Operational Risk Management in Financial Institutions: A Literature Review

Abstract

:1. Introduction

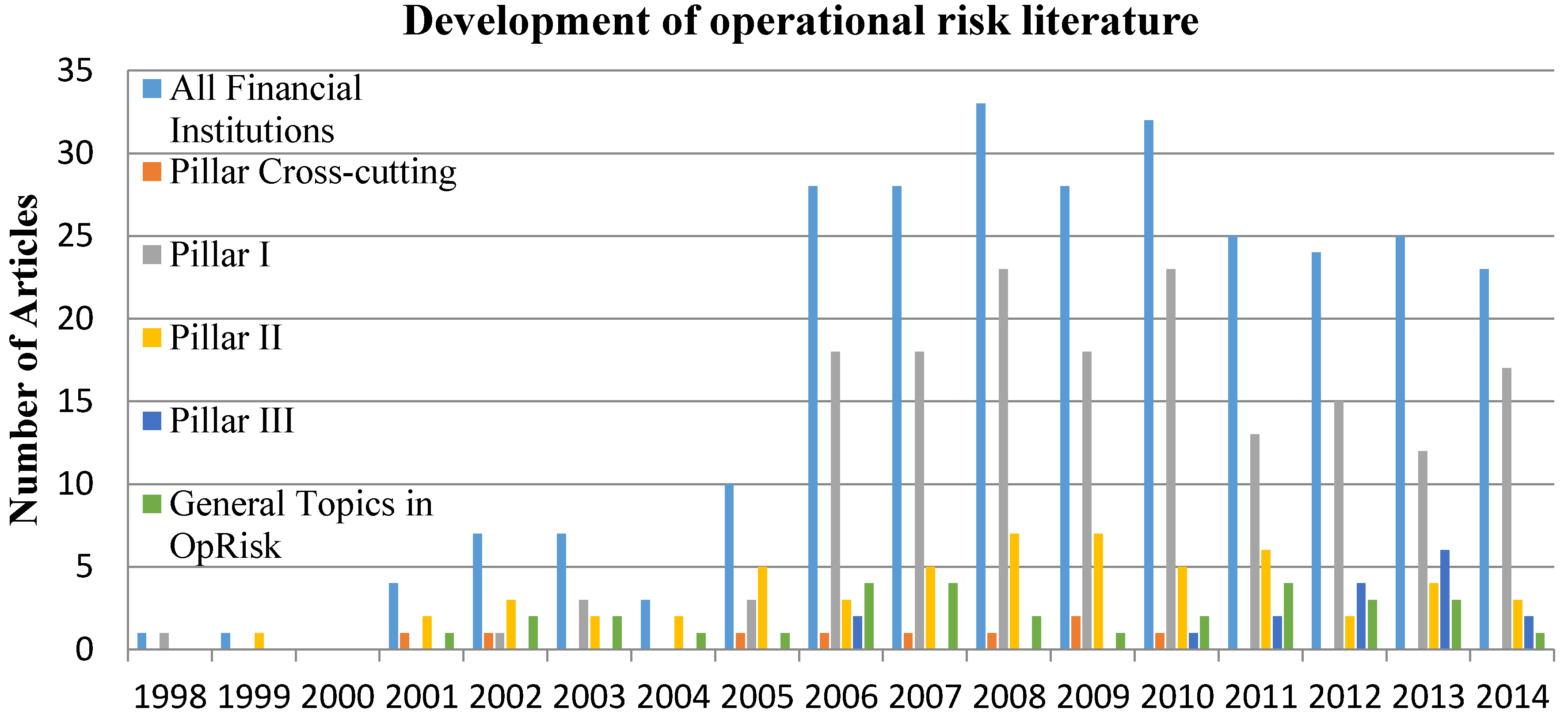

2. Methodology for the Literature Research

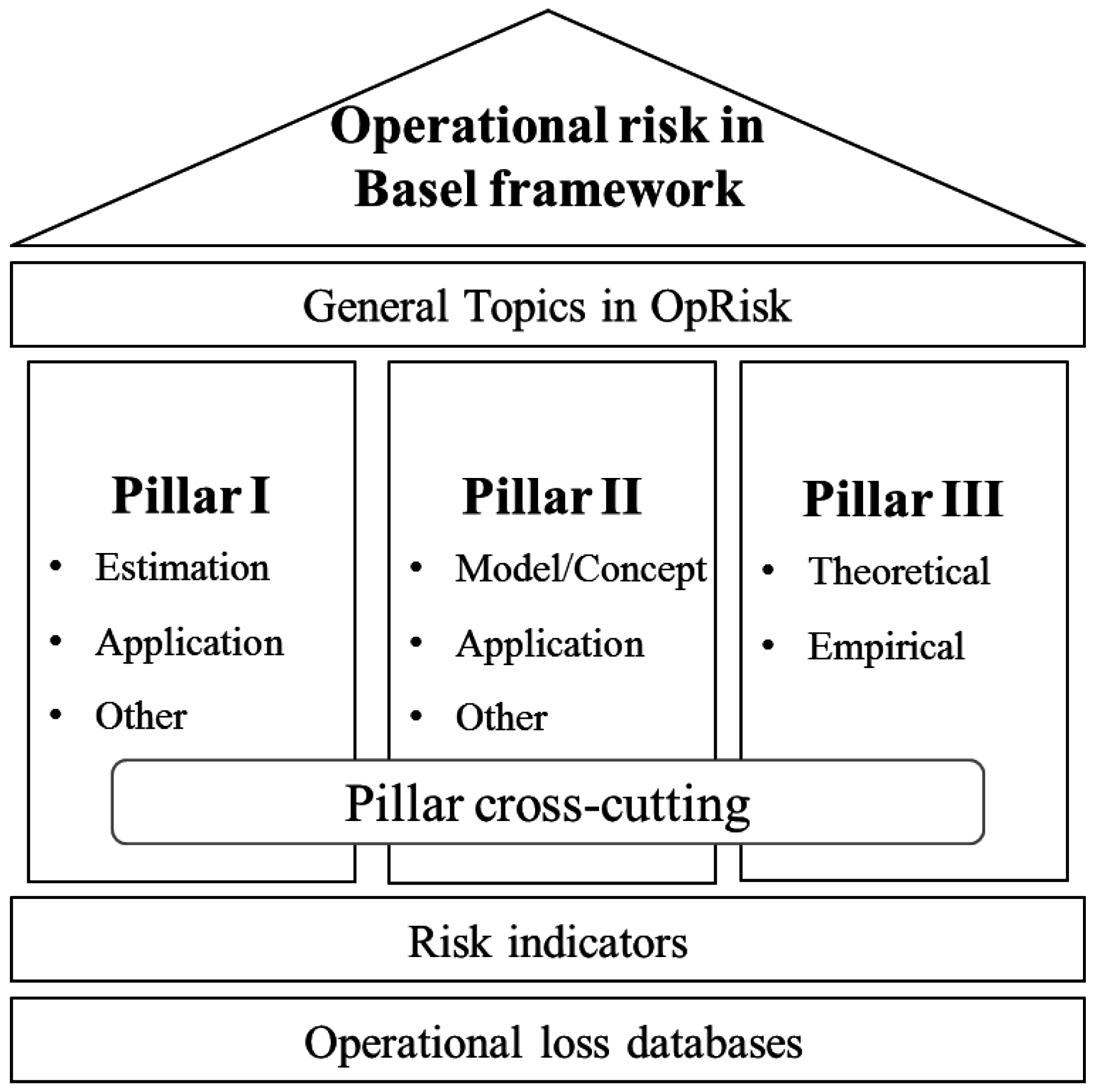

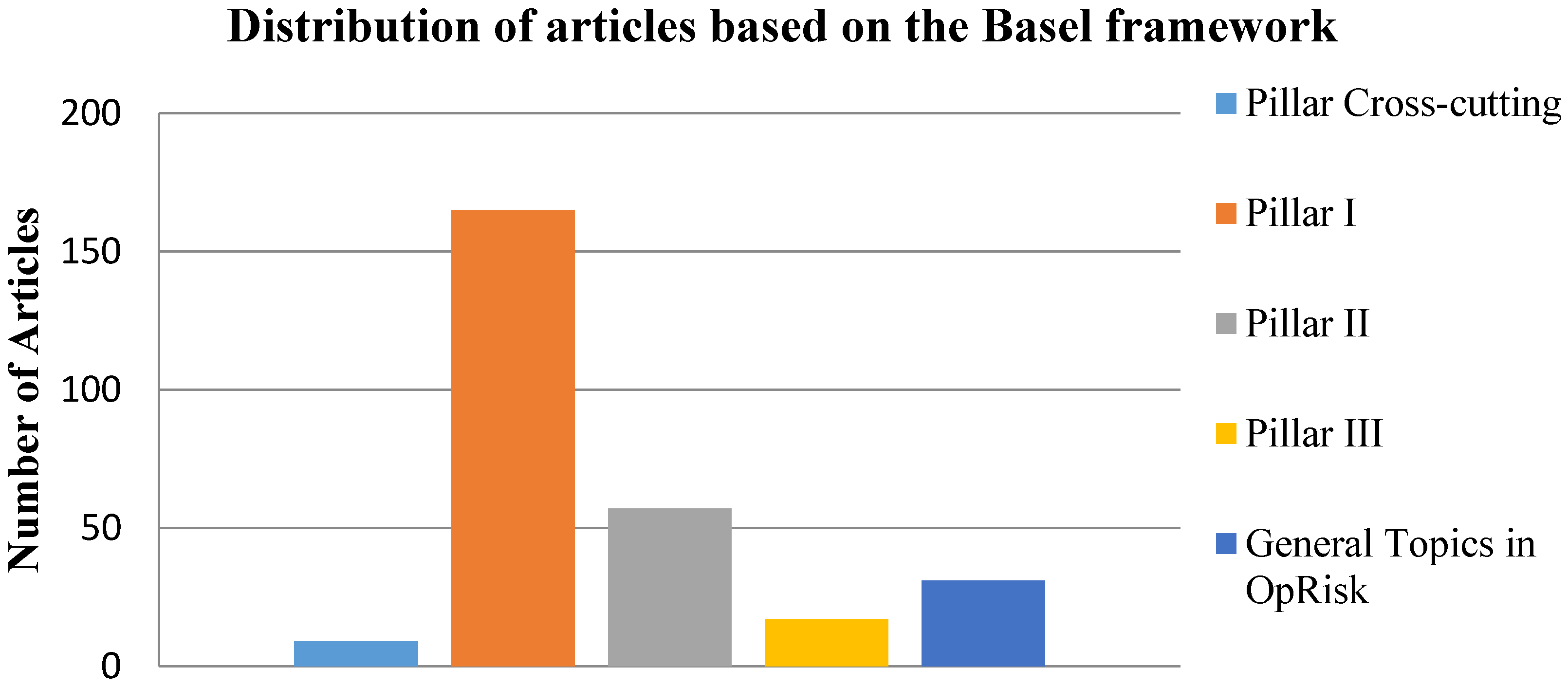

3. Categorisation of the Operational Risk Literature in the Basel II/III Framework

3.1. Pillar I

3.2. Pillar II

3.3. Pillar III

4. Operational Loss Databases

5. Risk Indicators

6. Conclusion and Directions for Future Research

Acknowledgments

Conflicts of Interest

References

- Basel Committee on Banking Supervision (BCBS). “Basel II: International Convergence of Capital Measurement and Capital Standards: A Revised Framework—Comprehensive Version.” June 2006. Available online: http://www.bis.org/publ/bcbs128.htm (accessed on 13 October 2015).

