Abstract

Momentum to phase out unabated coal use is growing globally. This transition is critical to meeting the Paris climate goals but can potentially lead to large amounts of stranded assets, especially in regions with newer and growing coal fleets. Here we combine plant-level data with a global integrated assessment model to quantify changes in global stranded asset risks from coal-fired power plants across regions and over time. With new plant proposals, cancellations, and retirements over the past five years, global net committed emissions in 2030 from existing and planned coal plants declined by 3.3 GtCO2 (25%). While these emissions are now roughly in line with initial Nationally Determined Contributions (NDCs) to the Paris Agreement, they remain far off track from longer-term climate goals. Progress made in 2021 towards no new coal can potentially avoid a 24% (503 GW) increase in capacity and a 55% ($520 billion) increase in stranded assets under 1.5 °C. Stranded asset risks fall disproportionately on emerging Asian economies with newer and growing coal fleets. Recent no new coal commitments from major coal financers can potentially reduce stranding of international investments by over 50%.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. Introduction

Historic steps were taken in 2021 to accelerate the transition away from coal power generation. Ahead of and during the United Nations Climate Change Conference (COP26) in Glasgow, many countries committed to stop building new coal plants, end international coal finance, transition away from coal, and reach net zero greenhouse gas (GHG) emissions [1–3]. With these commitments, the majority of new coal construction may come to an end. This is a marked acceleration of initial coal phaseout efforts over the past five years. While over three quarters of the global proposed coal capacity was cancelled between 2015 and 2021 [4], and total coal capacity declined in many OECD regions (for example, the U.S. and EU), global installed coal capacity has increased, as many countries continued to plan and build new coal power plants. As of January 2021, 503 GW of new capacity was under development globally, including 247, 66, and 100 GW in China, India, and Southeast Asia, respectively [5].

A rapid transition away from unabated coal use is essential to limiting the rise in global average temperature to 1.5 °C or 2 °C above pre-industrial levels. Coal combustion is responsible for a large fraction (currently, 44%) of global energy-related CO2 emissions and is the most emissions intensive way to produce electricity [6]. The window for action to meet the 1.5 °C goal is narrowing, and feasible pathways show unabated coal generation declining by 59%–78% by 2030 (relative to 2010 levels) and reaching near-zero by 2050 [7]. Given the large committed emissions from current fossil fuel infrastructure [8] and the need to quickly reduce emissions from coal, minimizing construction of new coal plants will be essential to meet climate goals. Previous research has quantified the risks posed by potential future emissions from existing energy infrastructure (including the coal sector) and fossil fuel reserves at global and regional levels [9–14]. Even with rapid implementation of a no new coal strategy, additional action to shorten lifetimes or reduce capacity factors of existing plants will likely be necessary to meet the 1.5 °C or 2 °C goals [15, 16].

Canceling new additions to the global coal fleet will have important effects on the economics of climate mitigation as new plants present a significant increase in stranded assets risks. Stranded assets are assets that experience a premature or unanticipated decline in value due to changing external factors [17, 18]. They not only pose economic risks to project owners but also, if they occur at a large scale, may cause significant damages to the broader financial system and macroeconomy [19–21]. These risks only increase with delayed climate action [19] and specifically with continued expansion of fossil fuel infrastructure [22]. Recently, a number of studies have calculated stranded assets under different climate policies [23], in units of unused capacity [9, 18, 22, 24–26], forgone profits [27–29], value at risk [16, 30–33], unrecovered capital cost [34–40], or global wealth loss [36] (see section 3 of the supplementary information for a detailed overview of estimates available online at stacks.iop.org/ERL/17/024029/mmedia). Several studies compare plant-level data with existing decarbonization scenarios [24–27, 34, 35, 41–47] or develop new scenarios using more aggregated infrastructure assumptions [10, 22, 25, 28–31, 36–38]. Research linking these two approaches is more limited and focuses on committed emissions and lifetime limits or fossil fuel reserves rather than stranded assets from power plants [15, 36, 39]. A more detailed accounting of stranded assets is essential for understanding the potential benefits of a no new coal policy.

Building on existing literature, this research fills several major gaps. First, we quantify the progress made in the past five years due to changes in the total coal project pipeline (both existing and planned capacity) and what further actions are needed to meet long-term 1.5 °C or 2 °C goals. Second, we quantify the changing stranded asset risks from existing and proposed coal power plants, by bridging a recent global plant-level database with a state-of-the-art integrated assessment model. This approach enables us to examine stranded assets from early coal retirements under the Paris goals at a more granular level, across plants and regions. We also investigate regional asset stranding from the perspective of international investors. Third, we look at alternative scenarios for near-term actions, where all proposed coal plants in the pipeline as of January 2021 are either cancelled or built within the next ten years. From these scenarios, we quantify the potential benefits—in terms of savings due to avoided stranded assets—from the progress made in 2021 towards no new coal.

