Composition and Activity of the Board of Directors: Impact on ESG Performance in the Banking System

1

Department of Management and Business Administration, “G. d’ Annunzio” University of Chieti-Pescara, 65127 Pescara, Italy

2

Department of Economics, University of Foggia, 71121 Foggia, Italy

3

Ionian Department of Law, Economics and Environment, University of Bari Aldo Moro, 74121 Taranto, Italy

4

Department of Economics, University of Salento, 73100 Lecce, Italy

5

Rimini Centre for Economic Analysis, 47921 Rimini, Italy

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(12), 4699; https://doi.org/10.3390/su10124699

Submission received: 10 November 2018

/

Revised: 1 December 2018

/

Accepted: 4 December 2018

/

Published: 10 December 2018

Abstract

:A growing body of research suggests that the composition of a firm’s board of directors can influence its environmental, social and governance (ESG) performance. In the banking industry, ESG performance has not yet been explored to discover how a critical mass of women on the board of directors affects performance. This paper seeks to fill this gap in the literature by testing the impact of a critical mass of female directors on ESG performance. Other board characteristics are accounted for: independence, size, frequency of meetings and Corporate Social Responsibility (CSR) committee. We use fixed effects panel regression models on a sample of 108 listed banks in Europe and the United States for the period 2011–2016. Our main empirical evidence shows that the relationship between women on the board of directors and a bank’s ESG performance is an inverted U-shape. Therefore, the critical mass theory for banks is not supported, confirming that only gender-balanced boards positively impact a bank’s performance for sustainability. There is a positive link between ESG performance and board size or the presence of a CSR committee, while it is negative with the share of independent directors. With this work, we stress the key role of corporate governance principles in banks’ ESG performance, with relevant implications for both banks and supervisory authorities.

1. Introduction

A company’s success essentially depends on the board of directors [1], given that they are responsible for approving and overseeing the implementation of strategic goals, the system of governance and creating company culture [2]. A successful board will also place an emphasis on business ethics and corporate responsibility [3]. An increasing amount of research finds a strong positive relationship between a firm’s sustainability performance and profitability: companies with high sustainability ratings significantly outperform their counterparts both in terms of stock market value and accounting performance [4]. In other words, adopting environmental, social and governance (ESG) best practices leads to a long-term competitive advantage. Businesses are well aware of the fact that their survival depends on achieving one or more Sustainability Development Goals (SDGs), particularly on the climate.

The High-Level Expert Group on Sustainable Finance (HLEG) used this evidence in its final 2018 report to suggest strengthening the director’s duties related to sustainability by urging them to take into consideration the “likely consequences of any decision in the longer term, the interests of the company’s employees and the impact of the company’s operations on the community and the environment (externalities), safeguarding the world’s cultural and natural heritage” [5] (p. 40). Therefore, it is increasingly important for members of governing bodies to address long-term sustainability risks and to integrate them into their corporate strategy and business models [2]. To achieve this, supervisory authorities should verify that boards of directors are knowledgeable on sustainability issues and are able to understand and value ESG preferences of stakeholders.

Based on these considerations, this study aims to identify the characteristics of the board of directors, which raise corporate social responsibility (CSR) performance. More specifically, according to the existing literature [6,7,8,9,10], our analysis examines the impact of a board’s characteristics (gender diversity, independence, size, activity and CSR sustainability committee) on CSR performance in the banking industry from 2011 to 2016. Our focus on the banking industry allows for a more homogeneous reference population and is important because banks, in mobilising substantial financial resources, represent one of the main economic drivers that can enhance the transition towards a more inclusive and sustainable economy [3,5]. To proxy a bank’s sustainability performance, we use Thomson Reuters’ ESG Asset4 score, a broad and verified measure of CSR performance adopted by scholars both for financial [11] and non-financial firms, e.g., [10,12,13]. The ESG Asset4 database provides objective, relevant and auditable ESG information for over 3400 publicly listed companies covering major indices, such as the NASDAQ100, S & P500, FTSE350, and MSCI World. Consulting official corporate documents (but also company websites, newspapers, journals, and trade publications), Thomson Reuters’ analysts collect 750 data points per firm that are used as inputs to calculate 250 key performance indicators (KPIs). The final score (ESG Asset4) ranges from 0 to 100, with a higher score indicating better sustainability performance. In sum, the ESG performance score is an ethical rating that aims at certifying the firm’s CSR quality, in other words, the non-financial performance of a company in three complementary areas: environment, governance and social. An increasing number of investors worldwide have adopted the ESG as a proxy for a company’s CSR performance in order to account for environmental, social, and corporate governance issues in their investment decisions. The ESG performance provides complementary information to the firm’s corporate financial performance (CFP), which is based only on economic and financial results. A great number of studies have investigated the link between sustainability performance (expressed by an ESG score or other measures of CSR) and CFP by showing, in most cases, a highly significant, positive and robust relationship, which holds across the countries and industries investigated [14]. In light of these considerations, for the purpose of this paper, we use the terms ESG, sustainability and CSR performance interchangeably.