- I.A. Moosa. “Operational Risk: A Survey.” Financial Mark. Inst. Instrum. 16 (2007): 167–200. [Google Scholar] [CrossRef]

- G. Galloppo, and A. Rogora. “What Has Worked in Operational Risk? ” Glob. J. Bus. Res. 5 (2011): 1–17. [Google Scholar]

- T. Lagner, and D. Knyphausen-Aufseß. “Rating Agencies as Gatekeepers to the Capital Market: Practical Implications of 40 Years of Research.” Financial Mark. Inst. Instrum. 21 (2012): 157–202. [Google Scholar] [CrossRef]

- E. Brechmann, C. Czado, and S. Paterlini. “Flexible dependence modeling of operational risk losses and its impact on total capital requirements.” J. Bank. Finance 40 (2014): 271–285. [Google Scholar] [CrossRef]

- G. Galloppo, and D. Previati. “A review of methods for combining internal and external data.” J. Oper. Risk 9 (2014): 83–103. [Google Scholar] [CrossRef]

- S. Kerbl. “Evidence, estimates and extreme values from Austria.” J. Oper. Risk 9 (2014): 89–123. [Google Scholar] [CrossRef]

- X. Zhou, R. Giacometti, F.J. Fabozzi, and A.H. Tucker. “Bayesian estimation of truncated data with applications to operational risk measurement.” Quant. Finance 14 (2014): 863–888. [Google Scholar] [CrossRef]

- IBM Media Relations. “IBM to Acquire Algorithmics, 2011.” IBM Web Site. Available online: http://www-03.ibm.com/press/us/en/pressrelease/35176.wss (accessed on 29 August 2016).

- I.A. Moosa. “Misconceptions about operational risk.” J. Oper. Risk 1 (2006): 97–104. [Google Scholar]

- Ebscohost. “Business Source Premier. Magazines and Journals, 2016.” Ebscohot Research Database Web Site. Available online: https://www.ebscohost.com/titleLists/buh-journals.pdf (accessed on 7 October 2016).

- I.A. Moosa. “A Critique of the Bucket Classification of Journals: The ABDC List as an Example.” Econ. Rec. 92 (2016): 448–463. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision (BCBS). “Operational Risk Management.” September 1998. Available online: http://www.bis.org/publ/bcbs42.pdf (accessed on 13 October 2015).

- M. Cruz, R. Coleman, and G. Salkin. “Modeling and measuring operational risk.” J. Risk 1 (1998): 63–72. [Google Scholar] [CrossRef]

- R.H. Barros, and M.I.M. Torre-Enciso. “Capital assessment of operational risk for the solvency of health insurance companies.” J. Oper. Risk 7 (2012): 43–65. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision (BCBS). “Basel II: The New Basel Capital Accord—second consultative paper.” January 2001. Available online: http://www.bis.org/bcbs/bcbscp2.htm (accessed on 14 October 2015).

- J.A.C. Santos. “Bank Capital Regulation in Contemporary Banking Theory: A Review of the Literature.” Financial Mark. Inst. Instrum. 10 (2001): 41–84. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision (BCBS). “Enhancements to the Basel II framework.” July 2009. Available online: http://www.bis.org/publ/bcbs157.htm (accessed on 28 October 2015).

- M.B. Gordy, and B. Howells. “Procyclicality in Basel II: Can we treat the disease without killing the patient? ” J. Financial Intermediation 15 (2006): 395–417. [Google Scholar] [CrossRef]

- A.-M. Kessler. “A systemic approach to operational risk measurement in financial institutions.” J. Oper. Risk 2 (2007): 27–68. [Google Scholar]

- A.A. Jobst. “The credit crisis and operational risk - implications for practitioners and regulators.” J. Oper. Risk 5 (2010): 43–62. [Google Scholar] [CrossRef]

- E.W. Cope, M.T. Piche, and J.S. Walter. “Macroenvironmental determinants of operational loss severity.” J. Bank. Finance 36 (2012): 1362–1380. [Google Scholar] [CrossRef]

- A. Chernobai, P. Jorion, and F. Yu. “The Determinants of Operational Risk in U.S. Financial Institutions.” J. Financial Quant. Anal. 46 (2011): 1683–1725. [Google Scholar] [CrossRef]

- C. Hess. “The impact of the financial crisis on operational risk in the financial services industry: Empirical evidence.” J. Oper. Risk 6 (2011): 23–35. [Google Scholar] [CrossRef]

- C. Andreatta, and D. Mazza. “Alternative approaches to generalized Pareto distribution shape parameter estimation through expert opinions.” J. Oper. Risk 8 (2013): 47–72. [Google Scholar] [CrossRef]

