Harnessing the Full Potential of Industrial Demand-Side Flexibility: An End-to-End Approach Connecting Machines with Markets through Service-Oriented IT Platforms

, , , , , ,

, , , , , ,

Abstract

:Featured Application

Abstract

1. Introduction and Motivation

2. State-of-the-Art

2.1. Fundamentals of Demand-Side Management and Demand-Side Response

- Generation: new flexibility on the supply side

- Transmission: flexibility through the expansion of the power grid

- Storage: flexibility through storage

- Sector coupling: flexible conversion of energy between energy sectors

- Consumption: flexibility through DR

2.2. Industrial Energy Procurement

2.3. Requirement Profiles for Industrial Demand-Side Response

2.4. Energy Flexibility for Industrial Companies

2.5. Platform Ecosystems

2.5.1. Manufacturing IT Platforms

2.5.2. Market-Side Platforms and Services

2.6. Preliminary Conclusions

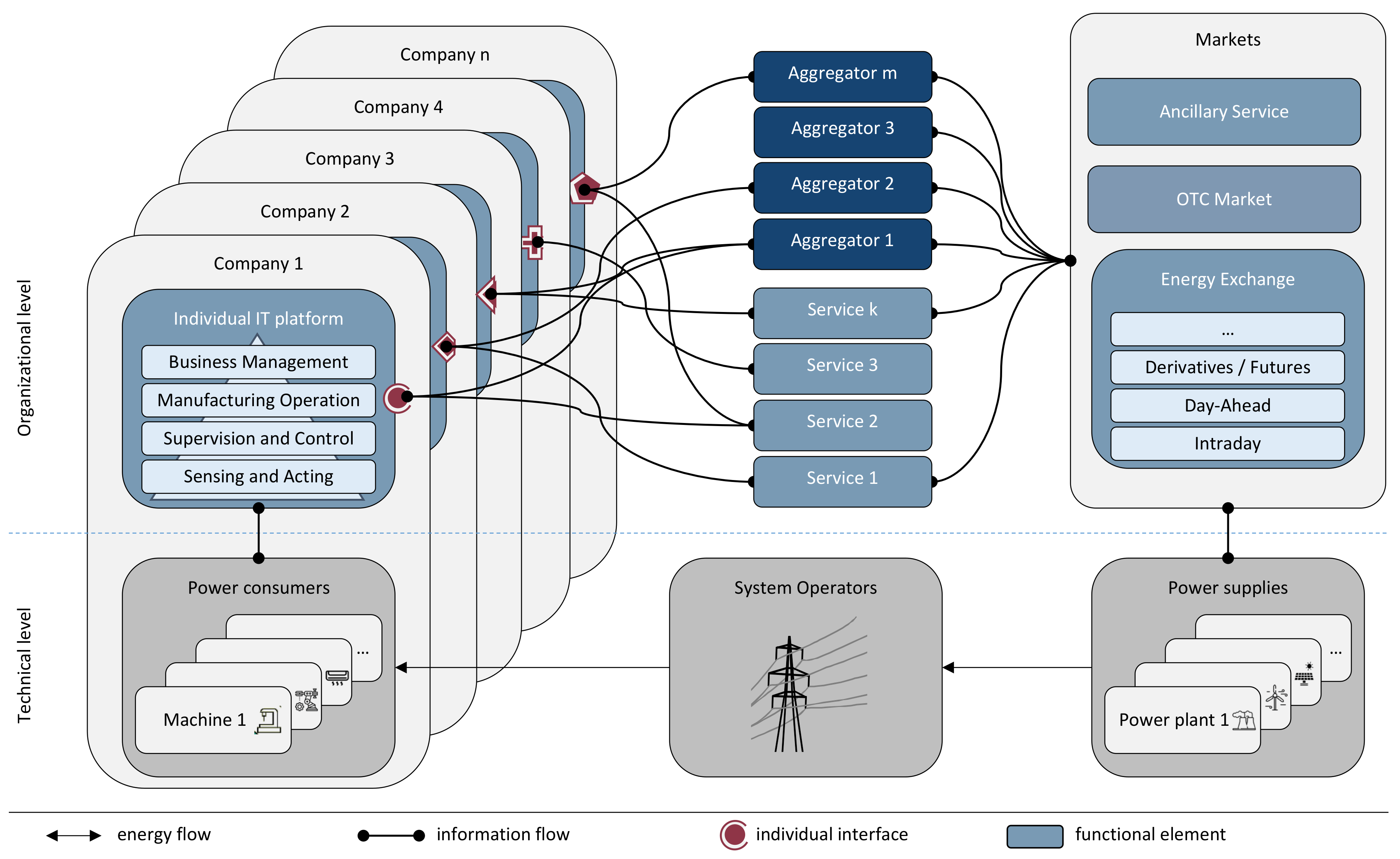

3. Industry Specification Analysis

- Functionality: The automated synchronization of industrial energy consumption and supply requires several different partners and functional levels from the energy market down to single machines to be involved. The increasing number of participating companies and the increasing challenges to balance the power grid make automated synchronization necessary. For this reason, an end-to-end approach is required, which defines the continuous information flow throughout all relevant stages and maps the following three central use cases: procurement of market information (e.g., price forecasts), evaluation of flexibility (e.g., ideal marketing time), and marketing of flexibility (on the appropriate target market). In addition, information on energy consumption needs to be equally considered within manufacturing. Thus, appropriate functionalities throughout all organizational levels of a company are required.

- Interoperability: Currently, a variety of communication protocols, data models, and IT systems are used in manufacturing. On top of that, energy markets and grid providers apply several interfaces and data models. Consequently, interoperability is another important requirement to enable a high number of heterogeneous companies to take part in a flexible manner. The integration of existing standards, shaping a transferable and robust architecture, as well as the harmonization of data models are crucial for the development of a new ecosystem in the context of energy flexibility.

- Free competition: To achieve wide acceptability and to offer incentives for companies to participate in the energy markets, a solution needs to be offered that ensures free competition. Accordingly, obstacles for new market actors need to be minimized, and an open ecosystem must be offered that provides flexible access to the services of different providers. In addition, industrial companies and other participants should be able to extend independently the functionalities of and solutions to their and their customers individual needs.

- Privacy and security: Privacy and security are key requirements for companies to participate. The detailed energy consumption contains crucial information about a manufacturing company, because for example, the given utilization or the used technology can be derived. Thus, no confidential information about energy consumption, etc., should be provided to external competitors. Besides privacy, security probably plays an even more important role. As energy systems are part of the critical infrastructure, the highest security standards need to be adopted, and given specifications need to be fulfilled, e.g., [75]. In addition, data leaks have to be prevented to ensure that personalized information does not fall into the wrong hands.

- Credibility and trustworthiness: The pursued solution should offer the possibility to purchase and sell energy flexibility automatically. Therefore, signing legally-binding digital contracts is an additional essential requirement. For this purpose, appropriate services and processes need to be established that at the same time provide proper technical solutions to ensure trustworthiness in terms of traceability and transparency.

- Market entry threshold: The specification analysis also involved the current market design and resulted in requirements for key changes. In order for demand flexibility to be used to its full extent, sanctioning flexibility by network charges needs to be eliminated. Furthermore, a non-discriminatory access to all flexibility markets needs to be ensured.

- General architecture requirements: Considering the discussed requirements for IT-based automated industrial DR, additional specifications regarding the architecture can be derived. In particular, modularity and extensibility are very important in order to provide the required reusability, adaptability, and scalability of the solution. These requirements can be summed up with the concept of service-oriented architectures. In addition, near real-time processing, as well as robust and reliable communication flows are essential. Furthermore, different deployment models, e.g., private or public cloud solutions, should be possible.

