations in the data. The best power-law fit is  .

.

Download figure:

Standard image High-resolution imageExamining the edges with large weights for the LT core, we find that most of these are repeated within the first few base networks. For example, if we consider the top-20 ranking edges (by the absolute value of weights) in the first ten base networks, we find only 46 distinct edges instead of the 200 maximally possible. Among these, 44 induce a weakly connected graph, including a total of 29 users; considering all edges among these users, 20 of them form a strongly connected component by themselves and all are weakly connected. These 29 users have a total of 1 349 815 separate Bitcoin addresses, forming a highly active subset in our core network.

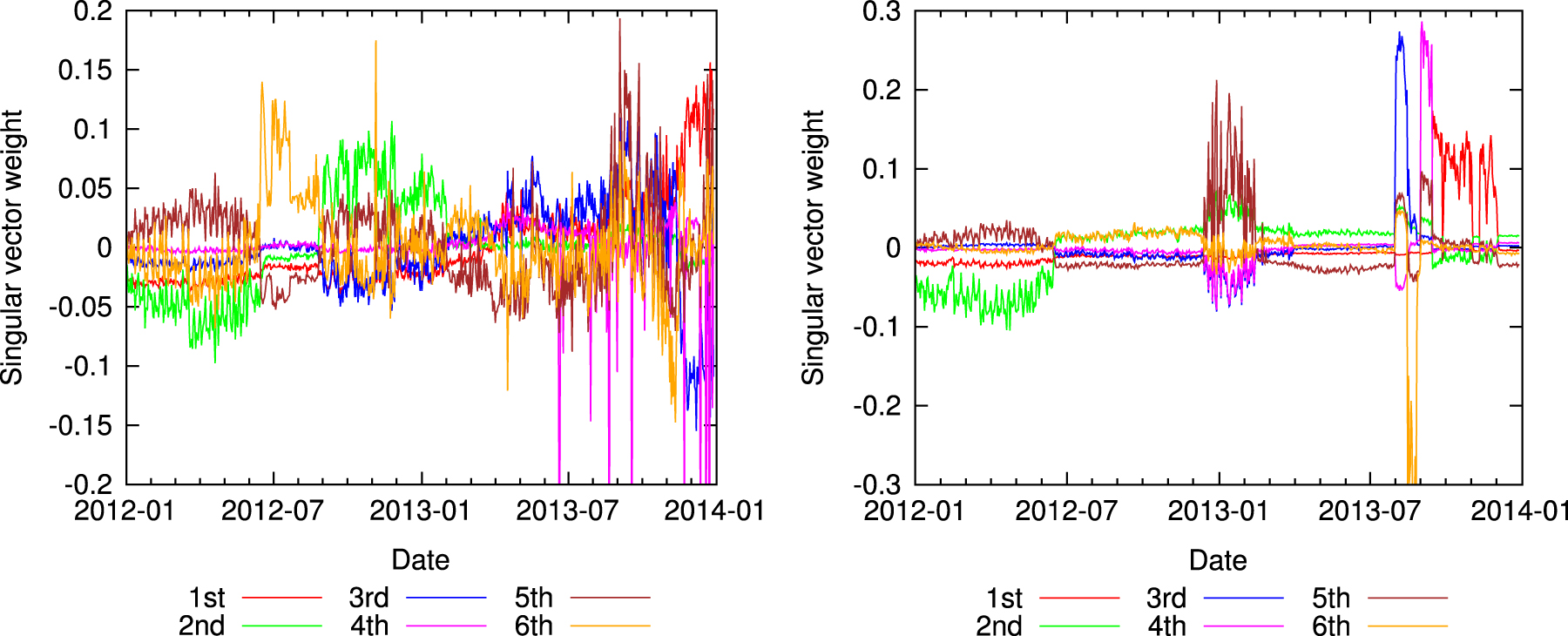

We show the time-varying contribution ui(t) of the first six base networks on figure 2. In most cases, ui(t) features a few abrupt changes, partitioning the history of Bitcoin into separate time periods. This is especially true for the AU core, where highly active but short lived users can significantly contribute. Identifying the individual nodes and edges responsible for network activity in a given period would require more information about Bitcoin addresses, which is difficult to obtain on a large scale.