- G. Arlt, F. Neumann, and U. Milkau. “A simple model for pseudo-nonstationarity in operational risk loss data due to interest rate dependency and reporting threshold.” J. Oper. Risk 8 (2013): 27–37. [Google Scholar] [CrossRef]

- S. Carrillo, H. Gzyl, and A. Tagliani. “Reconstructing heavy-tailed distributions by splicing with maximum entropy in the mean.” J. Oper. Risk 7 (2012): 3–15. [Google Scholar] [CrossRef]

- A. Cavallo, B. Rosenthalm, X. Wang, and J. Yan. “Treatment of the data collection threshold in operational risk: A case study using the lognormal distribution.” J. Oper. Risk 7 (2012): 3–38. [Google Scholar] [CrossRef]

- B. Ergashev, S. Mittnik, and E. Sekeris. “A Bayesian approach to extreme value estimation in operational risk modeling.” J. Oper. Risk 8 (2013): 55–81. [Google Scholar] [CrossRef]

- D. Guégan, and B.K. Hassani. “A Mathematical Resurgence of Risk Management: An Extreme Modeling of Expert Opinions.” Front. Finance Econ. 11 (2014): 25–45. [Google Scholar]

- V.S. Hari Rao, and K.V.N.M. Ramesh. “A checklist-based weighted fuzzy severity approach for calculating operational risk exposure on foreign exchange trades under the Basel II regime.” J. Oper. Risk 9 (2014): 105–124. [Google Scholar] [CrossRef]

- R.A. Jarrow. “Operational risk.” J. Bank. Finance 32 (2008): 870–879. [Google Scholar] [CrossRef]

- L. Tibiletti. “Value-at-risk: Is lacking in sub-additivity just an annoying technicality? ” Int. J. Risk Assess. Manag. 9 (2008): 44–51. [Google Scholar] [CrossRef]

- B. Tong, and C. Wu. “Asymptotics for operational risk quantified with a spectral risk measure.” J. Oper. Risk 7 (2012): 91–116. [Google Scholar] [CrossRef]

- A. Chernobai, and Y. Yildirim. “The dynamics of operational loss clustering.” J. Bank. Finance 32 (2007): 2655–2666. [Google Scholar] [CrossRef]

- E.W. Cope, and G. Antonini. “Observed correlations and dependencies among operational losses in the ORX consortium database.” J. Oper. Risk 3 (2008): 47–74. [Google Scholar]

- E.W. Cope, and A. Labbi. “Operational loss scaling by exposure indicators: evidence from the ORX database.” J. Oper. Risk 3 (2008): 25–45. [Google Scholar]

- E.W. Cope. “Modeling operational loss severity distributions from consortium data.” J. Oper. Risk 5 (2010): 35–64. [Google Scholar]

- E.W. Cope, G. Mignola, G. Antonini, and R. Ugoccioni. “Challenges and pitfalls in measuring operational risk from loss data.” J. Oper. Risk 4 (2009): 3–27. [Google Scholar] [CrossRef]

- H. Dahen, and G. Dionne. “Scaling models for the severity and frequency of external operational loss data.” J. Bank. Finance 34 (2010): 1484–1496. [Google Scholar] [CrossRef]

- P. De Fontnouvelle, V. Dejesus-Rueff, J.S. Jordan, and E.S. Rosengren. “Capital and Risk: New Evidence on Implications of Large Operational Losses.” J. Money Credit Bank 38 (2006): 1819–1846. [Google Scholar] [CrossRef]

- E. Gourier, W. Farkas, and D. Abbate. “Operational risk quantification using extreme value theory and copulas: From theory to practice.” J. Oper. Risk 4 (2009): 3–26. [Google Scholar]

- S. Li, D. Black, C. Lee, F. Famoye, and S. Li. “Dependence Models Arising from the Lagrangian Probability Distributions.” Commun. Stat. Theory Methods 39 (2010): 1729–1742. [Google Scholar] [CrossRef]

- R. Wei. “Quantification of operational losses using firm-specific information and external database.” J. Oper. Risk 1 (2006): 3–34. [Google Scholar]

- S. Figini, P. Giudici, and P. Uberti. “A threshold based approach to merge data in financial risk management.” J. Appl. Stat. 37 (2010): 1815–1824. [Google Scholar] [CrossRef]

- S. Figini, P. Giudici, P. Uberti, and A. Sanyal. “A statistical method to optimize the combination of internal and external data in operational risk measurement.” J. Oper. Risk 2 (2007): 69–78. [Google Scholar]

- C.-L. Liang. “Bayesian analysis of extreme operational losses.” J. Oper. Risk 4 (2009): 27–43. [Google Scholar]

- S. Mittnik, and T. Yener. “Estimating operational risk capital for correlated, rare events.” J. Oper. Risk 4 (2009): 29–51. [Google Scholar]

- J.D. Opdyke, and A. Cavallo. “Estimating operational risk capital: The challenges of truncation, the hazards of maximum likelihood estimation, and the promise of robust statistics.” J. Oper. Risk 7 (2012): 3–90. [Google Scholar] [CrossRef]

- J.D. Opdyke. “Estimating operational risk capital with greater accuracy, precision and robustness.” J. Oper. Risk 9 (2014): 3–79. [Google Scholar] [CrossRef]

- I.A. Moosa. “A critique of the advanced measurement approach to regulatory capital against operational risk.” J. Bank. Regul. 9 (2008): 151–164. [Google Scholar] [CrossRef]