4. Research Deficit

4.1. End-to-End Approach

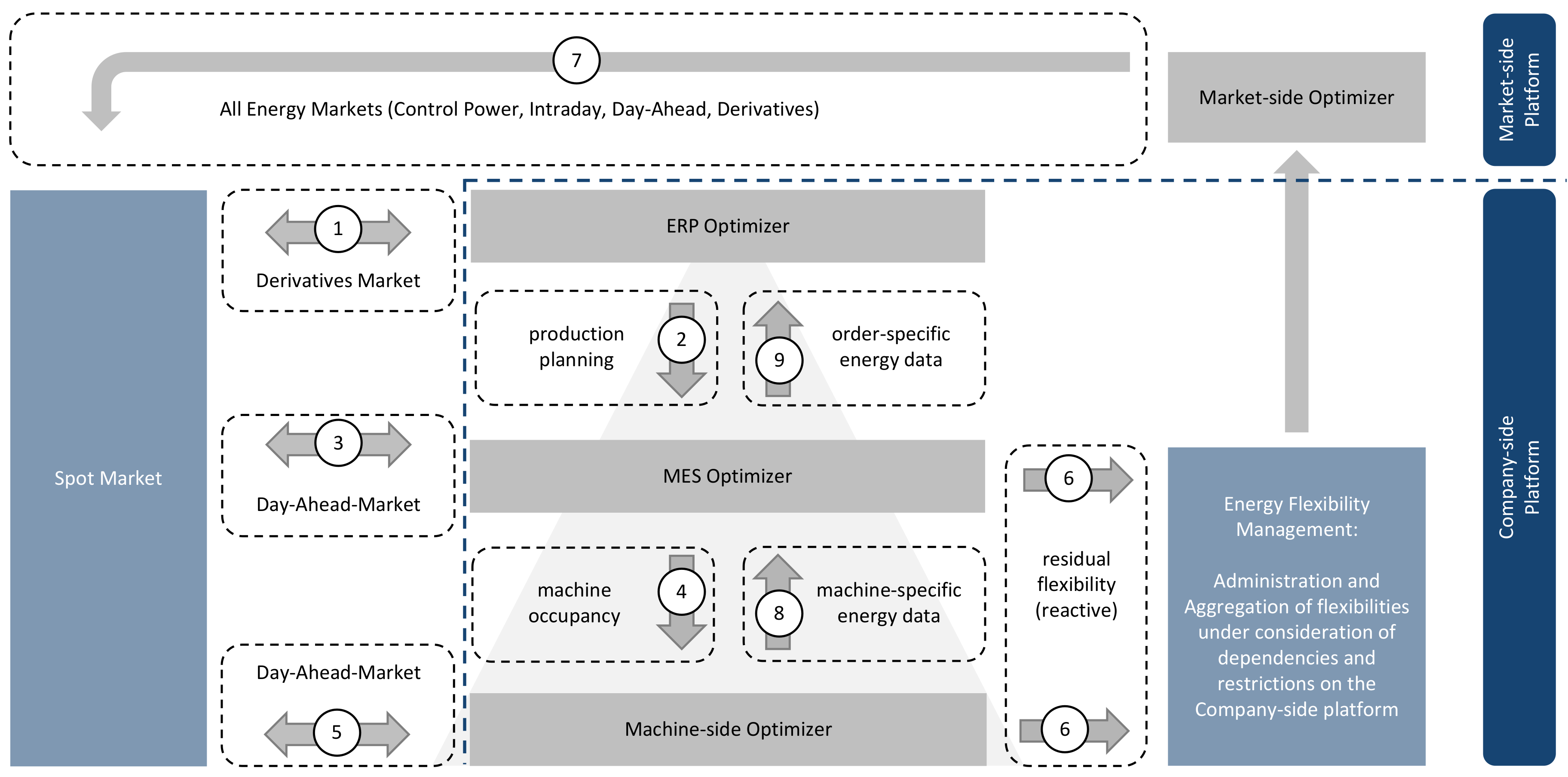

- Information flows: All bidirectional information flows between machines and energy markets, including every intermediate stage, must be covered to achieve an end-to-end approach. Bidirectionality because demand flexibility must be offered in the markets and, in addition, the purchase signals must subsequently be converted into load profiles within the company and ultimately into control signals for the machines and equipment. The information flows do not only cover company in-house processes as described by the automation pyramid [35,53]. Therefore, the concept of the automation pyramid needs to be broadened to include external processes with regard to marketing demand flexibility (see Nos. 1 and 2, Section 3). In addition, decentralized approaches also need to be considered as these concepts are increasingly common and provide more flexibility for companies (Section 2.5.1).

- Multi-level optimization: In order to regulate complex information flows and control the efficient use of flexibility, different levels of optimization are necessary. These levels decompose the overall optimization problem of efficient flexibility usage into sub-problems considering characteristics such as planning horizons, temporal resolutions, and maximum permissible runtimes. It is important that optimization levels can be implemented dynamically, e.g., depending on the target process and the company’s infrastructure, some of the optimization levels may be left out or split, e.g., into sub-optimizations. However, with decomposition, new challenges arise. First, restrictions made at certain levels must be respected by the following levels. Second, the·interaction between various optimization levels needs to be coordinated by a corresponding architecture (see No. 1, Section 3).

- Generic data model: To ensure consistency within the end-to-end approach for information flows and the interaction of different optimization levels, a generic data model covering a wide range of demand flexibility is necessary. However, not every communication between technical entities in the described end-to-end approach needs to be mapped in this data model. Rather, it is a matter of using the data model where it creates added value. Data models for further communication must then be designed in such a way that they can be derived from this generic data model or transferred back to it (see No. 2, Section 3).

- Traceability: While information flows and the data model ensure technical interoperability, the communication within the described end-to-end approach needs to be credible and trustworthy. Therefore, technical solutions meeting these specifications are necessary, e.g., step-by-step traceability of transactions. From a company-side perspective, this is to ensure that commercialized flexibility has really been implemented and the contract fulfilled accordingly. From a market-side point of view, the fulfillment of the contracts is equally important to ensure balanced groups in the energy system (see No. 5, Section 3).

- Encapsulation: Industry and the energy sector are completely different domains with diverse knowledge, methods, and technologies. To realize automated flexibility commercialization, both domains need to be connected and work interlocked. Consequently, approaches to encapsulate both domains without affecting the system’s performance are necessary. This includes, but is not limited to, commercializing load profiles without revealing manufacturing secrets and ensuring free competition on markets, etc. (see No. 4, Section 3).

4.2. Company-Side

- Vendor lock-in: Most existing manufacturing IT platforms are tailored to products and services offered by the respective vendor and lack interoperability with other platform providers or integration of external systems. To prevent vendor lock-in, open platforms with the ability to connect proprietary (e.g., Siemens S7, SAP BAPI, etc.) and open protocols (e.g., OPC-UA, REST, etc.) for hardware and software flexibly are required (see Nos. 2, 3 and 7, Section 3).

- Interoperability: To ensure interoperability, communication must be protocol independent, and the platform must be able to harmonize data models. For platforms to incorporate the described end-to-end approach, this does not only apply to internal interfaces and data models, but also to external communication. This allows, for example, the vendor-independent integration of PLC by Siemens and Bosch Rexroth with an EMS by econ solutions and an ERP by SAP. Additionally, it should be possible to establish a connection between platforms of different vendors. At the same time, since various stakeholders, vendors, components, and services are involved, the concepts for security and privacy become crucial. (see Nos. 2, 3, 4, and 6, Section 3).

- Energy as a decisive target: Existing platforms do not necessarily consider energy as a decisive target in manufacturing (see Section 2.5.1). Yet, with an increasingly volatile energy supply and the resulting need for greater demand flexibility, energy and its related availability and costs must be taken into account. Therefore, the functionalities of existing platforms need to be enhanced to consider energy aspects and to provide solutions for the synchronization of energy demand and supply (see No. 1, Section 3).

- Technical flexibility assessment: The variety of industry sectors yields a wide range of manufacturing processes with individual flexibility measure patterns. Besides the lack of adequate flexibility products on the energy markets, the technical assessment and integration into a flexibility portfolio within a complete flexibility management approach still requires high individual efforts, resulting in unpredictable project costs for companies. Even though aggregators and other service providers already offer audits to identify flexible loads for potential commercialization, the focus mainly lies on large-scale manufacturing plants, leaving unused potential (see No. 1, Section 3).

- Flexibility management: Due to the synchronization of energy demand and supply, the traditional magic triangle of time, cost, and quality becomes more and more volatile. Demand flexibility offers a possibility for cooperating with the rising importance of energy procurement. Therefore, platforms must enable an integrated management of demand flexibility within the company, integrating energy-related data with other manufacturing data for an adequate technical assessment. Consequently, the acquisition, aggregation, analysis, and optimization of process and manufacturing data are necessary to achieve energy-synchronized control of the systems, plants, and components (see No. 1, Section 3).

- Energy-synchronized control: Covering automated marketing of demand flexibility, functionality at all levels of the automation pyramid needs to be considered. Key features of this energy-synchronized control of manufacturing are the transformation of process data into flexibility measures and the aggregation by combining, splitting, and adapting the flexibility measures for optimized usage. In addition, a communication interface to the energy markets is required, which ideally is implemented using standardized and open protocols to automate the access to different offers of demand flexibility marketing, e.g., day-ahead-market, and information procurement, such as market price forecasts (see Nos. 1 and 2, Section 3).

- Entry hurdles: While the workload of administrators is reduced by the cloud offerings of certain manufacturing IT platforms, there are still significant entry hurdles for users. On the one hand, due to probable vendor lock-in and, on the other hand, due to the availability of functionalities in the field of manufacturing and the necessary effort for connection and usage. For these reasons, platforms should be designed as open development, sales, and operating platforms. Available functionalities can thus be obtained and operated via the platform, while missing functionalities can be developed by the user or software partners. (see Nos. 1, 2, 3, and 6, Section 3).

4.3. Market-Side

- Market design: The step towards trading flexibility from a market and regulatory perspective is subject to a number of obstacles. Three main obstacles to developing an efficient energy market embracing demand flexibility can be identified [76]:

- As the energy sector is subject to a complex regulatory system, a high uncertainty exists with regard to the continuity design of energy laws, subsidies, taxes, etc. This uncertainty is currently reflected by the indecision on the part of companies to invest.