Our main empirical evidence shows that there is a non-linear relationship between women on the board of directors and a bank’s ESG performance. Interestingly, the relationship between these two variables is an inverted U-shape, confirming that only gender-balanced boards positively impact a bank’s sustainability performance. Therefore, we do not support the critical mass theory for banks stricto sensu, meaning that after reaching a critical mass of women on the board, an increasing presence of female directors does not necessarily have a positive impact on a bank’s sustainability performance. Moreover, the linkage of ESG performance with board size and the presence of a CSR sustainability committee is positive, while it is negative with the share of independent directors.

This study contributes both to academic literature and to bank practices in several aspects. Firstly, current literature on the topic (relationship between board composition and ESG performance) primarily concentrates on non-financial firms, while this study focuses only on the banking industry. Secondly, to the best of our knowledge, existing studies on banks that analyse the relationship between governance variables and sustainability primarily deal with the CSR disclosure (and not the CSR performance) generally focus on developing economies and finally cover an old time interval [15,16,17,18,19]. Conversely, our empirical research covers the years 2011–2016 and analyses a large sample of 108 listed banks in Europe and the United States, two developed regions of which economies notably contribute to sustainable development. Thirdly, we add value to the existing literature, for the banking sector, by testing Kanter’s theory [20] on the critical mass of women on boards of directors. Consistent with the critical mass theory, a threshold of at least three women on the board is necessary before it has a significant impact on board dynamics or level of activity, and substantially change the board’s processes [21,22]. To test this theory in a more general scheme, we also look for a non-linear, U-shaped relationship between gender diversity and sustainability performance. Without imposing the three women rule for boards with very different sizes, we endogenously determine the value of the critical mass of women by including a quadratic term for the proportion of female directors on the board and by computing the turning point in the predicted ESG performance of the banks [23,24]. In general, all our results contribute to the definition of bank best practices, especially for the composition of a bank’s board, which is an important driver of sustainable development.

The remainder of the paper is organized as follows. Section 2 presents the literature review and the research hypotheses. Section 3 discusses the research method, including the sampling procedure, the measurement of dependent and independent variables and the methodology used. Section 4 shows and discusses the results, and finally, Section 5 presents the conclusions.

2. Literature Review and Hypotheses Development

The variables most widely used in the literature to describe the impact of corporate governance on ESG performance are related to the share of women on the board of directors (or board gender diversity), the share of independent directors on the board of directors (or board independence), board size, the number of board meetings per year and the existence of a CSR sustainability committee. In the sub-sections below, we develop our hypotheses for each of these characteristics of corporate governance.

2.1. Women on the Board

Interpretations of the relationship between women on the board and ESG performance are connected to the various features of the women themselves. For example, their educational and professional backgrounds could push them towards being more sensitive to sustainability initiatives than men [25,26]. Additionally, some typically female psychological traits (i.e., helpfulness, sensitivity, or attention to the welfare of others) are found to result in socially oriented behaviors [27,28]. Finally, women tend to adopt work styles involving participative communication, democratic decision-making and process orientation, which facilitate identifying and meeting stakeholders’ needs and expectations [26,27,29]. In sum, there are significant differences in values, beliefs, backgrounds, perceptions and work styles between women and men, so women seem to have greater empathy towards stakeholders’ issues and sustainability practices.