- M. Chaudhury. “A review of the key issues in operational risk capital modeling.” J. Oper. Risk 5 (2010): 37–66. [Google Scholar]

- R. Correa, and S. Raju. “Capital charges for operational risk in the Indian banking sector: Alternative measures.” J. Oper. Risk 5 (2010): 65–82. [Google Scholar]

- P.E.K. Berg-Yuen, and E.A. Medova. “Economic capital gauged.” J. Bank. Regul. 6 (2005): 353–378. [Google Scholar] [CrossRef]

- S. Ashby. “Operational risk: Lessons from non-financial organisations.” J. Risk Manag. Financial Inst. 1 (2008): 406–415. [Google Scholar]

- D. Breden. “Monitoring the operational risk environment effectively.” J. Risk Manag. Financial Inst. 1 (2008): 156–164. [Google Scholar]

- D. Cernauskas, and A. Tarantino. “Operational risk management with process control and business process modeling.” J. Oper. Risk 4 (2009): 3–17. [Google Scholar]

- M.I. Fheili. “Information technology at the forefront of operational risk: Banks are at a greater risk.” J. Oper. Risk 6 (2011): 47–67. [Google Scholar] [CrossRef]

- A.D. Grody, and P.J. Hughes. “Financial services in crisis: Operational risk management to the rescue! ” J. Risk Manag. Financial Inst. 2 (2008): 47–56. [Google Scholar]

- P. McConnell. “LIBOR manipulation: operational risks resulting from brokers’ misbehavior.” J. Oper. Risk 9 (2014): 77–102. [Google Scholar] [CrossRef]

- P. McConnell. “People risk: Where are the boundaries? ” J. Risk Manag. Financial Inst. 1 (2008): 370–381. [Google Scholar]

- F. Bergeon, and M. Hensley. “Swiss cheese and the PRiMA model: What can information technology learn from aviation accidents? ” J. Oper. Risk 4 (2009): 47–58. [Google Scholar]

- J. Moodie. “Internal systems and controls that help to prevent rogue trading.” J. Secur. Oper. Custody 2 (2009): 169–180. [Google Scholar]

- B. Macklin, D. De Tora, E. Rath, and P. Rothman. “A Partnership Approach to Operational Risk Management.” Bank Account. Finance 16 (2003): 9–14. [Google Scholar]

- J. Hanssen. “Corporate Culture and Operational Risk Management.” Bank Account. Finance 18 (2005): 35–38. [Google Scholar]

- A. Sheen. “Implementing the EU Capital Requirement Directive—key operational risk elements.” J. Financ. Regul. Compliance 13 (2005): 313–323. [Google Scholar] [CrossRef]

- B.C. Adeleye, F. Annansingh, and M.B. Nunes. “Risk management practices in IS outsourcing: An investigation into commercial banks in Nigeria.” Int. J. Inf. Management 24 (2004): 167–180. [Google Scholar] [CrossRef]

- Financial Stability Board. Enhancing the Risk Disclosures of Banks. Report of the Enhanced Disclosure Task Force; Basel, Switzerland: Financial Stability Board, 29 October 2012. [Google Scholar]

- J.D. Cummins, C.M. Lewis, and R. Wei. “The market value impact of operational loss events for US banks and insurers.” J. Bank. Finance 30 (2006): 2605–2634. [Google Scholar] [CrossRef]

- J. Goldstein, A. Chernobai, and M. Benaroch. “An Event Study Analysis of the Economic Impact of IT Operational Risk and its Subcategories.” J. Assoc. Inf. Syst. 12 (2011): 606–631. [Google Scholar]

- M. Benaroch, A. Chernobai, and J. Goldstein. “An internal control perspective on the market value consequences of IT operational risk events.” Int. J. Account. Inf. Syst. 13 (2012): 357–381. [Google Scholar] [CrossRef]

- R. Gillet, G. Hübner, and S. Plunus. “Operational risk and reputation in the financial industry.” J. Bank. Finance 34 (2010): 224–235. [Google Scholar] [CrossRef]

- F. Fiordelisi, M.-G. Soana, and P. Schwizer. “The determinants of reputational risk in the banking sector.” J. Bank. Finance 37 (2013): 1359–1371. [Google Scholar] [CrossRef]

- F. Fiordelisi, M.-G. Soana, and P. Schwizer. “Reputational losses and operational risk in banking.” Eur. J. Finance 20 (2014): 105–124. [Google Scholar] [CrossRef]

- G. Cannas, G. Masala, and M. Micocci. “Quantifying reputational effects for publicly traded financial institutions.” J. Financ. Transform. 27 (2009): 76–81. [Google Scholar]

- P. Sturm. “Operational and reputational risk in the European banking industry: The market reaction to operational risk events.” J. Econ. Behav. Organ. 85 (2013): 191–206. [Google Scholar] [CrossRef]

- L. Biell, and A. Muller. “Sudden crash or long torture: The timing of market reactions to operational loss events.” J. Bank. Finance 37 (2013): 2628–2638. [Google Scholar] [CrossRef]

- I.A. Moosa, and L. Li. “The frequency and severity of operational losses: A cross-country comparison.” Appl. Econ. Lett. 20 (2013): 167–172. [Google Scholar] [CrossRef]

- I.A. Moosa, and P. Silvapulle. “An empirical analysis of the operational losses of Australian banks.” Account. Finance 52 (2012): 165–185. [Google Scholar] [CrossRef]