- Energy market design aims to treat different technologies equally. However, in reality, the nature of flexibility measures (as described in Section 2), dependent on the type of machine or manufacturing process, does not imitate conventional generation schemes. The result is a distortion of flexibility options and technologies.

- The complexity of the energy sector is also reflected in the price structure. Daily price fluctuations on the electricity market are only partially visible to consumers. The high fixed cost share (electricity taxes, network charges, etc.) is leveled, the price fluctuations are reduced, and the profit margin of the demand flexibility project is reduced.

Further research is needed to highlight the inefficiencies and weaknesses of the current market design and to identify solutions for obtaining economically-viable demand flexibility options (see No. 6, Section 3). - Economic flexibility assessment: Participation in the energy market is attractive when the value of the flexibility measure, i.e., the electricity cost savings that can potentially be achieved through load shifting, is higher than the opportunity costs that the company incurs by making the process more flexible and possibly losing value due to the flexibility measure. If the value of flexibility signaled on the market is below the opportunity cost, a flexibility measure will not be stimulated. Therefore, the internal financial assessment of the flexibility needs to have both information on the manufacturing costs (including all implied potential costs if used) and real-time market prices. The information on the optimization combines the two prices and indicates which flexibilities should be drawn from an economic point of view. Regardless of whether the optimization takes place on the company-side or market-side platform, some kind of data model for communication of flexibilities is used. To ensure consistency in communication while maintaining a high level of functionality and traceability, a standardized description and modeling of industrial demand flexibility is required. (see Nos. 1, 2, and 5, Section 3).

- Energy market forecast: To ensure planning security, the role of forecasting energy market prices is crucial. However, a predictability of more than five days, e.g., the day-ahead-market, due to the intermittent nature of renewable energy sources, is difficult. In some company cases, predictions of more than five days, regardless of the forecast quality, are needed. Currently, plenty of forecast service providers are competing for the growing market of demand flexibility. The forecasting service market is not yet transparent, and therefore, it is not easy to compare different services. This might be suitable for individual service providers; however, it does not contribute to a performance-based free market embracing free competition (see No. 3, Section 3).