Figure 2. The time-varying contribution ui(t) of the first six base networks, for the LT core (left) and AU core (right).

Download figure:

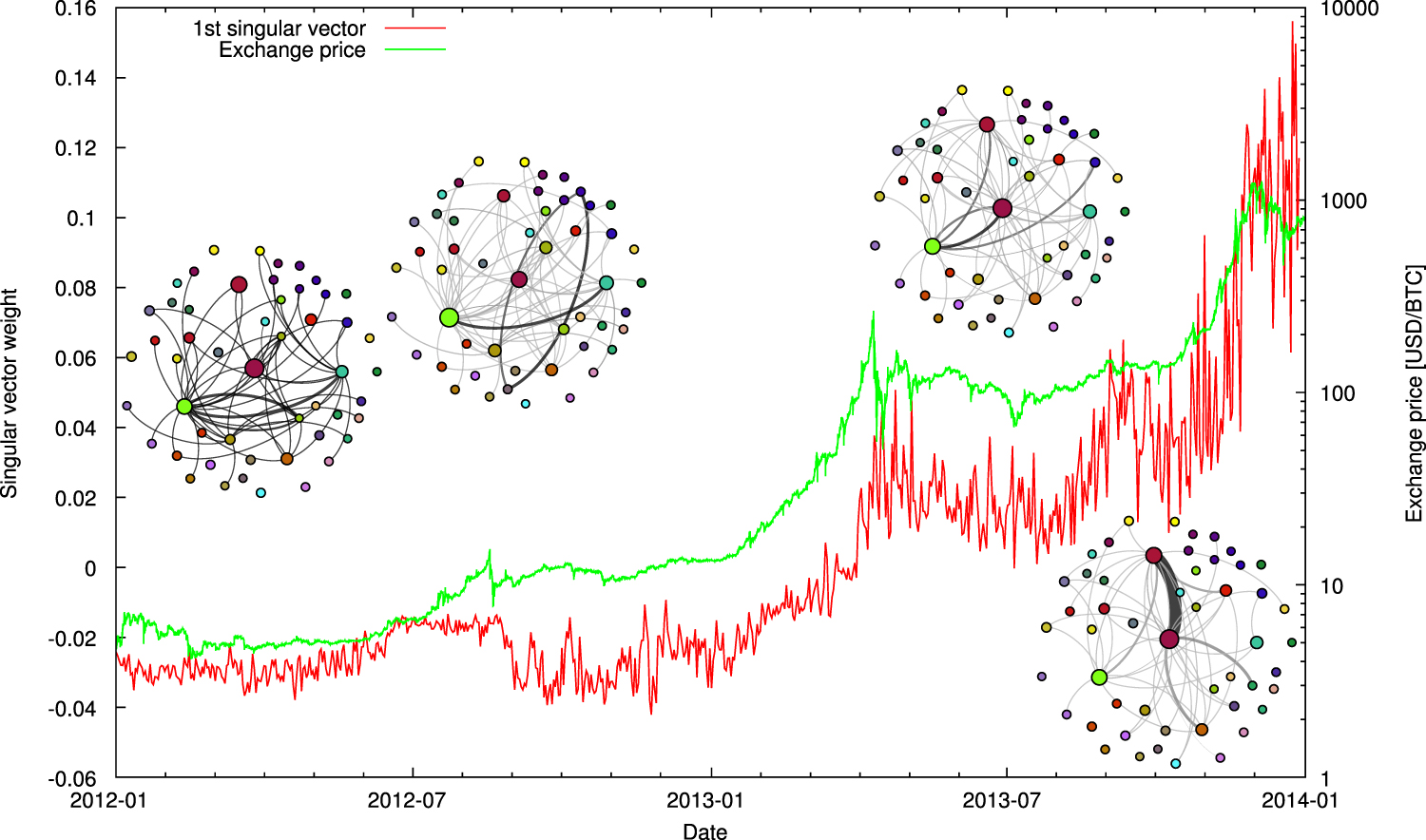

Standard image High-resolution imageThe most striking feature uncovered by our analysis is a clear correspondence between the first singular vector of the graph of long-term users and the market price of bitcoins as shown on figure 3. Apart from visual similarity, the two datasets have a significantly high correlation coefficients (see table 1).