In light of these considerations, having more women on the board can influence a firm’s sensitivity towards social and environmental issues. There seems to be a general consensus in the literature regarding the positive impact of female directors on sustainability performance. More in detail, women on boards positively impact the firm’s charitable contributions [25,30], apprehension for climate change [31], Kinder, Lydenberg, Domini (KLD) strengths [8] and reputation-based CSR measures [28]. Similarly, many studies find that board gender diversity increases the extent of social and environmental reporting [7,15,32,33,34,35,36] and decreases environmental lawsuits [37]. However, there are also studies with different contradictory results such as a weak statistically significant positive impact [19,38], no significant association [39,40,41,42,43] or a negative association [44,45] between social and environmental practices and the presence of female directors.

A likely explanation of these inconsistent results could be the presence of a non-linear relationship between board gender diversity and social and environmental performance. In other words, only when there is at least a significant minority of women in a group, namely a threshold or critical mass, can women provide new perspectives, abilities and skills and hence positively influence group culture, interactions and performance [20]. Based on the critical mass theory, some studies [21,22] point out that an absolute number of at least three women on the board is necessary to exert significant power on board activeness and to substantially change the dynamics and the processes within the board.

In spite of its fame and use in legislative and political research [46,47], Kanter’s theory has rarely been tested in business environments. Concerning social and environmental issues, Post et al. [6] show that companies with boards comprising three or more female directors present higher KLD ratings in the environmental strength areas. This result is in line with Boulota [48], who finds that the higher the board gender diversity, the fewer the negative corporate social performance (CSP) practices, expressed by KLD concerns. Similarly, Fernandez-Feijoo et al. [49,50] find that at least three female directors are a determinant for the level and transparency of CSR disclosure. Additionally, Cabeza-García et al. [51] find that a critical mass of at least three women on the board leads to better firm CSR disclosure. Partial confirmation of the critical mass theory is provided by Manita et al. [52]: the authors show that the relationship between board gender diversity and ESG disclosure is not statistically significant below a level of three female directors, even though on the whole, they do not find significant relationship. Finally, environmental disclosure also seems to be positively influenced by the presence of a critical mass of female directors [53,54], and Liu [37] documents that firms with three or more women on the boardroom experience significantly fewer environmental litigations. Some studies show similar results while focusing on financial performance. Among these, Liu et al. [55] document that boards with three or more female directors provide a more significant impact on firm performance than boards with two or fewer. Additionally, Joecks et al. [23] show that only a critical mass of about 30%, which corresponds to three women on the board, is associated with higher financial performance. These findings are confirmed by Farag and Mallin [24], who find a non-linear relationship between bank financial performance and women on management boards, and by Owen and Temesvary [56], who confirm the non-linear relationship when banks are well-capitalized.

In consideration of this evidence, we advance the following hypothesis:

Hypothesis 1.

A critical mass of women on the board of directors has a positive effect on ESG performance.

2.2. Independent Directors

The variable most frequently adopted by scholars to describe the structure of the board is independence of the company board [57] since it is considered key to ensuring effective board monitoring and linking the firms’ strategic policies to stakeholders’ interests and expectations [58]. According to agency theory, independent directors facilitate effective oversight on board practices as they are able to produce more objective judgments on management performance [2]. This occurs because these managers are less involved in the company’s operations and thus they are less dependent on control exerted by the Chief Executive Officer (CEO) [59]. Moreover, unlike inside directors, an independent director’s compensation is not related to short-term financial performance. Hence, boards with higher independence are supposed to be better at monitoring [60,61] and to be more inclined towards social responsibility [18,62]. Similarly, according to stakeholder theory, greater board independence reduces the conflicts of interests between different stakeholders, encouraging management activities to maximize long-term value and higher levels of transparency [60,61]. Board independence is generally considered the main characteristic of a board associated with protecting stakeholder interests. For these reasons, many authors suggest that boards with higher proportions of independent directors encourage higher level of voluntary disclosure and facilitate engagement in CSR investments [61,63].