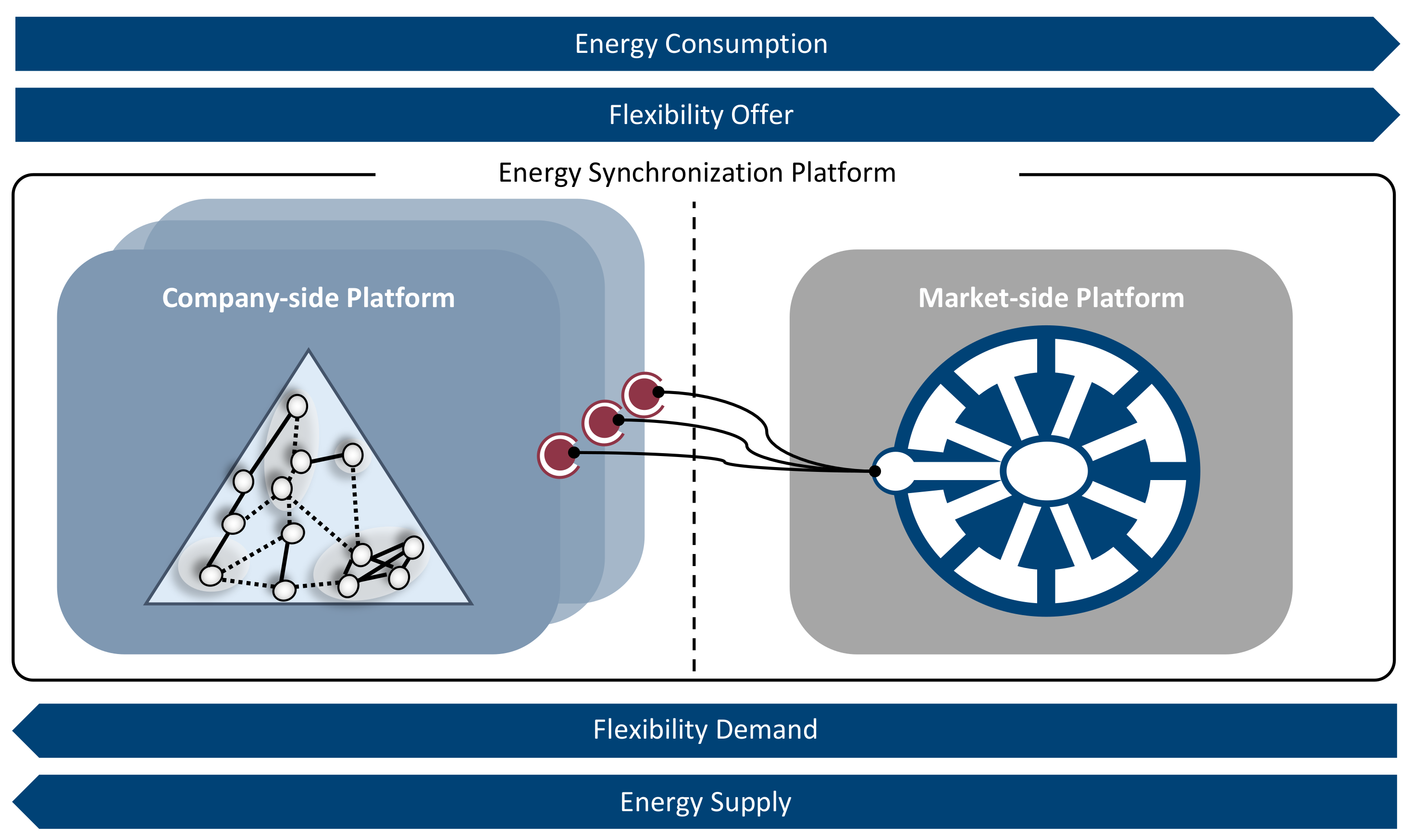

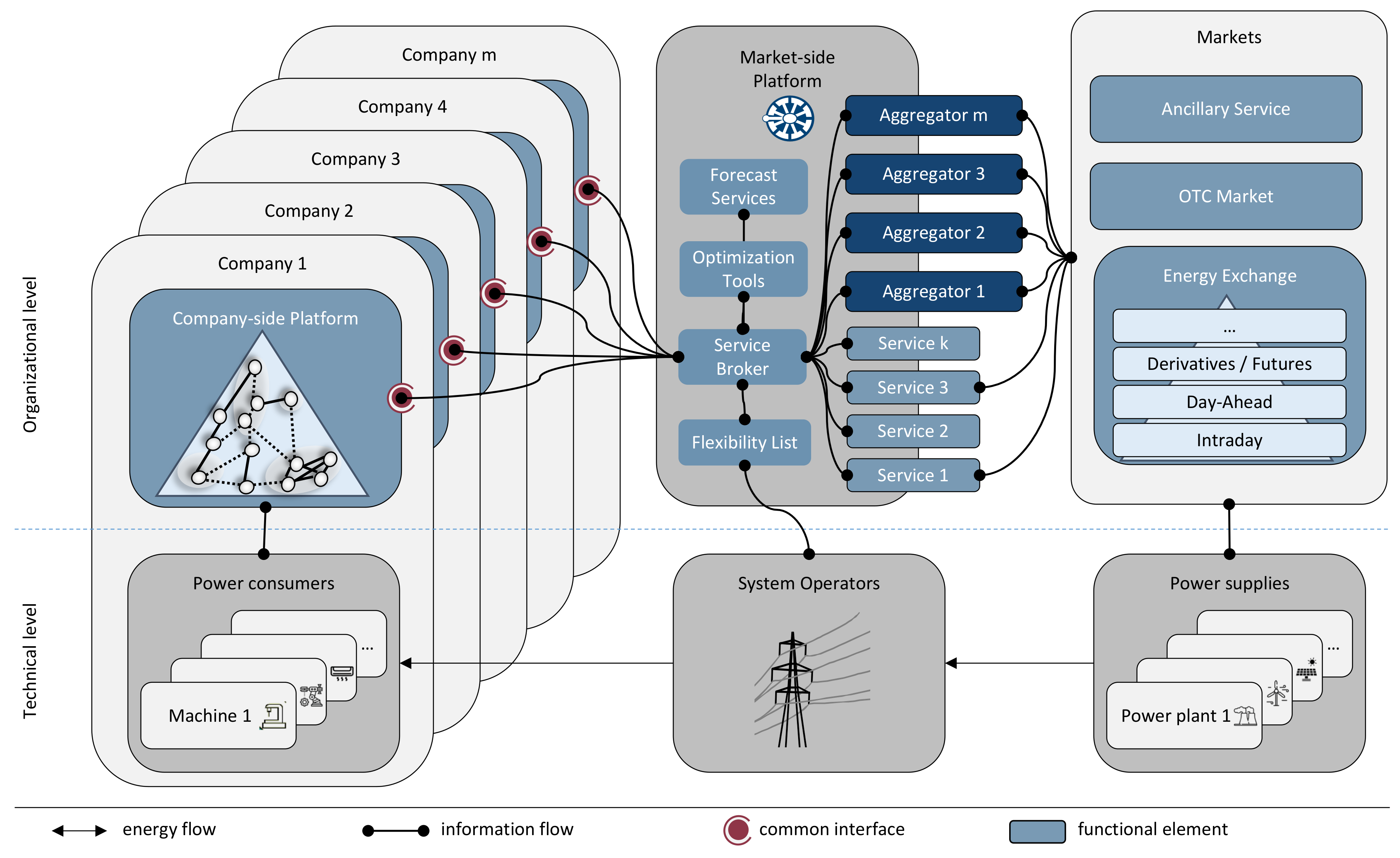

5. Concept of the Energy Synchronization Platform

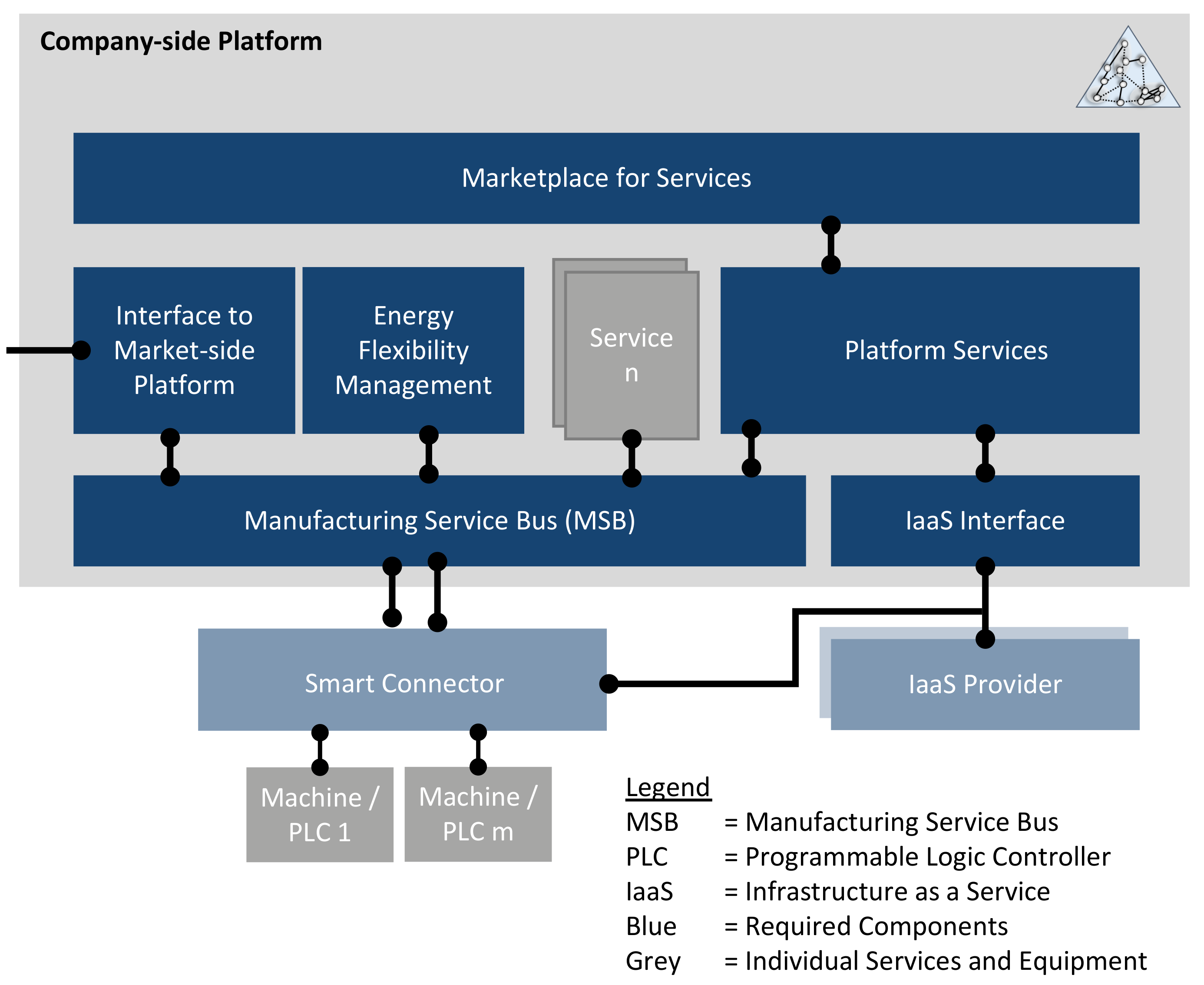

5.1. Company-Side Platform

- Marketplace for services: The marketplace for services is comparable to the well-known concept of app stores and represents the web-based point of entry for users. It enables obtaining new services and deploying them automatically in conjunction with the platform services. Due to the simple booking of services on demand, entry hurdles for new participants are reduced. Offering a wide range of services from different independent services vendors, the marketplace ensures free competition.

- Services: In contrast to existing approaches, which do not consider energy as a decisive target for manufacturing [79,80], additional services on the CoP, such as manufacturing planning and control or various optimization services, are designed taking it into account. A typical approach with respect to logistic operating curves in manufacturing planning and control was described in [81]. Since these additional services are highly individual and vary greatly between use cases, they are flexibly orchestrated using the MSB and integrated into the handling of demand flexibility by the energy flexibility management. As complementors can flexibly contribute their services, the ecosystem is able to profit from co-evolution. In addition, the central role of the complementors prevents from winner-takes-all situations (see Section 2.5).

- Platform services: The operational functions of the CoP are summarized in platform services. Among them are identity and permission management, service repository, service life cycle management, as well as service accounting and service monitoring. Platform services are well described in the literature, e.g., in [62,82].

- Interface to the market-side platform: The interface to the market-side platform enables services on the CoP to access data and services on the MaP via a single standardized interface. Services on the CoP benefit from this by only having to implement a single interface instead of multiple interfaces to all requested services on the MaP. Furthermore, this represents a security barrier between companies and energy markets.

- Energy flexibility management: The CoP’s hub for aggregating and managing all demand flexibilities and their dependencies is represented by the energy flexibility management. First, it includes an overview of the company’s flexibility. Second, it supports the technical assessment of flexibility. Third, the energy flexibility management provides an API to combine, split, and adapt flexibility for optimized usage. However, the optimization is not part of the energy flexibility management and is provided by third party services instead. Furthermore, the energy flexibility management is responsible for controlling the implementation of demand flexibility measures and communication with energy markets. Most likely, the functionality of the energy flexibility management will be integrated or at least closely connected to a company’s EMS.

- Manufacturing service bus: An integration layer for manufacturing companies needs to ease reconfiguration, enable a loose coupling, allow for asynchronous communication, and offer standards-based integration [83]. The MSB meets these requirements, as well as additional ones as described in [84]. It provides an abstraction layer for different protocols, which can easily be extended by additional interfaces. The purpose of this abstraction layer is to harmonize data models by allowing individual data objects to be mapped flexibly to each other. This mapping can either be modeled automatically via a self-description or manually. Furthermore, the easy extensibility enables effortless additions of protocols, which can either be proprietary or open. Consequently, the MSB can also be used to translate proprietary protocols (e.g., Siemens S7) to open protocols (e.g., OPC-UA). Summarizing, the MSB ensures interoperability between all components of the CoP in the sense of a close cooperation of independent, heterogeneous systems in order to exchange information efficiently and in a usable manner.

- Smart connector: The smart connector is designed as a bidirectional interface to access machines and their respective PLCs from higher-level IT systems. Therefore, it extends the MSB by translating proprietary PLC protocols to open IT protocols and allows for process data and machine data acquisition. Additionally, the smart connector’s machine interface is designed to process energy data and to transfer it to the generic EFDM to model demand flexibility. Moreover, orchestrated by services on the CoP, the smart connector is also capable of an energy-synchronized control of the process, e.g., triggered by price signals.

- IaaS interface: The IaaS interface represents an abstraction layer between the CoP and its underlying infrastructure. It enables the CoP to distribute the deployment of services, ranging from in-house infrastructure to external cloud infrastructure such as Amazon Web Services and edge devices such as the smart connector.