We find that stranded asset risks from coal plants yet to be built have decreased over the past few years but remain globally significant. An immediate no new coal strategy would significantly reduce the risk of stranded assets—in fact, with a no new coal policy, a 1.5 °C climate target can be met with less asset stranding than would be expected under a 2 °C target but with delayed action on no new coal (i.e. where all plants currently in the pipeline come online as scheduled). Coal plant assets at risk of stranding are held disproportionately by emerging economies in Asia with newer and growing coal fleets, and these countries may see a large fraction of their fleet value stranded. If we account for the country where the owner company is headquartered, rather than the country where the plant is located, stranded asset totals are further concentrated in China as well as the U.S., Europe, South Korea, and Japan. New commitments from major coal financing countries to end international financing of new plants help reduce their stranded assets.

2. Methods

We examine the stranded asset risks from existing and proposed power plants under alternative near-term trends to reach the 1.5 °C and 2 °C climate goals. Specifically, we look at two different pathways to reach the same climate target, with alternate assumptions of near-term coal buildout (see section 2.3). For the first pair of pathways, no new coal plants come online after 2020 and economy-wide mitigation begins immediately. For the second pair of pathways, all coal plants currently under development come online by 2030, and mitigation from coal power and other sectors is delayed until after 2030.

We first compare potential future emissions from the current coal pipeline to that from five years ago to quantify the emission impacts of recent coal trends. The Global Change Analysis Model (GCAM), an integrated assessment model, is then used to simulate changes in coal power generation and other sectors to meet the 1.5 °C and 2 °C targets. We also use plant-level data to develop regional coal plants phaseout pathways under each decarbonization scenario.

2.1. Global plant-level coal data

Plant-level data on the global coal fleet was obtained from the Global Coal Plant Tracker (GCPT) database by Global Energy Monitor (GEM) [5]. GCPT provides data on coal plants currently operating as well as those that are under construction, permitted, in pre-permit development, announced, mothballed, shelved, cancelled, and retired. The database includes the plant location, capacity, stage of development, investor company or companies, and an estimate of the overnight capital cost and is updated every six months. We used the January 2021 version of the GCPT database in our analysis. A small number of plants in the database were missing data on capacity (two plants) and the year when they began operation (2% of plants). For these, we conservatively assumed a capacity of 350 MW and a start date earlier than the design lifetime. To the extent that plants with missing data were larger or newer, this approach could lead to a slight underestimate of stranded assets in our calculations. Regional capacity factors were taken from EIA and the capacity factor for South Korea was set to 0.62 (see section 4 of the supplementary information) [48].

To calculate stranded assets by investor region, we also matched the location, by country, of the parent company headquarters for each coal plant in the dataset. First, we used fuzzy matching to connect the GCPT database with the Global Coal Exist List (GCEL) database [49], which includes company names and locations for many coal plants. Second, for the parent company headquarters not identified in the first step (and to conduct spot checks for the automatic matches), a manual search was completed. This entailed using Google's search engine to identify parent company headquarter locations. For parent companies with common names, both the terms 'energy' and 'coal' were used to specify the search.

For plants with multiple investors, we focused on the largest or first investor listed in the GCEL database. We used this approach because the GCEL database does not list the percentage of investments for all investors, and as a result we cannot assign a fraction of stranded assets to all investors. (For plants where investor percentages are listed, the largest investor is listed first.) This approach tends to overestimate stranded assets for the primary investors while underestimating it for the smaller investors that are sometimes domestic companies.

2.2. The GCAM

This study uses the GCAM version 5.3, an open-source integrated assessment model developed and maintained by the Pacific Northwest National Laboratory and the Joint Global Change Research Institute at the University of Maryland (https://github.com/JGCRI). GCAM represents relationships among five global systems at various spatial scales: economics, energy, water, climate, and agriculture and land use. Market equilibrium is the operating principle for GCAM, and assumptions regarding regional population and labor productivity growth are combined with physical, technological, and economic parameters to solve for equilibrium market prices and quantities. Using a run period extending through 2100 at five-year intervals, GCAM tracks several influential climate parameters such as temperature, radiative forcing, and the emissions of 16 greenhouse gases, aerosols and short-lived species at a 0.5 × 0.5 degree resolution.

GCAM, and integrated assessment models more broadly, are useful for exploring the implications of different technology and policy choices for greenhouse gas reductions and climate change. As GCAM encompasses an array of complex interactions, it continues to serve the Intergovernmental Panel on Climate Change (IPCC) in the production of Assessment Reports (ARs) [50–52], Representative Concentration Pathways (RCPs) [53], and Shared Socioeconomic Pathways (SSPs) [54].