However, even if most studies linking board independence to CSR seem to confirm a positive relationship [60], other studies find that the presence of non-executive and independent directors on boards has a negative impact on social and environmental disclosure [64,65,66] and environmental performance [41]. Further studies document non-significant association [67,68,69,70], while Ortiz-de-Mandojana et al. [71] suggest that the contribution of independent directors to the growth of a firm’s environmental sustainability is affected by the national institutional context.

With regard to the banking industry, Basel Committee on Banking Supervision recently stated that “the board must be suitable to carry out its responsibilities and have a composition that facilitates effective oversight. For that purpose, the board should be comprised of a sufficient number of independent directors” [2] (p. 32). However, while positive results are found by Barako and Brown [15], Jizi et al. [18] and Kiliç et al. [19], no significant linkage is shown by Hossain and Reaz [72]. In addition, studies on banks mostly concern the CSR disclosure and do not report strong empirical evidence with respect to CSR performance.

Therefore, on the basis of these inconsistent findings, we posit the following hypothesis:

Hypothesis 2.

There is a positive/negative relationship between independent directors and ESG performance.

2.3. Board Size

Board size has mostly been studied as to its relationship to firm performance. Empirical studies can be classified into two categories: a first stream of research is in favor of smaller boards, whereas a second school of thought advocates larger boards.

On the one hand, considering group dynamics and collective decision-making process along with the agency perspective, smaller boards are expected to be more effective at monitoring and controlling in firm governance than larger boards [42,60,73,74] and better able to mitigate managers’ opportunistic behavior to the detriment of shareholders. In particular, smaller boards foster good cohesion, coordination and communication among directors [60,75], and hence they intensify the accountability and commitment of individual members.

On the other hand, from a legitimation perspective, smaller boards might have a low degree of diversification in terms of education, expertise, gender and stakeholder representation [76,77], and entail higher workload and responsibilities for the directors, who therefore might less effectively carry out their role as monitors [78,79]. Conversely, larger boards have better workload allocation and wider collective expertise. The reaction of the stock markets depends on the variation in the number of directors: it is positive when the number of directors increases and negative when it decreases [80].

Board size depends on a firm’s complexity, so its industry and size are important factors that influence the number of directors [81,82]. Since the banks in our sample are listed, and are therefore large and complex financial institutions that work in a context of intense regulation, we expect that larger boards will be more efficient, especially in terms of workload and responsibility allocation, and of greater diversity in terms of stakeholder representation, when engaging in good ESG practices and improving ESG performance [18,61]. Our hypothesis agrees with the findings of previous studies that show a positive relationship between board size and the breadth of sustainability practices [17,18,59,61,83,84,85,86,87].

Based on the previous considerations, the following hypothesis is proposed for testing:

Hypothesis 3.

Board size has a positive effect on ESG performance.

2.4. Board Meetings

For the number of board meetings per year, which is usually used as a proxy for the level of board activity and board diligence [76,88], there is also no consensus about impact on non-financial performance.

On the one hand, more frequent meetings denote the inefficacy of directors and thereby poor performance of the activities they carry out, higher coordination costs [88] and the possibility of simply splitting the agenda into many meetings without expanding sustainability issues [89].

On the other hand, a high frequency of meetings allows the directors better oversight of firm operations and is beneficial to shareholders, so the number of meetings is an important resource in improving the effectiveness of a board [90,91]. Furthermore, board meetings allow the directors to share more information and viewpoints, improving the decision-making process [76] and ensure legitimacy of all stakeholder expectations in a dynamic business environment. In reality, it is necessary to meet frequently in order to co-ordinate actions that are considered useful when facing the negative impacts emerging from events related to sustainability [89].

Since the banks in our sample work in a dynamic business environment, which requires increased meeting frequency to ensure legitimacy, legitimacy theory provides the basis for proposing a positive relationship between board meeting frequency and ESG performance. Our hypothesis aligns with the studies that find a positive relationship between the number of board meetings and sustainability practices [18,59,92,93,94].