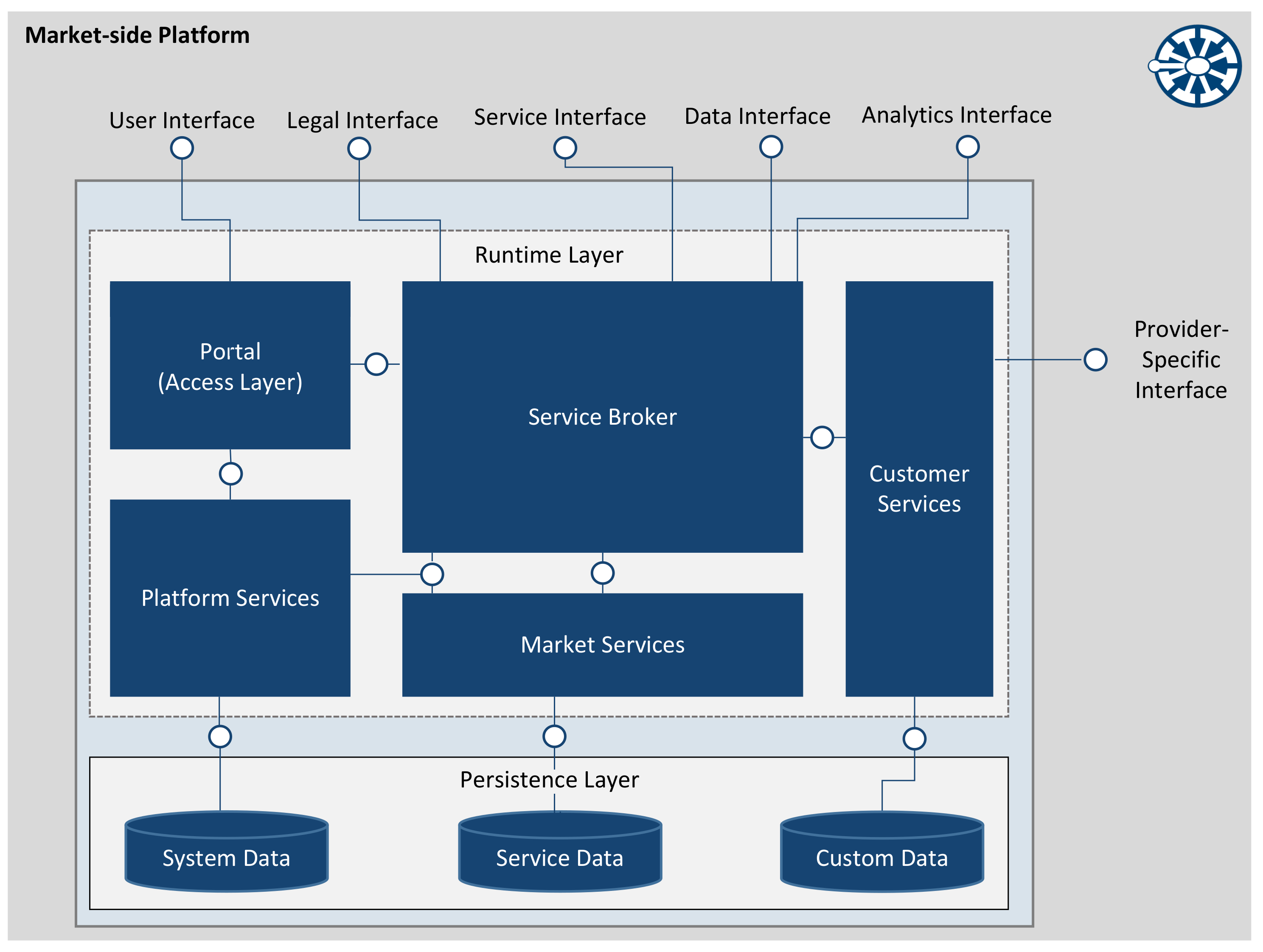

5.2. Market-Side Platform

- Runtime layer: This represents the active component of the MaP, which has the necessary interfaces to the outside. On the one hand, the runtime layer is the basis for system-related and domain-specific services; on the other hand, it also implements the routing to the corresponding services and data.

- Persistence layer: The persistence layer acts as a scalable data management component and allows writing and reading access from the runtime layer. It represents the passive “database” component of the MaP.

- Portal (access layer): The portal represents the component, which allows users to communicate with the platform through a graphical user interface. Besides basic features, such as registration and login, it provides an input mask for information transfer to other components, API documentation, the possibility to execute test calls, community functionalities (e.g., rating), and the monitoring of offered services. It is connected to the platform services for access management and authentication, as well as the service broker for further access to functionalities.

- Service broker: The service broker acts as a central access point for market participants implementing the API gateway, makes inquiries to registries, and forwards the request of the current market participant according to the response from the registries. The core task of the service broker is to establish contact between flexibility providers and their users by integrating supporting services. As the core of the multi-sided architecture, it is also exposed to threats and requires threat protection against cyber attacks, such as distributed denial of service attacks, SQL injections, etc. Moreover, it is the logical instance that regulates access control policies and enforces policies related to subscriber authentication and authorization of access to services. Thus, the service broker uses services of operational components from platform services.

- Platform services: The operational functions of the MaP are summarized in platform services. They inherit control and contract services, in order to monitor and maintain the platform, but also oversee the access management, which regulates access to sensitive data according to the respective authorization. In order to monitor the access authorizations, the platform services access the system data containing the log, user, and contract data, market services, the service broker, and the access layer.

- Market services: These are the services offered on the MaP by third parties and allow service providers and platform users to analyze what features have been used and what registered users are looking for. It is important to note that market services are only addressed from the service broker. The connection to platform services is for authentication reasons only. Market service-related data are stored within the component service data. This comprises among others the storage of flexibility data in the form of a filterable list, e.g., in the form “market participant X has offered flexibility Y of quantity Z [for time interval T]”.

- Customer services: In order to provide an interface to the external services or datasets offered by market participants, but not directly published on the market platform, the customer services complement the service broker by a collection of virtual services that bijectively map to these external services. In this way, the service broker can address the virtual services and datasets and thus communicate with the external ones. It has a connection to custom data and a database to store the required information.

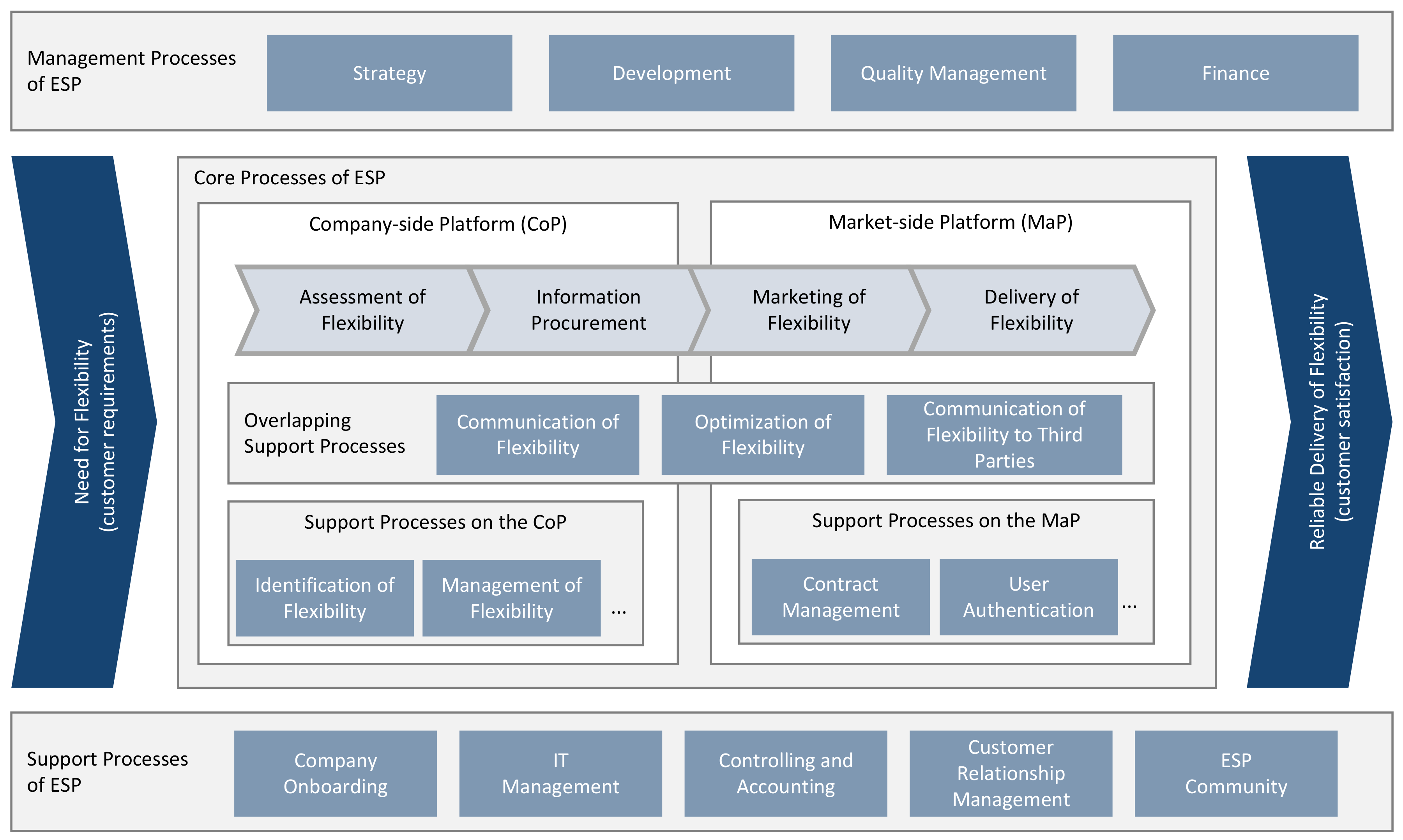

5.3. Synthesis to an End-to-End Approach

6. Summary

7. Outlook and Remaining Deficit

- Governance: The concept of governance for the invented platform ecosystem is one of the most significant remaining deficits. The governance approach should be mainly based on two elements, introducing standards and a community. To enable external access and contributions, a strict standardization of all processes, services, interfaces, data models, and communication flows is necessary. The BPMN documentation presents a first step. Nevertheless, this needs to be further developed by standardizing a reference architecture. In addition, the ecosystem requires a platform carrier to coordinate future extensions, maintenance, regulation, and safeguard ongoing operations. Since the literature indicates self-selection as the most effective approach for platform ecosystems, a central task is to build a broad community, where all participants and complementors of the platform can participate.