Figure 3. The time-varying contribution of the first base network  for the LT core and the time series of the logarithm of exchange price at the MtGox trading site. To illustrate how this corresponds to changes in the network, snapshots of the subnetworks induced by top 100 edges with the largest absolute weight in the base network are also shown for a few dates. Visual inspection shows a good correspondence of the two; also, the two datasets have high correlation coefficients, see table 1.

for the LT core and the time series of the logarithm of exchange price at the MtGox trading site. To illustrate how this corresponds to changes in the network, snapshots of the subnetworks induced by top 100 edges with the largest absolute weight in the base network are also shown for a few dates. Visual inspection shows a good correspondence of the two; also, the two datasets have high correlation coefficients, see table 1.

Download figure:

Standard image High-resolution imageTable 1.

Correlation coefficients between the singular vectors of the network time series matrix and the Bitcoin exchange price. Left: first five singular vectors. Right: the five singular vectors with the highest correlation. Here,  is the Pearson correlation coefficient and

is the Pearson correlation coefficient and  is the Spearman rank correlation coefficient.

is the Spearman rank correlation coefficient.

| Long-term nodes | Most active nodes | Long-term nodes | Most active nodes | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Component |

|

|

|

|

Component |

|

|

Component |

|

|

| 1 | 0.8528 | 0.8654 | 0.3689 | 0.9231 | 1 | 0.8528 | 0.8654 | 10 | −0.5395 | 0.0075 |

| 2 | −0.0335 | 0.4367 | 0.1233 | 0.4435 | 3 | −0.3782 | 0.4407 | 7 | 0.3928 | 0.3633 |

| 3 | −0.3782 | 0.4407 | 0.0779 | −0.0268 | 21 | 0.1898 | 0.0466 | 1 | 0.3689 | 0.9231 |

| 4 | −0.074 | 0.5913 | 0.0972 | 0.3568 | 4 | −0.074 | 0.5913 | 11 | 0.3276 | −0.0578 |

| 5 | −0.0148 | −0.2991 | −0.1313 | −0.3066 | 19 | 0.0589 | 0.0423 | 8 | −0.2632 | −0.3631 |

Motivated by this result, we tested whether the price of bitcoins can be estimated with the ui(t) coefficients. To proceed, we subtract the average value from the price time series, and estimate this as a linear combination of singular vectors:

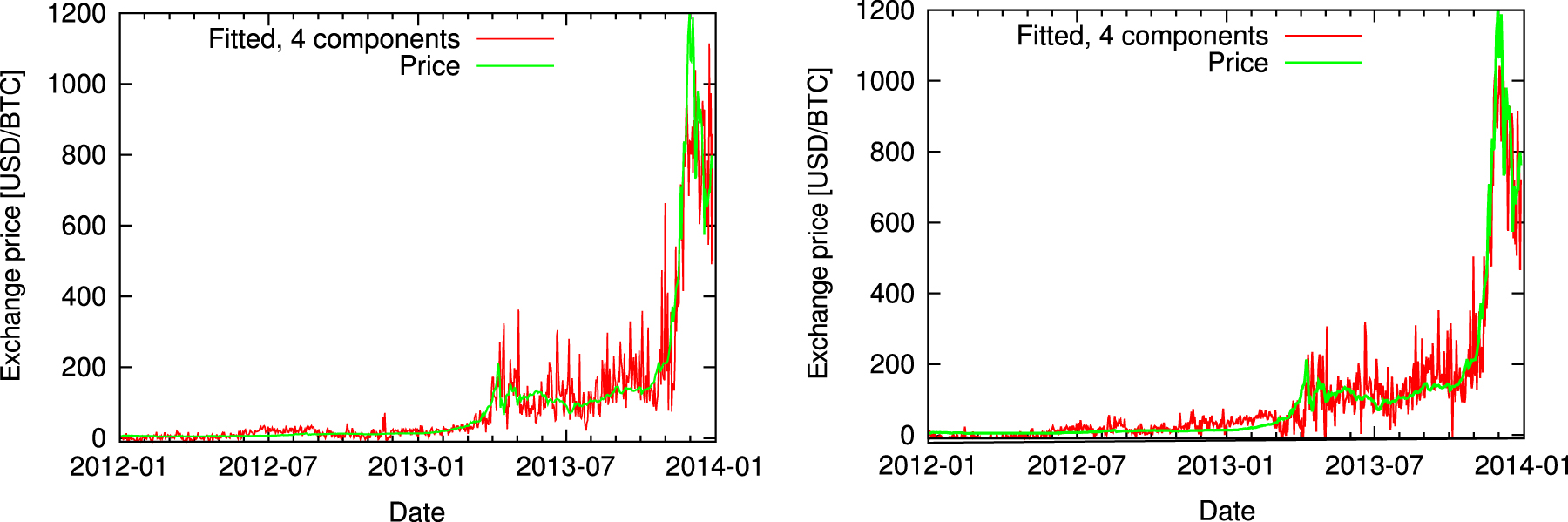

Here the coefficients ci can be computed as the dot product of the price time series and ui(t), and therefore ci is proportional to the Pearson correlation coefficients shown in table 1. We are interested how large N is needed to model the price time series with acceptable accuracy. We show the residual standard error as a function of N on figure 4. It is apparent that there are sudden decreases in the error after the inclusion of certain base networks. We note that the base networks are ranked by their contribution to the original network time series matrix, i.e. the singular values of X. On the other hand, we can rank these components by their similarity to the price time series by using correlation coefficients. This results in a more rapid decrease of the error, and the large jumps are all at the beginning. In table 1, we show the first few components with the highest correlation coefficients. Two approximations of the time series for the LT core is shown on figure 5; one with the first four base networks, the other with the four base networks whose time-varying contribution ui(t) has the highest correlation to the price. We find that in both cases most features of the time series are well approximated, but the fitted time series is still apparently noisy. In the first case, the shape of the peak at the end of 2013 is missed, while in the second case it is approximated much better. A closer examination of the correlation values (table 1) and the singular vectors reveals that the 21st component is responsible for this change, which contains high resemblance to the final section of the time series.

Figure 4. Residual standard error of approximating the exchange rate of bitcoins with a linear combination of the time-varying contribution of base networks.

Download figure:

Standard image High-resolution image

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 5. Approximating the exchange price of bitcoins with a linear combination of singular vectors of the time series matrix of the graph induced by the long-term nodes. Left: using the first four vectors ranked by singular values; right: using the first four vectors ranked by Pearson correlation with the price time series.

Download figure:

Standard image High-resolution image{kind=link}

4. Conclusions and future work

In this paper, we investigated whether connection between the network structure and macroscopic properties (i.e. the exchange price) can be established in the Bitcoin network. For our analysis, we reconstructed daily network snapshots of the networks of the most active users in a two-year period. We organized these snapshots into the graph time series matrix of the system. We analyzed this matrix using PCA which allowed us to identify changes in the network structure. A striking feature we found was that the time-varying contribution of some of the base networks show a clear correspondence with the market price of bitcoins. The contribution of the first base network was found to be exceptionally similar. Using the linear combination of only four vectors, we were able to reproduce most of the features of the long-term time evolution of the market price.

Based on our results, it is apparent that the analysis of the structure of the underlying network of a financial system can provide important new insights complementing analysis of the external features. Further research could focus on establishing causal relationship between the observed features, and possibly predicting price changes based on structural changes in the network. Also, collecting publicly available information about Bitcoin addresses identified as members of the highly active core of the network could result in a better understanding of the role of the associated users in the Bitcoin ecosystem, and help explain the correlations observed here.

Acknowledgments

The authors thank the partial support of the European Union and the European Social Fund through project FuturICT.hu (grant no.: TAMOP-4.2.2.C-11/1/KONV-2012-0013), the OTKA 7779 and the NAP 2005/KCKHA005 grants. EITKIC_12-1-2012-0001 project was partially supported by the Hungarian Government, managed by the National Development Agency, and financed by the Research and Technology Innovation Fund and the MAKOG Foundation.

Footnotes

- 1

Several open-source Bitcoin clients exist, see e.g. https://bitcoin.org/en/choose-your-wallet

- 2

http://satoshidice.com; their addresses used for the service start with '1Dice'.