Based on the previous considerations, the following hypothesis is tested:

Hypothesis 4.

The number of board meetings has a positive effect on ESG performance.

2.5. CSR Sustainability Committee

In recent years, companies are more frequently choosing to establish a CSR committee to handle important sustainability duties. According to stakeholder theory, such committees typically assist the board of directors in overseeing the company’s responsibility practices, but they can also play a key role in monitoring and assessing the firm’s CSR performance by ensuring compliance with regulations that manage sustainability risks [95]. Indeed, the board can design and implement CSR projects through a CSR committee, increasing stakeholder participation in the company’s ethical culture and ensuring risks that could be dangerous to the firm’s reputation are properly assessed [2,57]. Moreover, the CSR committee is responsible for the reporting procedures of environmental and social information: it reports periodically to the board of directors on sustainability matters affecting the company, while also managing the public disclosure on sustainability issues.

For these reasons, creating a CSR committee is seen as an important mechanism for an organization to maximize opportunities for sustainable development. As noted by Hussain et al. [94] (p. 418), “the existence of a CSR committee symbolises the board’s orientation and commitment towards sustainable development”. Additionally, Liao et al. state that [96] (p. 414) “the role of an environmental committee with respect to environmental disclosure is analogous to the role of an audit committee in ensuring proper financial accounting disclosures”. In summary, a company that chooses to establish a CSR committee demonstrates not only its CSR commitment to stakeholders, but also its intention to make sustainability a key core strategy [42,92,97]. For these reasons, many authors find that the presence of a CSR committee is positively associated with the extent and/or the quality of sustainability disclosure. Among these, Amran et al. [42] find that the existence of a CSR committee enhances the quality of sustainability reporting. Equally, Cucari et al. [56] show that the existence of a CSR committee increases the ESG disclosure score provided by the Bloomberg database. Similar results are also found with respect to environmental disclosure: Adnan et al. [98] and Liao et al. [96] argue that when companies establish an environmental committee, their transparency on greenhouse gas emissions is greater. More recently, Helfaya and Moussa [12] suggest that the existence of CSR committees is significant and positively connected to more relevant and credible environmental information. Finally, Spitzeck [99] confirms that CSR committees benefit companies in achieving higher levels of CSR performance.

On the contrary, only a limited number of studies reveal a negative relationship between CSR committee and CSR disclosure/performance [32,100].

For these motivations, we posit the following and last research hypothesis:

Hypothesis 5.

The establishment of a CSR sustainability committee has a positive effect on ESG performance.

3. Research Methodology

3.1. Sample Selection and Data Sources

Our sample comprised 108 listed banks in Europe and the United States, for which data on ESG performance was available on the date of analysis. We constructed a six-year panel dataset (from 2011 to 2016, the last year available in our data sources), including 406 bank-year observations, after listwise deletion for missing values.

Data on ESG performance and corporate governance (women on the board of directors, independent directors, board size, number of board meetings, CSR committee, background and skills) came from the Thomson Reuters Asset4 database, which has been used in recent studies [12,13,101,102,103]. Bank-specific financial data (total assets, profitability and leverage) was collected from Thomson Reuters Datastream, while the country variable (Gross Domestic Product (GDP) per capita) was collected from the World Bank Data.

3.2. Dependent Variable

To test our hypotheses, we used data on ESG performance (ESG SCORE) from Asset4. This score is based on three dimensions: environmental, social and corporate governance.

Environmental performance measures a company’s capacity to reduce environmental emissions, to efficiently use natural resources in the production processes and to support the research and development of eco-efficient products and services. Social performance measures a company’s capacity to generate trust and loyalty in its workforce, to respect the fundamental conventions on human rights, to be a good citizen, to protect public health, to respect business ethics and to create value-added products and services. Finally, corporate governance performance measures a company’s capacity to act in the best interest of its shareholders through company management systems and processes (structure and functions of the board of directors, compensation policy, etc.).