- Additional services: The implementation and marketing of energy flexibility in manufacturing companies are complex. Therefore, the existing services on CoP and MaP are not yet all-encompassing and cannot fulfill all requirements in every use case. Consequently, some further extensions and additional services need to be implemented, e.g., for advanced price and signal predictions, aggregation of flexibility measures, hierarchical optimization at the different operational levels, evaluation costs for energy flexibility at the manufacturing level, risk assessment of flexibility measures, etc.

- Information procurement: While the existing energy flexibility management based on the EFDM is very well suited to the applications of assessing and marketing flexibility, there is a gap with respect to information procurement, e.g., market price predictions. Therefore, an approach for flexibly connecting services on the CoP with MaP has to be developed. The challenge is to make it possible to use more than a single data model such as the one described for flexibility measures, but rather a wide range of data models must be translated without affecting the operation of the existing components.

- Security: Security by design has been the main way of integrating security aspects so far. In future research, a detailed security analysis needs to be conducted in which feared events are identified and relevant counter measures derived. In addition, standardized security requirements for any kind of interface and service need to be defined. Thus, security aspects were mainly incorporated for the encapsulation of companies and energy markets. A serious threat, however, is the deliberate disruption of the energy system through manipulation of the energy markets via the ESP. As part of a critical infrastructure [75], this aspect must, therefore, also be taken into account when extending the security concept.

- Credibility and trustworthiness: The elaborated architecture and information flow guarantee high standards of credibility and trustworthiness. However, in the recent past, there has been an increase of new distributed ledger-based technologies (e.g., block chain), which show promising results in this field. Their application should be examined and implemented to further enhance the capability of the solution.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| API | Application Programming Interface |

| BPMN | Business Process Model and Notation |

| CoP | Company-side Platform |

| DR | Demand-Side Response |

| DSM | Demand-Side Management |

| EFDM | Energy Flexibility Data Model |

| EMS | Energy Management Systems |

| ERP | Enterprise Resource Planning |

| ESP | Energy Synchronization Platform |

| IaaS | Infrastructure as a Service |

| IT | Information Technology |

| MaP | Market-side Platform |

| MES | Manufacturing Execution System |

| MSB | Manufacturing Service Bus |

| OPC-UA | Open Platform Communications Unified Architecture |

| OpenADR | Open Automated Demand Response |

| OTC | Over The Counter |

| PLC | Programmable Logic Controllers |

| REST | Representational State Transfer |

| USEF | Universal Smart Energy Framework |

| XaaS | Everything as a Service |

References

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: New York, NY, USA, 2015. [Google Scholar]

- Mann, M.E.; Rahmstorf, S.; Kornhuber, K.; Steinman, B.A.; Miller, S.K.; Coumou, D. Influence of Anthropogenic Climate Change on Planetary Wave Resonance and Extreme Weather Events. Sci. Rep. 2017, 7, 1–10. [Google Scholar] [CrossRef] [PubMed]

- Channel, J.; Churmi, E.; Ngyen, P.; Prior, E.; Syme, A.; Jansen, H.; Rahbari, E.; Morse, E.; Kleinman, S.; Kruger, T. Energy Darwinism II: Why a Low Carbon Future Doesn’t Have to Cost the Earth; Citi GPS: London, UK, 2015. [Google Scholar]

- International Energy Agency. Key World Energy Statistics 2018; International Energy Agency: Paris, France, 2018. [Google Scholar]

- Bertram, R.; Primova, T.; Herbert, J.; Bulantova, K.; Metaxa, K.; Ugryn, K.; Walsh, M. Energy Atlas: Facts and Figures About Renewables in Europe 2018; Heinrich Böll Foundation: Berlin, Germany, 2018. [Google Scholar]

- Federal Ministry for Economic Affairs and Energy. Energiekonzept für Eine Umweltschonende, Zuverlässige und Bezahlbare Energieversorgung; BMWi: Berlin, Germany, 2010. [Google Scholar]

- Umweltbundesamt. Erneuerbare Energien in Deutschland: Daten zur Entwicklung im Jahr 2018; Umweltbundesamt: Dessau-Roßlau, Germany, 2019. [Google Scholar]

- Bundesnetzagentur für Elektrizität, Gas, Telekommunikation, Post und Eisenbahnen. Quartalsbericht zu Netz-und Systemsicherheitsmaßnahmen: Gesamtjahr und Viertes Quartal 2018; Bundesnetzagentur für Elektrizität, Gas, Telekommunikation, Post und Eisenbahnen: Bonn, Germany, 2019. [Google Scholar]

- European Environmental Agency. Final Energy Consumption by Sector and Fuel; European Environmental Agency: Kopenhagen, Denmark, 2018. [Google Scholar]

- Papaefthymiou, G.; Haesen, E.; Sach, T. Power System Flexibility Tracker: Indicators to track flexibility progress towards high-RES systems. Renew. Energy 2018, 127, 1026–1035. [Google Scholar] [CrossRef]

- Lund, P.D.; Lindgren, J.; Mikkola, J.; Salpakari, J. Review of energy system flexibility measures to enable high levels of variable renewable electricity. Renew. Sustain. Energy Rev. 2015, 45, 785–807. [Google Scholar] [CrossRef] [Green Version]

- Müller, T.; Möst, D. Demand Response Potential: Available when Needed? Energy Policy 2018, 115, 181–198. [Google Scholar] [CrossRef]

- Lacal Arantegui, R.; Jäger-Waldau, A. Photovoltaics and wind status in the European Union after the Paris Agreement. Renew. Sustain. Energy Rev. 2018, 81, 2460–2471. [Google Scholar] [CrossRef]

- Battaglini, A.; Komendantova, N.; Brtnik, P.; Patt, A. Perception of barriers for expansion of electricity grids in the European Union. Energy Policy 2012, 47, 254–259. [Google Scholar] [CrossRef]

- Lund, H.; Østergaard, P.A.; Connolly, D.; Ridjan, I.; Mathiesen, B.V.; Hvelplund, F.; Thellufsen, J.Z.; Sorknæs, P. Energy Storage and Smart Energy Systems. Int. J. Sustain. Energy Plan. Manag. 2016, 11, 3–14. [Google Scholar] [CrossRef]

- Palensky, P.; Dietrich, D. Demand Side Management: Demand Response, Intelligent Energy Systems, and Smart Loads. IEEE Trans. Ind. Inf. 2011, 7, 381–388. [Google Scholar] [CrossRef]

- Feuerriegel, S.; Neumann, D. Measuring the financial impact of demand response for electricity retailers. Energy Policy 2014, 65, 359–368. [Google Scholar] [CrossRef] [Green Version]

- Albadi, M.H.; El-Saadany, E.F. A summary of demand response in electricity markets. Electr. Power Syst. Res. 2008, 78, 1989–1996. [Google Scholar] [CrossRef]

- Markle-Huss, J.; Feuerriegel, S.; Neumann, D. Decision model for sustainable electricity procurement using nationwide demand response. In Proceedings of the 49th Annual Hawaii International Conference on System Sciences, Koloa, HI, USA, 5–8 January 2016; pp. 1010–1019. [Google Scholar] [CrossRef]

- Jazayeri, P.; Schellenberg, A.; Rosehart, W.D.; Doudna, J.; Widergren, S.; Lawrence, D.; Mickey, J.; Jones, S. A Survey of Load Control Programs for Price and System Stability. IEEE Trans. Power Syst. 2005, 20, 1504–1509. [Google Scholar] [CrossRef]

- Steurer, M. Analyse von Demand Side Integration im Hinblick auf eine Effiziente und Umweltfreundliche Energieversorgung. Ph.D. Thesis, University of Stuttgart, Stuttgart, Germany, 2017. [Google Scholar] [CrossRef]

- Bertsch, J.; Fridgen, G.; Sachs, T.; Schöpf, M.; Schweter, H.; Sitzmann, A. Ausgangsbedingungen für die Vermarktung von Nachfrageflexibilität: Status-Quo-Analyse und Metastudie; Bayreuther Arbeitspapiere zur Wirtschaftsinformatik; University of Bayreuth: Bayreuth, Germany, 2017; Volume 62. [Google Scholar]