2.3. Scenario development

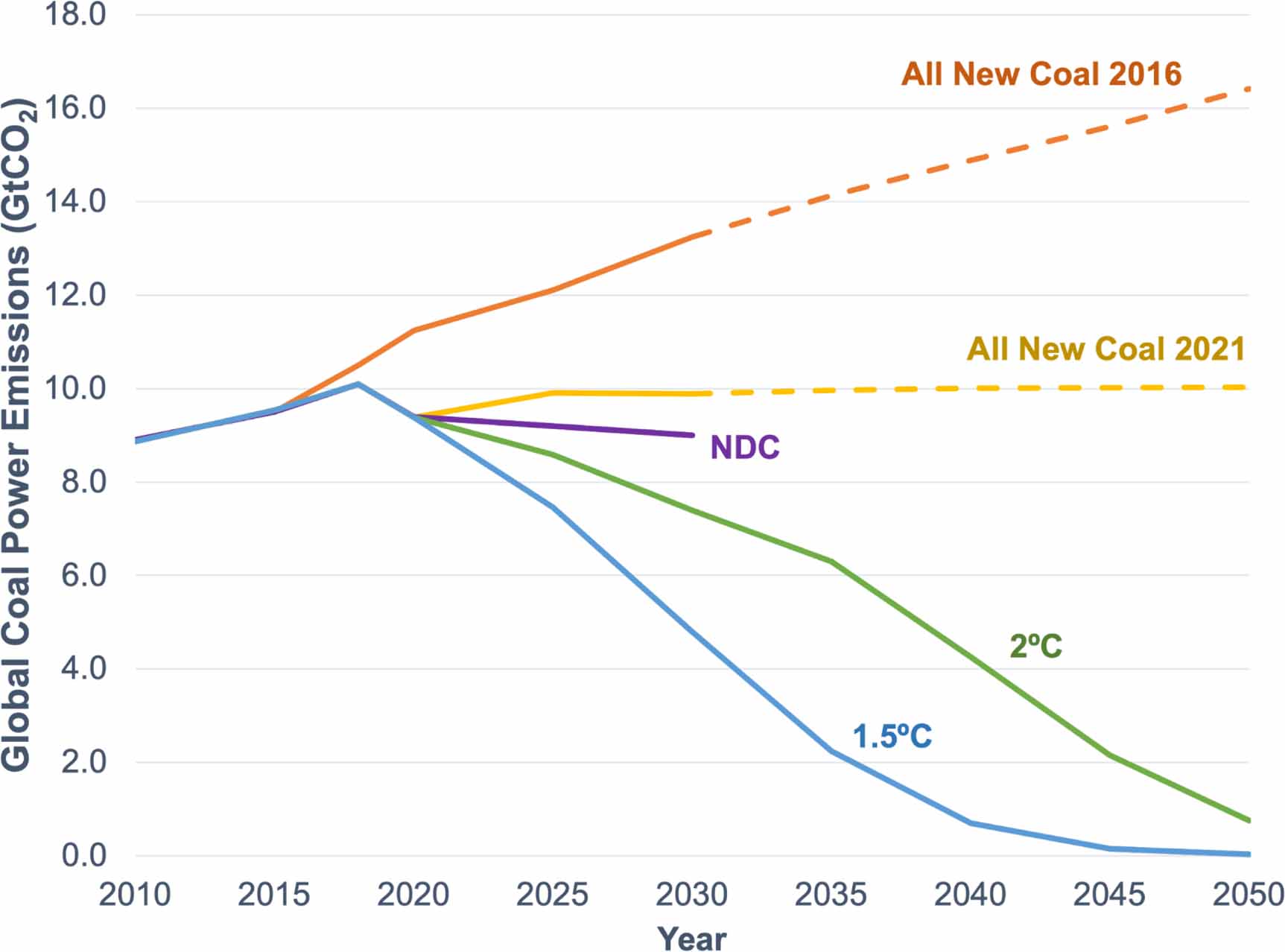

We use the plant-level data on existing and proposed coal plants to develop scenario inputs for GCAM to explore the implications of delayed action on no new coal. We examine three scenarios for the global coal fleet: (a) all proposed plants in 2016 come online as scheduled (the All New Coal 2016 scenario), and growth in the global coal fleet continues at the same rate, (b) all proposed plants in 2021 come online as scheduled (the All New Coal 2021, All New Coal to 1.5 °C and All New Coal to 2 °C scenarios), and (c) no new coal plants are built (the No New Coal to 1.5 °C and No New Coal to 2 °C scenarios). For the near-term trends in coal buildout, we translate current and/or planned coal capacity into GCAM inputs. All coal plants currently in the pipeline come online by 2025 (for plants that are already under construction or have received official approvals) or 2030 (for plants that are in the permitting stage or have been announced). For the deep decarbonization scenarios, we apply increasing global carbon prices to all GHG emissions to simulate pathways for meeting the 1.5 °C and 2 °C Paris goals. We also simulate coal trajectories where coal plants live out their historical average lifetimes in the absence of policy or market forces to accelerate coal retirement. We also examine coal generation and emissions for a case where countries collectively meet their near-term nationally determined contributions (NDCs), which outline country-level efforts to reduce national emissions and adapt to the impacts of climate change [55]. See table 1 for an overview of the scenarios included in our analysis and figure 1 for a comparison of our scenario and others in the literature.