- S. Plunus, R. Gillet, and G. Hübner. “Reputational damage of operational loss on the bond market: Evidence from the financial industry.” Int. Rev. Financial Anal. 24 (2012): 66–73. [Google Scholar] [CrossRef]

- A. Barakat, A. Chernobai, and M. Wahrenburg. “Information asymmetry around operational risk announcements.” J. Bank. Finance 48 (2014): 152–179. [Google Scholar] [CrossRef]

- P. Sturm. “How much should creditors worry about operational risk? The credit default swap spread reaction to operational risk events.” J. Oper. Risk 8 (2013): 3–25. [Google Scholar] [CrossRef]

- G. Helbok, and C. Wagner. “Determinants of operational risk reporting in the banking industry.” J. Risk 9 (2006): 49–74. [Google Scholar] [CrossRef]

- J. Oliveira, L.L. Rodrigues, and R. Craig. “Voluntary risk reporting to enhance institutional and organizational legitimacy: Evidence from Portuguese banks.” J. Financial Regul. Compliance 19 (2011): 271–289. [Google Scholar] [CrossRef] [Green Version]

- M.F.A.E. Haija, and A.F. Al Hayek. “Operational Risk Disclosures in Jordanian Commercials Banks: It’s Enough.” Int. Res. J. Finance Econ. 83 (2012): 49–61. [Google Scholar]

- A. Barakat, and K. Hussainey. “Bank governance, regulation, supervision, and risk reporting: Evidence from operational risk disclosures in European banks.” Int. Rev. Financial Anal. 30 (2013): 254–273. [Google Scholar] [CrossRef]

- H. Sataputera Na, J. van den Berg, L.C. Miranda, and M. Leipoldt. “An econometric model to scale operational losses.” J. Oper. Risk 1 (2006): 11–31. [Google Scholar]

- M. Brunner, F. Piacenza, F. Monti, and D. Bazzarello. “Capital allocation for operational risk.” J. Risk Manag. Financial Inst. 2 (2009): 165–174. [Google Scholar]

- S. Ebnöther, P. Vanini, A. McNeil, and P. Antolinez. “Operational risk: A practitioner’s view.” J. Risk 5 (2003): 1–15. [Google Scholar] [CrossRef]

- D. Guégan, and B.K. Hassani. “Multivariate VaRs for operational risk capital computation: A vine structure approach.” Int. J. Risk Assess. Manag. 17 (2013): 148–170. [Google Scholar] [CrossRef]

- F. Monti, M. Brunner, F. Piacenza, and D. Bazzarello. “Diversification effects in operational risk: A robust approach.” J. Risk Manag. Financial Inst. 3 (2010): 243–258. [Google Scholar]

- A. Agostini, P. Talamo, and V. Vecchione. “Combining operational loss data with expert opinions through advanced credibility theory.” J. Oper. Risk 5 (2010): 3–28. [Google Scholar]

- A. Chernobai, and T.R. Svetlozar. “Applying robust methods to operational risk modeling.” J. Oper. Risk 1 (2006): 27–41. [Google Scholar] [CrossRef]

- M. Guillén, J. Gustafsson, and J.P. Nielsen. “Combining underreported internal and external data for operational risk measurement.” J. Oper. Risk 3 (2008): 3–24. [Google Scholar] [CrossRef]

- S. Lavaud, and V. Lehérissé. “Goodness-of-fit tests and selection methods for operational risk.” J. Oper. Risk 9 (2014): 21–50. [Google Scholar] [CrossRef]

- I.K. Mitov, S.T. Rachev, and F.J. Fabozzi. “Approximation of aggregate and extremal losses within the very heavy tails framework.” Quant. Finance 10 (2010): 1153–1162. [Google Scholar] [CrossRef]

- J. Feng, J. Li, L. Gao, and Z. Hua. “A combination model for operational risk estimation in a Chinese banking industry case.” J. Oper. Risk 7 (2012): 17–39. [Google Scholar] [CrossRef]

- F. Aue, and M. Kalkbrenner. “LDA at work: Deutsche Bank’s approach to quantifying operational risk.” J. Oper. Risk 1 (2006): 49–93. [Google Scholar]

- R.A. Jarrow, J. Oxman, and Y. Yildirim. “The cost of operational risk loss insurance.” Rev. Deriv. Res. 13 (2010): 273–295. [Google Scholar] [CrossRef]

- I.A. Moosa. “Operational risk as a function of the state of the economy.” Econ. Model. 28 (2011): 2137–2142. [Google Scholar] [CrossRef]

- N. Horbenko, P. Ruckdeschel, and T. Bae. “Robust estimation of operational risk.” J. Oper. Risk 6 (2011): 3–30. [Google Scholar]

- Standards Implementation Group’s Operational Risk Subgroup (SIGOR). Observed Range of Practice in Key Elements of Advanced Measurement Approaches (AMA) 2009. Basel, Switzerland: Bank for International Settlements. Press & Communications. Available online: http://www.bis.org/publ/bcbs160b.pdf (accessed on 13 October 2015).