- Lübbecke, M.; Koster, A.M.; Letmathe, P.; Madlener, R.; Peis, B.; Walther, G. Operations Research Proceedings 2014: Selected Papers of the Annual International Conference of the German Operations Research Society (GOR), RWTH Aachen University, Germany, 2–5 September 2014; Springer: Cham, Switzerland, 2016. [Google Scholar]

- Maier, F.; Belhassan, H.; Klempp, N.; Koetter, F.; Siehler, E.; Stetter, D.; Wohlfrom, A. Decision Support for Structured Energy Procurement. In Proceedings of the 6th International Conference on Smart Cities and Green ICT Systems-Volume 1, Porto, Portugal, 22–24 April 2017; pp. 77–86. [Google Scholar] [CrossRef]

- Rackow, T.; Kohl, J.; Canzaniello, A.; Schuderer, P.; Franke, J. Energy Flexible Production: Saving Electricity Expenditures by Adjusting the Production Plan. Procedia CIRP 2015, 26, 235–240. [Google Scholar] [CrossRef] [Green Version]

- Zafirakis, D.; Chalvatzis, K.J.; Baiocchi, G.; Daskalakis, G. The value of arbitrage for energy storage: Evidence from European electricity markets. Appl. Energy 2016, 184, 971–986. [Google Scholar] [CrossRef]

- Fridgen, G.; Häfner, L.; König, C.; Sachs, T. Providing Utility to Utilities: The Value of Information Systems Enabled Flexibility in Electricity Consumption. J. Assoc. Inf. Syst. 2016, 17, 537–563. [Google Scholar] [CrossRef]

- Fridgen, G.; Keller, R.; Thimmel, M.; Wederhake, L. Shifting load through space—The economics of spatial demand side management using distributed data centers. Energy Policy 2017, 109, 400–413. [Google Scholar] [CrossRef]

- Koliou, E.; Eid, C.; Chaves-Ávila, J.P.; Hakvoort, R.A. Demand response in liberalized electricity markets: Analysis of aggregated load participation in the German balancing mechanism. Energy 2014, 71, 245–254. [Google Scholar] [CrossRef]

- Dranka, G.G.; Ferreira, P. Review and assessment of the different categories of demand response potentials. Energy 2019, 179, 280–294. [Google Scholar] [CrossRef]

- Strbac, G. Demand side management: Benefits and challenges. Energy Policy 2008, 36, 4419–4426. [Google Scholar] [CrossRef]

- Meeus, L.; Hancher, L.; Azevedo, I.; He, X.; Keyaerts, N.; Glachant, J.M. Shift, Not Drift: Towards Active Demand Response and Beyond (Topic 11); Publications Office: Luxembourg, 2013. [Google Scholar]

- Graßl, M.; Reinhart, G. Evaluating Measures for Adapting the Energy Demand of a Production System to Volatile Energy Prices. Procedia CIRP 2014, 15, 129–134. [Google Scholar] [CrossRef]

- Roesch, M.; Berger, C.; Braunreuther, S.; Reinhart, G. Cost-model for Energy-oriented Production Control. In Proceedings of the 2018 IEEE International Conference on Industrial Engineering and Engineering Management (IEEM), Bangkok, Thailand, 16–19 December 2018; pp. 158–162. [Google Scholar] [CrossRef]

- VDI. VDI 5600-1: Manufacturing Execution Systems (MES); Beuth Verlag: Berlin, Germany, 2016. [Google Scholar]

- Sauter, T.; Soucek, S.; Kastner, W.; Dietrich, D. The Evolution of Factory and Building Automation. IEEE Ind. Electron. Mag. 2011, 5, 35–48. [Google Scholar] [CrossRef]

- Thomas, L.D.W.; Autio, E.; Gann, D.M. Architectural Leverage: Putting Platforms in Context. Acad. Manag. Perspect. 2014, 28, 198–219. [Google Scholar] [CrossRef]

- Gawer, A. Bridging differing perspectives on technological platforms: Toward an integrative framework. Res. Policy 2014, 43, 1239–1249. [Google Scholar] [CrossRef] [Green Version]

- Tilson, D.; Sorensen, C.; Lyytinen, K. Change and Control Paradoxes in Mobile Infrastructure Innovation: The Android and iOS Mobile Operating Systems Cases. In Proceedings of the 2012 45th Hawaii International Conference on System Science, Maui, HI, USA, 4–7 January 2012; pp. 1324–1333. [Google Scholar] [CrossRef]

- Parker, G.; Van Alstyne, M.; Jiang, X. Platform Ecosystems: How Developers Invert the Firm. MIS Q. 2017, 41, 255–266. [Google Scholar] [CrossRef]

- Tiwana, A.; Konsynski, B.; Bush, A.A. Research Commentary—Platform Evolution: Coevolution of Platform Architecture, Governance, and Environmental Dynamics. Inf. Syst. Res. 2010, 21, 675–687. [Google Scholar] [CrossRef]

- Keller, R. Cloud Networks as Platform-Based Ecosystems: Detecting Management Implications for Actors in Cloud Networks. Ph.D. Thesis, University of Bayreuth, Bayreuth, Germany, 2019. [Google Scholar] [CrossRef]

- De Reuver, M.; Sørensen, C.; Basole, R.C. The Digital Platform: A Research Agenda. J. Inf. Technol. 2018, 33, 124–135. [Google Scholar] [CrossRef] [Green Version]

- Ozalp, H.; Cennamo, C.; Gawer, A. Disruption in Platform–Based Ecosystems. J. Manag. Stud. 2018, 55, 1203–1241. [Google Scholar] [CrossRef]

- Inoue, Y.; Tsujimoto, M. New market development of platform ecosystems: A case study of the Nintendo Wii. Technol. Forecast. Soc. Chang. 2018, 136, 235–253. [Google Scholar] [CrossRef]

- Forbes. The World’s Most Valuable Brands; Forbes Media: New York, NY, USA, 2018. [Google Scholar]

- Eisenmann, T.R. Winner-Takes-All in Networked Markets; Harvard Business School: Boston, MA, USA, 2007; pp. 806–831. [Google Scholar]

- Inoue, Y. Winner-Takes-All or Co-Evolution among Platform Ecosystems: A Look at the Competitive and Symbiotic Actions of Complementors. Sustainability 2019, 11, 726. [Google Scholar] [CrossRef]

- Clements, M.T.; Ohashi, H. Indirect Network Effects and the Product Cycle: Video Games in the U.S., 1994–2002. J. Ind. Econ. 2005, 53, 515–542. [Google Scholar] [CrossRef]

- Ceccagnoli, M.; Forman, C.; Huang, P.; Wu, D.J. Cocreation of Value in a Platform Ecosystem! The Case of Enterprise Software. MIS Q. 2012, 36, 263. [Google Scholar] [CrossRef]

- Wareham, J.D.; Fox, P.B.; Cano Giner, J.L. Technology Ecosystem Governance. Org. Sci. 2014, 25, 1195–1215. [Google Scholar] [CrossRef]

- Huber, T.L.; Kude, T.; Dibbern, J. Governance Practices in Platform Ecosystems: Navigating Tensions Between Cocreated Value and Governance Costs. Inf. Syst. Res. 2017, 28, 563–584. [Google Scholar] [CrossRef]

- IEC. IEC 62264-1: Enterprise-Control System Integration-Part 1: Models and Terminology; IEC: Geneva, Switzerland, 2013. [Google Scholar]

- Acatech. Cyber-Physical Systems: Driving Force for Innovation in Mobility, Health, Energy and Production; Acatech-National Academy of Scvience and Engineering: Berlin, Germany, 2011. [Google Scholar]

- Körner, M.F.; Bauer, D.; Keller, R.; Rösch, M.; Schlereth, A.; Simon, P.; Bauernhansl, T.; Fridgen, G.; Reinhart, G. Extending the Automation Pyramid for Industrial Demand Response. Procedia CIRP 2019, 81, 998–1003. [Google Scholar] [CrossRef]

- Seitz, P.; Abele, E.; Bank, L.; Bauernhansl, T.; Colangelo, E.; Fridgen, G.; Schilp, J.; Schott, P.; Sedlmeir, J.; Strobel, N.; et al. IT-based Architecture for Power Market Oriented Optimization at Multiple Levels in Production Processes. Procedia CIRP 2019, 81, 618–623. [Google Scholar] [CrossRef]

- Monostori, L.; Kádár, B.; Bauernhansl, T.; Kondoh, S.; Kumara, S.; Reinhart, G.; Sauer, O.; Schuh, G.; Sihn, W.; Ueda, K. Cyber-physical systems in manufacturing. CIRP Ann. 2016, 65, 621–641. [Google Scholar] [CrossRef]

- Zezulka, F.; Marcon, P.; Vesely, I.; Sajdl, O. Industry 4.0–An Introduction in the phenomenon. IFAC-PapersOnLine 2016, 49, 8–12. [Google Scholar] [CrossRef]

- Tsujimoto, M.; Kajikawa, Y.; Tomita, J.; Matsumoto, Y. A review of the ecosystem concept—Towards coherent ecosystem design. Technol. Forecast. Soc. Change 2018, 136, 49–58. [Google Scholar] [CrossRef]