Figure 1. Comparison of the GCAM scenarios applied in this paper to the IAMC 1.5 °C Scenario Explorer database: (a) global cumulative net CO2 emissions since 1875; (b) global net CO2 emission pathways; (c) global coal power generation without carbon capture and storage (CCS). The lighter lines are scenarios from the IAMC 1.5 °C Scenario Explorer [56]. The light blue lines indicate scenarios categorized as below 1.5 °C and 1.5 °C low overshoot, and the light green lines indicate scenarios categorized as lower 2 °C in the database.

Download figure:

Standard image High-resolution imageTable 1. Scenario overview.

| Scenario name | Near-term trend of coal buildout | Climate actions all sectors | Climate target |

|---|---|---|---|

| All New Coal 2016 | Based on 2016 pipeline, all proposed coal plants are implemented, continued growth to 2050 | None | None |

| All New Coal 2021 | Based on 2021 pipeline, all proposed coal plants are implemented, continued growth to 2050 | None | None |

| NDC | Coal pathways resulted from economy-wide carbon price to reach NDC targets | Apply the same economy-wide carbon price to reach NDC targets | NDC by 2030 |

| No New Coal to 1.5 °C | No new coal is added after 2020 | Immediate climate action after 2020, applying the same economy-wide carbon price to reach the climate target | 1.5 °C |

| No New Coal to 2 °C | No new coal is added after 2020 | Immediate climate action after 2020, applying the same economy-wide carbon price to reach the climate target | 2 °C |

| All New Coal to 1.5 °C | Based on 2021 pipeline, all proposed coal plants are implemented by 2030; no new coal is added after that | Delayed climate action until after 2030, applying the same economy-wide carbon price to reach the climate target | 1.5 °C |

| All New Coal to 2 °C | Based on 2021 pipeline, all proposed coal plants are implemented by 2030; no new coal is added after that | Delayed climate action until after 2030, applying the same economy-wide carbon price to reach the climate target | 2 °C |

2.4. Stranded asset calculations

We calculate stranded assets under a 1.5 °C and 2 °C climate policy, for cases where all coal plants currently in the pipeline are built and where no new plants are built. For each policy scenario, we extract future coal generation (at five-year time steps) from GCAM. We then compare regional generation to the levels that would be expected if all plants lived out historical average lifetimes (and operated at constant capacity factors). If these generation levels exceed those in the policy scenario, we simulate plant retirements oldest to youngest in each region to meet the target levels. On the one hand, this is a conservative approach—to the extent that local constraints and other factors lead to retirements of some younger plants before older ones, total stranded assets would be underestimated, On the other hand, strategies like lower plant utilization or CCS retrofitting, which we do not model in this analysis, may help reduce stranded assets.

We calculate stranded assets as the overnight capital cost (OCC, in units of $ per kW) of each plant times the capacity (K) and the fraction of its expected lifetime (L) that it does not live out due to an earlier-than-expected retirement age (R):

Overnight capital costs are estimated regionally from GEM [57]. Stranded assets depend on a variety of factors and are estimated in the literature using different approaches. Following several recent studies [40–46], we use unrecovered capital cost as a measure of stranded asset. Calculations in the literature typically use either physical or economic lifetimes; we use physical (i.e. historical global average) lifetimes in our analysis. Because physical lifetimes are generally longer than economic ones, this approach will lead to higher estimates of stranded assets and partially reflects the fact that forgone earnings are experienced even after assets exceed their economic lifetimes. We also examine the sensitivity of our results to the plant lifetime and cover a range that captures typical economic as well as physical lifetimes.