- M.I. Fheili. “Developing human resources key risk indicators—Know Your Staff (KYS) practices.” J. Oper. Risk 1 (2006): 71–85. [Google Scholar]

- M.I. Fheili. “Employee turnover: An HR risk with firm-specific context.” J. Oper. Risk 2 (2007): 69–84. [Google Scholar]

- S. Scandizzo. “Risk Mapping and Key Risk Indicators in Operational Risk Management.” Econ. Notes 34 (2005): 231–256. [Google Scholar] [CrossRef]

- R. Cech. “Measuring causal influences in operational risk.” J. Oper. Risk 4 (2009): 59–76. [Google Scholar]

- E.W. Cope. “Combining scenario analysis with loss data in operational risk quantification.” J. Oper. Risk 7 (2012): 39–56. [Google Scholar] [CrossRef]

- U. Broll, and B. Eckwert. “Transparency in the interbank market and the volume of bank intermediated loans.” Int. J. Econ. Theory 2 (2006): 123–133. [Google Scholar] [CrossRef]

- Financial Services Authority (FSA). “FSA Final Notice 2012: Barclays Bank Plc, 2012.” FSA Web Site. Available online: http://www.fsa.gov.uk/static/pubs/final/barclays-jun12.pdf (accessed on 27 August 2016).

- J. Aharony, and I. Swary. “Contagion Effects of Bank Failures: Evidence from Capital Markets.” J. Bus. 56 (1983): 305–322. [Google Scholar] [CrossRef]

- A. Akhigbe, and J. Madura. “Why do contagion effects vary among bank failures? ” J. Bank. Finance 25 (2001): 657–680. [Google Scholar] [CrossRef]

- P. Jorion, and G. Zhang. “Good and bad credit contagion: Evidence from credit default swaps.” J. Financial Econ. 84 (2007): 860–883. [Google Scholar] [CrossRef]

- R.E. Lamy, and G.R. Thompson. “Penn Square, Problem Loans, and Insolvency Risk.” J. Financial Res. 9 (1986): 103–111. [Google Scholar] [CrossRef]

- R.H. Pettway. “Potential Insolvency, Market Efficiency, and Bank Regulation of Large Commercial Banks.” J. Financial Quant. Anal. 15 (1980): 219–236. [Google Scholar] [CrossRef]

- I. Swary. “Stock Market Reaction to Regulatory Action in the Continental Illinois Crisis.” J. Bus. 59 (1986): 451–473. [Google Scholar] [CrossRef]

- Consumer Financial Protection Bureau (CFBP). “CFPB Probe into Capital One Credit Card Marketing Results in $140 Million Consumer Refund, 2012.” CFBP Web Site. Available online: http://www.consumerfinance.gov/newsroom/cfpb-capital-one-probe/ (accessed on 27 August 2016).

- Consumer Financial Protection Bureau (CFBP). “CFPB Orders Bank of America to Pay $727 Million in Consumer Relief for Illegal Credit Card Practices, 2014.” CFBP Web Site. Available online: http://www.consumerfinance.gov/newsroom/cfpb-orders-bank-of-america-to-pay-727-million-in-consumer-relief-for-illegal-credit-card-practices/ (accessed on 27 August 2016).

- Consumer Financial Protection Bureau (CFBP). “CFPB Orders Chase and JPMorgan Chase to Pay $309 Million Refund for Illegal Credit Card Practices, 2013.” CFBP Web Site. Available online: http://www.consumerfinance.gov/newsroom/cfpb-orders-chase-and-jpmorgan-chase-to-pay-309-million-refund-for-illegal-credit-card-practices/ (accessed on 27 August 2016).

- Consumer Financial Protection Bureau (CFBP). “CFPB Orders American Express to Pay $59.5 Million for Illegal Credit Card Practices, 2013.” CFBP Web Site. Available online: http://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-american-express-to-pay-59-5-million-for-illegal-credit-card-practices/ (accessed on 27 August 2016).

- A. Edmans. “Blockholders and Corporate Governance.” Annu. Rev. Financial Econ. 6 (2014): 23–50. [Google Scholar] [CrossRef]

- A.R. Admati, and P. Pfleiderer. “The “Wall Street Walk” and Shareholder Activism: Exit as a Form of Voice.” Rev. Financial Stud. 22 (2009): 2645–2685. [Google Scholar] [CrossRef]

- J. Zwiebel. “Block Investment and Partial Benefits of Corporate Control.” Rev. Econ. Stud. 62 (1995): 161–185. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision (BCBS). Standardised Measurement Approach for operational risk. Consultative Document; Basel, Switzerland: Bank for International Settlements, 2016. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Category | Subcategory | Number of Articles | Percentage |

|---|---|---|---|

| Pillar I | |||

| a) Estimation | 81 | 49.09% | |

| b) Application | 79 | 47.88% | |

| c) Other | 5 | 3.03% | |

| Sum | 165 | 100% | |

| Pillar II | |||

| a) Model/Concept | 41 | 71.93% | |

| b) Application | 10 | 17.54% | |

| c) Other | 6 | 10.53% | |

| Sum | 57 | 100% | |

| Pillar III | |||

| a) Theoretical | 0 | 0.00% | |

| b) Empirical | 18 | 100.00% | |

| 1) Event study | 14 | 77.78% | |

| 2) Other | 4 | 22.22% | |

| Sum | 18 | 100% | |

| Study | Sample Period | Num. of OL Events | Market | Operational Loss Database | Market Value | Reputational Damage | Dependence on Basel II Event Types |

|---|---|---|---|---|---|---|---|

| [69] | 1978–2003 | 492 | U.S. | Algo OpVantage | decline | YES | NO |

| [70] | 1985–2009 | 142 | U.S. | Algo FIRST | decline | not examined | not examined |

| [71] | 1985–2009 | 142 | U.S. | Algo FIRST | decline | not examined | not examined |