- Duan, Y.; Fu, G.; Zhou, N.; Sun, X.; Narendra, N.C.; Hu, B. Everything as a Service (XaaS) on the Cloud: Origins, Current and Future Trends. In Proceedings of the 2015 IEEE 8th International Conference on Cloud Computing, New York, NY, USA, 27 June–2 July 2015; pp. 621–628. [Google Scholar] [CrossRef]

- Ren, L.; Zhang, L.; Tao, F.; Zhao, C.; Chai, X.; Zhao, X. Cloud manufacturing: From concept to practice. Enterp. Inf. Syst. 2015, 9, 186–209. [Google Scholar] [CrossRef]

- Stock, D.; Stöhr, M.; Rauschecker, U.; Bauernhansl, T. Cloud-based Platform to Facilitate Access to Manufacturing IT. Procedia CIRP 2014, 25, 320–328. [Google Scholar] [CrossRef]

- Holtewert, P.; Wutzke, R.; Seidelmann, J.; Bauernhansl, T. Virtual Fort Knox Federative, Secure and Cloud-based Platform for Manufacturing. Procedia CIRP 2013, 7, 527–532. [Google Scholar] [CrossRef]

- Huang, B.; Li, C.; Yin, C.; Zhao, X. Cloud manufacturing service platform for small- and medium-sized enterprises. Int. J. Adv. Manuf. Technol. 2013, 65, 1261–1272. [Google Scholar] [CrossRef]

- Bauer, D.; Stock, D.; Bauernhansl, T. Movement Towards Service-orientation and App-orientation in Manufacturing IT. Procedia CIRP 2017, 62, 199–204. [Google Scholar] [CrossRef]

- Schott, P.; Ahrens, R.; Bauer, D.; Hering, F.; Keller, R.; Pullmann, J.; Schel, D.; Schimmelpfennig, J.; Simon, P.; Weber, T.; et al. Flexible IT platform for synchronizing energy demands with volatile markets. IT-Inf. Technol. 2018, 60, 155–164. [Google Scholar] [CrossRef]

- Hülsbömer, S.; Rozsa, A.; Schonschek, O.; Thomas-Ißbrücker, T. Studie Cloud Security 2019; IDG Business Media GmbH: München, Germany, 2019. [Google Scholar]

- Keller, R.; König, C. A Reference Model to Support Risk Identification in Cloud Networks. In Proceedings of the International Conference on Information Systems (ICIS 2014): Building a Better World through Information Systems, Auckland, New Zealand, 14–17 December 2014. [Google Scholar]

- Federal Office for Economic Affairs and Export Control. Der Markt für Energiemanagement-Systeme in Kleinen und Mittleren Unternehmen; Federal Office for Economic Affairs and Export Control: Eschborn, Germany, 2017. [Google Scholar]

- Kahlenborn, W.; Kabisch, S.; Klein, J.; Richter, I.; Schürmann, S. Energy Management Systems in Practice: ISO 50001: A Guide for Companies and Organisations; BMU: Berlin, Germany, 2012. [Google Scholar]

- Sauer, A.; Weckmann, S.; Zimmermann, F. Softwarelösungen für das Energiemanagement von Morgen: Eine Vergleichende Studie; University of Stuttgart: Stuttgart, Germany, 2016. [Google Scholar]

- Fontana, M.E.; Aragão, J.P.S.; Morais, D.C. Decision support system for outsourcing strategies. Prod. Eng. 2019, 22, 832. [Google Scholar] [CrossRef]

- Siano, P. Demand response and smart grids—A survey. Renew. Sustain. Energy Rev. 2014, 30, 461–478. [Google Scholar] [CrossRef]

- Seifermann, S.; Abele, E.; Bauernhansl, T.; Brecher, C.; Franke, J.; Herrmann, C.; Putz, M.; Reinhart, G.; Thiede, S.; Zaeh, M. Energy Flexibility in Manufacturing: The Kopernikus-Project SynErgie. In Proceedings of the CIRP 2017 General Assembly, STC-A Meeting, Lugano, Switzerland, 20–26 August 2017. [Google Scholar]

- Federal Ministry of the Interior. Cyber Security Strategy for Germany; Federal Ministry of the Interior: Berlin, Germany, 2011. [Google Scholar]

- Ländner, E.M.; Märtz, A.; Schöpf, M.; Weibelzahl, M. From energy legislation to investment determination: Shaping future electricity markets with different flexibility options. Energy Policy 2019, 129, 1100–1110. [Google Scholar] [CrossRef]

- Gilder, G. Metcalf’s Law and Legacy. Forb. ASAP 1993, 152, 158–166. [Google Scholar]

- Schott, P.; Sedlmeir, J.; Strobel, N.; Weber, T.; Fridgen, G.; Abele, E. A Generic Data Model for Describing Flexibility in Power Markets. Energies 2019, 12, 1893. [Google Scholar] [CrossRef]

- Neugebauer, R.; Putz, M.; Schlegel, A.; Langer, T.; Franz, E.; Lorenz, S. Energy-Sensitive Production Control in Mixed Model Manufacturing Processes. In Leveraging Technology for a Sustainable World; Dornfeld, D.A., Linke, B.S., Eds.; Springer: Berlin/Heidelberg, Germany, 2012; pp. 399–404. [Google Scholar]

- Reinhart, G.; Geiger, F.; Karl, F.; Wiedemann, M. Handlungsfelder zur Realisierung energieeffizienter Produktionsplanung und -steuerung. ZWF Z. für Wirtsch. Fabr. 2011, 106, 596–600. [Google Scholar] [CrossRef]

- Pfeilsticker, L.; Colangelo, E.; Sauer, A. Energy Flexibility—A new Target Dimension in Manufacturing System Design and Operation. Procedia Manuf. 2019, 33, 51–58. [Google Scholar] [CrossRef]

- Schel, D.; Bauer, D.; Vazquez, F.G.; Schulz, F.; Bauernhansl, T. IT Platform for Energy Demand Synchronization Among Manufacturing Companies. Procedia CIRP 2018, 72, 826–831. [Google Scholar] [CrossRef]

- Mínguez, J. A Service-Oriented Integration Platform for Flexible Information Provisioning in the Real-Time Factory. Ph.D. Thesis, Unversity of Stuttgart, Stuttgart, Germany, 2012. [Google Scholar] [CrossRef]

- Schel, D.; Henkel, C.; Stock, D.; Meyer, O.; Rauhöft, G.; Einberger, P.; Stöhr, M.; Daxer, M.A.; Seidelmann, J. Manufacturing Service Bus: An Implementation. Procedia CIRP 2018, 67, 179–184. [Google Scholar] [CrossRef]

- Hagiu, A.; Wright, J. Multi-Sided Platforms. Int. J. Ind. Org. 2015, 43, 162–174. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Rosing, M.V.; Scheer, A.W.; Scheel, H.V. The Complete Business Process Handbook: Body of Knowledge from Process Modeling to Bpm: Volume I; Morgan Kaufmann: Waltham, MA, USA, 2015. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Requirement Profile | Short Description | Request Duration | Remuneration |

|---|---|---|---|

| 1. Short-term load adjustment | Flexibility can compensate short-term fluctuations in generation or demand. | 5 min–1 h | Balancing power markets, interruptible load market, intraday-market |

| 2. Load adjustment over several hours | Mismatch of renewable generation and demand lead to significant fluctuations in electricity prices. | 3 to 12 h | Day-Ahead-Market, derivatives |

| 3. Reduction/increase of load over several days | Relevance for flexibility over longer periods increases with regard to the security of supply. | 1–5 days | Day-ahead-market, derivatives |

| 4. Atypical grid usage | By avoiding grid usage at congested times, the grid and procurement costs can be reduced. | Several hours per day | Reduction of network charges |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Roesch, M.; Bauer, D.; Haupt, L.; Keller, R.; Bauernhansl, T.; Fridgen, G.; Reinhart, G.; Sauer, A. Harnessing the Full Potential of Industrial Demand-Side Flexibility: An End-to-End Approach Connecting Machines with Markets through Service-Oriented IT Platforms. Appl. Sci. 2019, 9, 3796. https://doi.org/10.3390/app9183796

Roesch M, Bauer D, Haupt L, Keller R, Bauernhansl T, Fridgen G, Reinhart G, Sauer A. Harnessing the Full Potential of Industrial Demand-Side Flexibility: An End-to-End Approach Connecting Machines with Markets through Service-Oriented IT Platforms. Applied Sciences. 2019; 9(18):3796. https://doi.org/10.3390/app9183796

Chicago/Turabian StyleRoesch, Martin, Dennis Bauer, Leon Haupt, Robert Keller, Thomas Bauernhansl, Gilbert Fridgen, Gunther Reinhart, and Alexander Sauer. 2019. "Harnessing the Full Potential of Industrial Demand-Side Flexibility: An End-to-End Approach Connecting Machines with Markets through Service-Oriented IT Platforms" Applied Sciences 9, no. 18: 3796. https://doi.org/10.3390/app9183796