3. Recent coal trends and the Paris goals

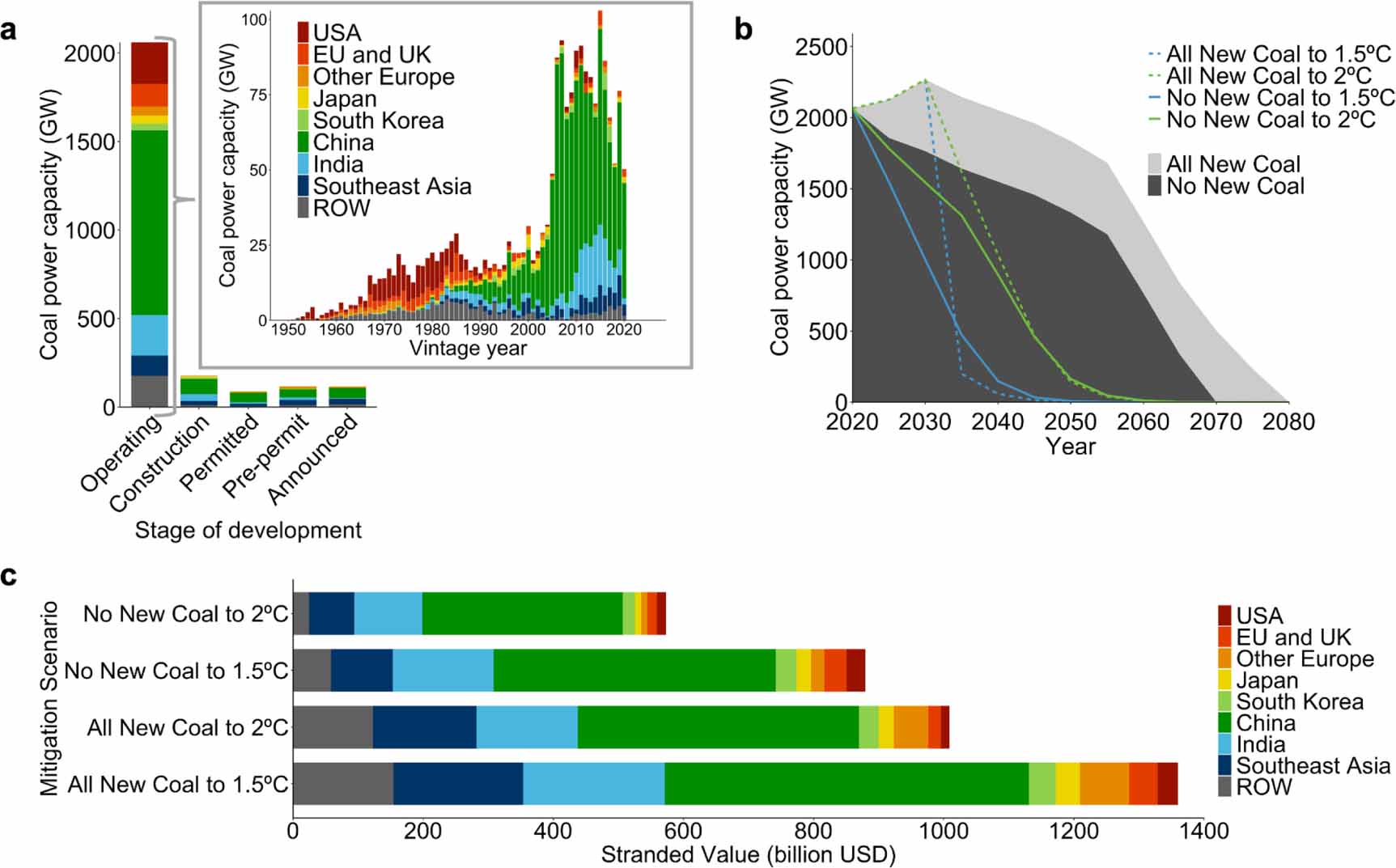

Over the past few years, the global pipeline of existing and proposed coal power plants shrank by 659 GW (see figure 2). While total installed capacity increased by 119 GW between 2016 and 2021, proposed capacity declined by over 60%. A total of 779 GW of new projects in the planning, permitting, or construction stages were cancelled. At the regional level, the U.S. and Europe are shifting away from coal, representing 59% of retirements at 69 GW and 56 GW, respectively. However, coal reliance remains strong elsewhere. China continues to be the largest owner and builder of coal plants, with 1049 GW installed and 247 GW proposed, contributing 66% of capacity additions from 2016 to 2021. India contributes another 229 GW installed and 66 GW proposed capacity. However, China and India together also make up almost 70% of net project cancellations between 2016 and 2021, at 364 GW and 177 GW, respectively. New project proposals have also trended downward over this period.

Figure 2. Changes in the global coal power pipeline from 2016 to 2021. The global pipeline of operating and proposed coal power capacity declined by 659 GW over the past four years, driven mainly by new project cancellations in China, India, and elsewhere, with smaller contributions from plant retirements.

Download figure:

Standard image High-resolution imageRecent trends in the global coal fleet have implications for meeting near- and long-term climate policy goals. Figure 3 shows emission pathways from the 2016 to 2021 coal pipeline, as well as to those under the near-term NDCs and long-term 1.5 °C and 2 °C goals. There has been significant progress in reducing committed emissions from the coal fleet over the past five years. If all currently proposed plants came online and operated for the global historical average lifetime (50 years), the resulting 2030 emissions from coal generation would be 3.3 GtCO2 (or 25%) lower than those expected from the 2016 pipeline, approaching the aggregate global NDCs. Yet there is a substantial gap between these trends and the long-term Paris goals. This gap indicates a potential for substantial asset stranding from both existing coal plants and new builds. Expected emissions in 2030 would need to be reduced by even more than the reduction between the 2016 and 2021 pipelines to be on track with these goals. There is an emission gap of 5.1 GtCO2 in 2030 to the 1.5 °C target.