| [72] | 1990–2004 | 154 | U.S. + EU | Algo OpVantage | decline | YES | YES |

| [73] | 2003–2008 | 215 | U.S. + EU | Algo OpVantage | decline | YES | YES |

| [74] | 1994–2008 | 430 | U.S. + EU | Algo OpVantage | decline | YES | YES |

| [75] | 2000–2006 | 20 | U.S. + EU | Algo OpVantage | decline | YES | not examined |

| [76] | 2000–2009 | 136 | EU | ÖffschOR | decline | YES | NO |

| [77] | 1974–2009 | 279 | EU | Algo OpVantage | decline | YES | YES |

| [78] | 1999–2008 | 163 | GB | Algo FIRST | decline | NO | NO |

| [79] | 1990–2007 | 54 | Australia | Algo FIRST | decline | YES | NO |

| Databases | Banks’ Internal Databases or Unidentified | Self-Collected | ORX | GOLD | DakOR | ÖffschOR | Operational Loss Data Sharing Consortium | Algo FIRST | Algo OpVantage | SAS OpRisk Global Data | Italian Database of Operational Losses (DIPO) | Austrian Loss Data Collection |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| non-profit associations | 0 | 0 | 6 | 0 | 0 | 2 | 1 | 0 | 0 | 0 | 0 | 1 |

| private vendors | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 13 | 11 | 3 | 3 | 0 |

| publicly available events | 0 | 6 | 0 | 0 | 0 | 2 | 0 | 13 | 11 | 3 | 0 | 0 |

| publicly not-available events | 52 | 0 | 6 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 1 |

| Total | 96 |

- 1Losses are taken from the ÖffSchOR Database provided by the Association of German Public Sector Banks (Bundesverband öffentlicher Banken, VÖB).

- 2While assessing the literature on operational risk, we observe a wide range of definitions on operational risk that are discussed in detail by Moosa [2].

- 3Algorithmics was acquired by IBM in 2011 (see [9]).

- 4See the Pillar III subsection.

- 5EBSCO Business Source Premier provides full text for nearly 6159 scholarly business journals and magazines, including full text for more than 1114 peer-reviewed business publications. For more details, see [11]. Google Scholar provides a search of scholarly literature across many disciplines and sources. For more details, see https://scholar.google.com/intl/us/scholar/help.html#coverage (accessed on 07 October 2016).

- 6Lagner and Knyphausen-Aufseß [4] collect articles from journals ranked with A and B by the German Academic Association of Business Research (VBA) and papers available in the Social Science Research Network (SSRN) over the last three years.

- 7For more detailed critique of journal ranking see [12].

- 8This definition has not been changed until now.

- 9For comparison, the literature related to operational risk in the insurance sector can be identified only up to 2004 and reached its peak in 2012, indicating a growth of interest in the topic (see, for example, [15]).

- 10Despite the fact that the Basel Committee excludes reputational risk from the operational risk definition and defines it as “the risk arising from negative perception on the part of customers, counterparties, shareholders, investors, debt-holders, market analysts, other relevant parties or regulators that can adversely affect a bank’s ability to maintain existing, or establish new, business relationships and continued access to sources of funding” [18] (p. 19), former research focuses on measuring the extent of reputation losses based on the market reaction to an operational loss announcement and provides empirical evidence about significant reputational damage. As a measure of reputational damage, the operational risk literature suggests the market value decline by the operational risk event announcing firm that exceeds the reported loss amount (see the review of literature in the following “Pillar III” section).

- 11Under the Basel II framework, banks are required to use one of the three methods for the estimation of regulatory capital for operational risk: (i) the Basic Indicator Approach (BIA); (ii) the Standardized Approach (STA); and (iii) Advanced Measurement Approaches (AMA) (see [1]).

- 12A list of articles included in this subcategory is available from the authors upon request.

- 13A list of articles included in this subcategory is available from the authors upon request.

- 14The Basel Committee classifies operational risk events into seven loss event type categories: Internal Fraud (ET1), External Fraud (ET2), Employment Practices and Workplace Safety (ET3), Clients, Products, and Business Practices (ET4), Damage to Physical Assets (ET5), Business Disruption and System Failures (ET6) and Execution, Delivery, and Process Management (ET7) (see [1]).

- 15The expression ‘“real” operational loss’ is defined in this paper as losses collected in compliance with the Basel II definition of operational risk.

- 16Among these studies, Chernobai and Svetlozar [93] note that the data used in their study are obtained from major European operational public loss data and provide no further information. Mitov et al. [96] resample their data with added heavy-tailed noise to ensure the anonymity of provided data. Feng et al. [97] conduct research based on 860 self-collected operational loss events from various publicly available sources, such as newspapers and court judgments.

- 17For further details, see www.ORX.org (accessed on 29 August 2016).

- 18More details are available under http://www.voeb-service.de/ (accessed on 29 August 2016).

- 19Although the study at hand provides a comprehensive review of the operational risk literature, our sample can be biased against studies not published in peer-reviewed journals.

© 2016 by the author; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pakhchanyan, S. Operational Risk Management in Financial Institutions: A Literature Review. Int. J. Financial Stud. 2016, 4, 20. https://doi.org/10.3390/ijfs4040020

Pakhchanyan S. Operational Risk Management in Financial Institutions: A Literature Review. International Journal of Financial Studies. 2016; 4(4):20. https://doi.org/10.3390/ijfs4040020

Chicago/Turabian StylePakhchanyan, Suren. 2016. "Operational Risk Management in Financial Institutions: A Literature Review" International Journal of Financial Studies 4, no. 4: 20. https://doi.org/10.3390/ijfs4040020