Figure 3. Future emissions from the global coal pipeline and under the near- and long-term Paris goals. Expected emissions declined from 2016 to 2021 and are approximately in line with coal emissions under the NDCs; however, even greater reductions are required under the long-term 1.5 °C and 2 °C goals. (Solid lines in the All New Coal scenarios indicate expected emissions if plants in the pipeline come online as scheduled; dotted lines are a linear extrapolation of new builds between 2020 and 2030.)

Download figure:

Standard image High-resolution imageThese trends are driven by different factors across regions, including falling prices of competing technologies, air quality and climate policies, and public opposition to coal power plants. The COVID-19 crisis may also have near- and long-term impacts on the global coal pipeline. The global coal fleet shrank for the first time on record in the first half of 2020, due to both continued retirements and delays in commissioning [40, 58]. Coal demand also declined by approximately 8% in early 2020 [59], exacerbating overcapacity issues in coal-dominant regions. However, the second half of 2020 saw a reversal of this downward trend. Coal expansion was led by China, which commissioned three times as much new coal capacity—and announced five times as much—as the rest of the world combined [60]. At the same time, several countries have pointed to the potential benefits of green stimulus for economic recovery. The long-term evolution of the global coal fleet and stranded asset risks remains uncertain and will depend critically on planning and policy decisions in the next few years.

4. Global and regional stranded asset risks

Our results suggest that continued buildout of coal plants currently in the pipeline will greatly increase stranded asset risks (see figure 4). If all plants currently under development are built, we estimate that meeting the Paris climate goals will lead to $1.4 trillion in stranded assets under a 1.5 °C policy and $1 trillion under a 2 °C policy. If all proposed coal projects are cancelled, asset stranding under a 1.5 °C policy falls to $880 billion and stranding under a 2 °C policy falls to $573 billion. This represents a global savings of $427–520 billion from a no new coal policy. Additions from coal plants in the pipeline represent 24% of current operating capacity but 55% of stranded assets under 1.5 °C and 76% under 2 °C. This increase in stranded assets is caused by both the need to retire the newly built plants, themselves, and to retire existing plants more rapidly to reach the same climate goal. The relative difference between a no new coal and all new coal policy is smaller for the 1.5 °C goal because faster retirements of the current fleet are required even if no new plants are built.

Figure 4. Current status and future pathways for global coal capacity: (a) proposed coal capacity by stage of development with subset of operating coal capacity by vintage, (b) comparison of coal capacity pathways for no new coal and all new coal scenarios under 1.5 and 2 °C goals (lines) or if plants live out their historical average lifetimes (shaded regions), and (c) asset stranding under 1.5 and 2 °C policies if no new coal plants are built or all plants currently in the pipeline come online within the next ten years. (See supplementary figures S1–S7 for a version of figure (a) without operating capacity for a more detailed view of proposed plants and supplementary figures 3–1, and 3–2 for a comparison of our results to the literature.)

Download figure:

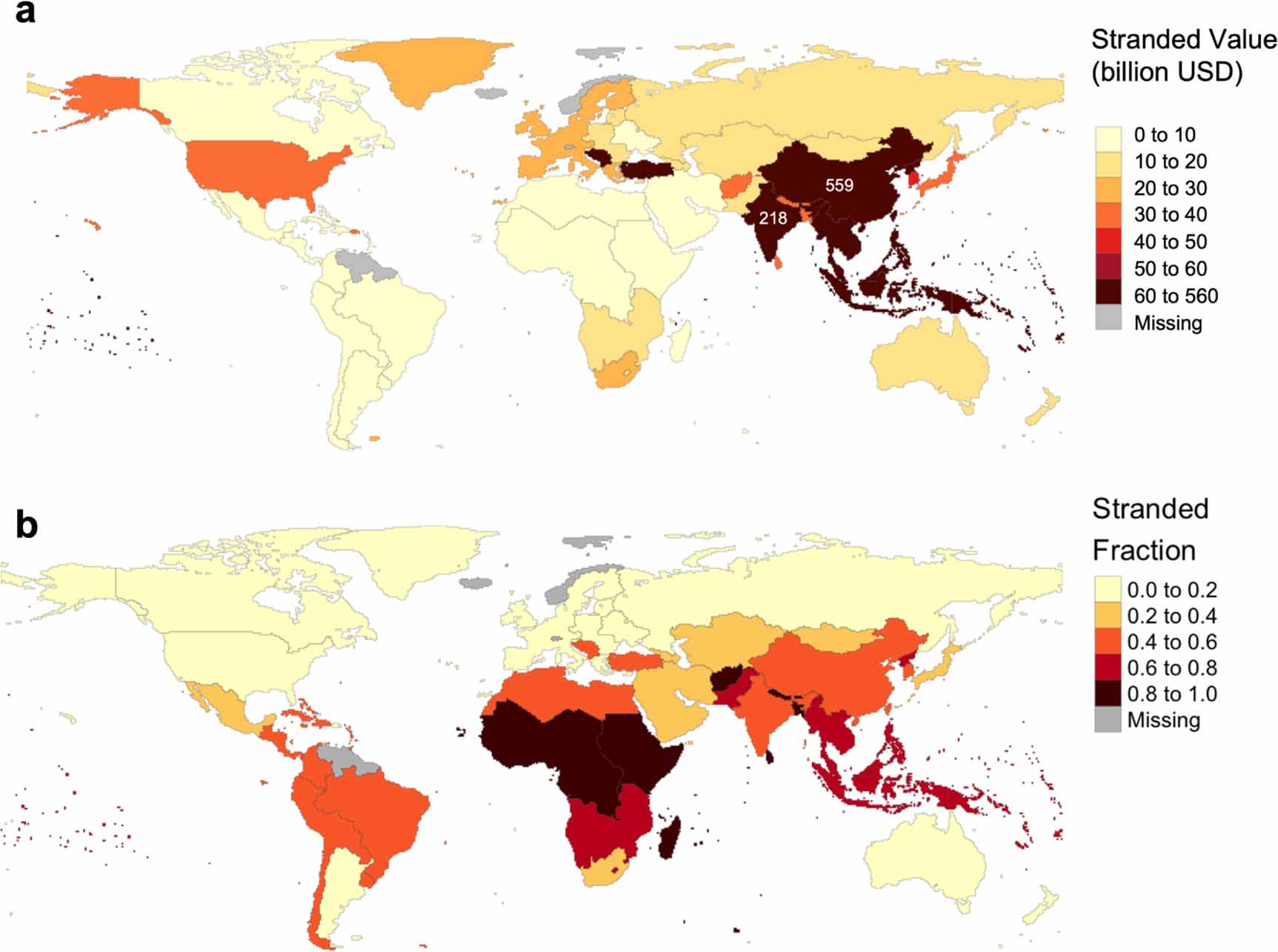

Standard image High-resolution imageRegions with newer coal fleets, especially with large amounts of capacity yet to be built, will incur disproportionately high stranded assets risks (see figure 5). Rapidly growing and emerging economies in Asia have the largest new and planned coal fleets. China has the highest value of stranded asset risks, representing 41%–55% of the global total across the scenarios examined here. India and Southeast Asia also see large amounts of asset stranding. Together, China, India, and Southeast Asia represent 50% of the savings (in terms of avoided stranded assets) from a no new coal policy. A number of regions have smaller overall coal fleets but represent hotspots where a large fraction of their fleet value is at risk of stranding under the Paris goals. If all new coal plants in the pipeline are built, a 1.5 °C policy leads to a large fraction of coal plant assets being stranded. Some areas in Asia and Africa—as well as non-EU Europe—see over a doubling of stranded asset risks. The U.S. and EU, with older coal fleets, see much smaller stranded assets in terms of both fraction of the fleet and total value.

Figure 5. Coal plant stranded assets by region under a 1.5 °C policy if all plants currently in the pipeline are built: (a) absolute level of stranded assets and (b) fraction of assets stranded. Immediate action on no new coal reduces asset stranding, with the largest relative differences seen in parts of Asia, Africa, and Latin America (see supplementary figures S1–S2, S1–S3 and S1–S4 for a comparison of immediate and delayed action for 2 °C).

Download figure:

Standard image High-resolution imageStranded asset risks may go beyond a plant's physical location, since some plants are developed by companies from other countries. To better understand the risks to project developers, we also calculate regional stranded assets based on the location of the primary investor company headquarters, rather than the physical plant location. A recent study on finance-based committed emissions illustrates the importance of this perspective [61]. We find that asset stranding increases for large investor countries and regions, including the U.S., Europe, Japan, South Korea, and China, with the U.S. and EU seeing the largest percent increase in stranded assets. All of these major investor countries have recently committed to end international financing of new coal plants [62–67]. We find that these commitments can potentially reduce the stranded assets of their overseas investments by over 50% under both a 1.5 °C and 2 °C policy. On the other hand, Southeast Asia, India, Australia, and parts of Africa and South America saw decreases in their stranded assets, with the largest percent decreases in Africa and Indonesia (see figure 6). Stranded assets whose region changed (based on the regional groupings in figures 5 and 6) accounted for approximately 3% of stranded assets in the No New Coal scenarios and 7%–8% in the All New Coal scenarios. Company and policy responses to stranded assets may depend on both the location of the coal plant and its investor companies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 6. Changes in regional stranded assets when assets are calculated based on region of the company headquarters rather than the plant location. Positive values indicate that stranded assets are greater when the assets are assigned to the location of the company headquarters rather than the location of the plant. The magnitude of the positive and negative values is the same for each scenario, since the total value of stranded assets in each scenario does not change.

Download figure:

Standard image High-resolution image{kind=link}

5. Discussion

Committed emissions from the existing and proposed global coal fleet have declined over the past few years. However, the risk of asset stranding to meet the Paris goals remains significant. We find that, if all proposed coal plants as of January 2021 are built as scheduled, stranded assets may reach $1.4 trillion under a 1.5 °C policy and $1 trillion under 2 °C. These new plants would represent 24% of current capacity (503 GW) but 55% and 76% of stranded assets under 1.5 °C and 2 °C goals, respectively, with larger differences in regions with plans to build new coal plants. Progress made in 2021 toward no new coal has potentially avoided $520 billion in stranded assets under 1.5 °C and $427 billion under 2 °C. Previous studies have not investigated stranded assets from coal power plants under the scenarios we present here; however, our results on the overall level of asset stranding are generally in line with previous estimates (see section 3 of the supplementary information). While some asset stranding is likely under any climate policy [8], new plants have an outsized impact on stranded assets that can be avoided if these plants are not built. Stranded asset risks also fall disproportionately on rapidly-growing and emerging economies with large, new coal fleets. Consequently, an accelerated coal phaseout brings very different impacts across regions, with disparities growing if no new coal commitments are delayed.

Calculations of stranded assets are also subject to many uncertainties, including plant lifetimes, overnight capital costs, costs of financing, and costs of emission controls and other upgrades. The total magnitude of stranded assets is uncertain, but the finding that a no new coal policy would significantly reduce asset stranding is robust to these uncertainties. While the global average lifetime at retirement for coal plants is approximately 50 years, lifetimes vary significantly across plants and locations. For example, coal plants in the U.S. can have lifetimes well beyond 50 years, and new investments in emissions controls may lead to asset stranding even for old plants. Conversely, in China, plants typically have a design lifetime of 30 years [15, 60]. Lifetimes are also considerably shorter than the global average due to accelerated retirement of small, high-polluting units. Immediate action on no new coal could result in near zero stranded assets with a 20 year lifetime under 1.5 °C and a 30 year lifetime under 2 °C (see section 2 of the supplementary information). If all proposed plants as of January 2021 are built, stranded assets can be significant even if plant lifetimes are limited to 20 years. Additionally, the effects of stranded assets depend critically on dynamics in the financial system, and investor expectations about climate policy may enable or hamper a smooth energy transition [68].

The most effective strategy for reducing stranded assets is to stop building new coal plants. Since many coal plants currently in the pipeline have not yet begun construction (64%), there is an opportunity to avoid these stranded assets risks with relatively small sunk costs. A rapid coal phaseout will be most effective and equitable if it incorporates principles of just energy transitions [69, 70]. These include providing transition assistance and job opportunities for workers in the coal sector [71, 72] and resources to support low-carbon energy investments in developing countries as well as low-income and minority communities in all countries [73, 74]. Building new coal plants may exacerbate just transition challenges. While emerging Asian economies have large, young coal fleets, and a significant amount of capacity still in the pipeline, many countries in Latin America, Africa, and Asia could see a large fraction of their coal assets stranded. For plants that have already been built, refinancing can be a useful strategy for enabling early retirement, especially in developing countries [75], and is an important area for future research. There are also opportunities to reduce stranded assets by lowering utilization levels and retrofitting existing plants with CCS.

Stranded assets also present significant opportunity costs for climate policy. While the total investment required to meet climate goals depends on many factors (and in some sectors may be lower than business as usual levels [76]), estimates put the investment gap at over $300 billion per year for a 2 °C policy and close to $500 billion per year for 1.5 °C [77]. Yet simply not building coal plants in the January 2021 pipeline could free up two to three times this amount of capital. To better understand the full financial implications of the energy transition, future research could compare investment gaps and avoided stranded assets over time and for other fossil-based infrastructure, especially outside the electricity sector [14, 20] and at scales relevant for local planning and policy [23]. Achieving climate goals will require a substantial mobilization of climate finance and stronger commitments from countries with greater ability and historical responsibility to address the climate crisis. A no new coal policy can play a critical role in reducing emissions and enabling investment while reducing asset stranding under the Paris climate goals.

Acknowledgments

The authors acknowledge funding support from Bloomberg Philanthropies, ClimateWorks Foundation, and the University of Wisconsin—Madison Office of the Vice Chancellor for Research and Graduate Education with funding from the Wisconsin Alumni Research Foundation.

Data availability statement

The data that support the findings of this study are openly available at the following URL/DOI [5]: https://globalenergymonitor.org/projects/global-coal-plant-tracker/download-data/.

Conflict of interest

The authors declare no competing interests.

Author contributions

M R E and R C coordinated the research, designed the scenario and data analysis, created the figures, and led the writing of the paper. N H, H M, and G I contributed to the study design. M B contributed to the scenario analysis and figures. K M, J S, and A Z contributed to the data collection and analysis. All authors provided feedback and contributed to writing the paper.

Code availability

The Global Change Analysis Model is an open-source integrated assessment model, available at https://github.com/JGCRI/gcam-core/releases. Data processing is conducted using R 3.6.3. All figures are created using R 3.6.3.