Following the literature [13,102,103,104,105,106], our study measures the level of ESG performance by calculating the arithmetic mean of the three scores: social, environmental and corporate governance. The overall ESG SCORE is expressed as a percentage ranging from 0 to 100 percent.

In an attempt to capture the impact of board characteristics on ESG performance with time for the effects to appear and lessen endogeneity problems, governance variables of any year are related to the ESG measure of the following year.

3.3. Independent Variables

The independent variables included in our econometric models are the share of women on the board of directors, share of independent directors on the board of directors, board size, number of board meetings per year and the establishment of a CSR sustainability committee. In one model, a dummy variable indicating a critical mass of women (three or more women) is controlled for.

To avoid model misspecification, we control for additional variables that could influence ESG SCORE. In line with existing literature [9,12,59], we identify the following most widely studied bank-specific control variables: bank size, return on equity (ROE) and bank leverage. We also introduce background and skills of board members to control for virtuous behaviors, which promote diversity of views, communication, collaboration, and critical debate in the decision-making process [2]. Since our banks are in different countries, we also control for the country-specific variable measuring the development level of the economy: GDP per capita based on purchasing power parity (PPP) [50,107].

3.4. Methodology

The next section will test the hypotheses regarding the effect of the board characteristics on the ESG SCORE, using panel data analysis to control for omitted/unobserved variable bias. In particular, fixed effects panel regression models are presented. The choice of fixed effects (with respect to random effects) models relies on the significant results for the Hausman tests run on all the presented specifications: in this case, fixed effects are preferable for consistency [108]. In all the model specifications, the dependent variable is ESG SCORE and all the explanatory variables are lagged by 1 year. Natural logarithmic transformations of the numerical (non index) variables (BOARD SIZE, BOARD MEET, GDP and BANK SIZE) are used to better approximate a normal distribution and overcome a possible problem of heteroskedasticity. Finally, robust standard errors of the estimated coefficients are clustered at the bank level, and year dummies and constant are included.

More specifically, the two-way fixed effects model is estimated as:

where is the dependent variable, ESG SCORE, is the constant, the vector is the variable of interest, the board characteristics, the vector is the firm-level control, the vector is the country-level control, is the fixed (bank) effect, is the year dummy and is independent disturbance, stands for the individual bank, and stands for the year. The vectors of coefficients indicated by are computed and reported (with their robust standard errors) in Tables 4 and 5.

4. Empirical Results and Discussion

4.1. Descriptive Statistics

Table 2 illustrates the descriptive statistics for both the dependent and independent variables. The descriptive statistics table includes the minimum, maximum, mean and standard deviation. The average level of ESG performance (ESG SCORE) of the banks analyzed is 61%, with a maximum equal to 100%. This reveals that the banks’ sustainability performance for the period 2011–2016 was very satisfactory by the standards of the score definition. Similarly, the board independence (the proportion of independent directors on the board) reaches an adequate average value (61%) and the maximum value is 100%, suggesting that there are banks of which board members are all independents. On the contrary, the average representation of women on boards seems still low, considering that some bank boards do not include any female directors (the minimum value is equal to zero).

Finally, it is worth noting that the average of ROE is negative: in the years following the sub-prime financial crisis (2011–2016 in our sample), banks experienced poor economic performance.

4.2. Correlation Results

The correlation matrix (Table 3) highlights very important relationships between the main variables of the study. More specifically, bank sustainability performance (ESG SCORE) is found to be positively associated with women on the board of directors, board size, CSR committee and bank size. These relationships show that more ethical and responsible banks tend to appoint more women to their boards and more frequently establish a committee dedicated solely to sustainability. Interestingly, women on the board are positively associated both with bank size and ROE, suggesting that banks of which boards are served by more female directors are larger and more profitable. Similarly, board independence is also positively related to the bank’s economic performance (ROE).

4.3. Regression Results and Discussion

Table 4 shows the estimation results of Equation (1) which can address our hypotheses relating to the impact of board composition on ESG performance of banks. Hypothesis 1 predicts that a critical mass of women on the board of directors has a positive effect on a bank’s ESG performance. In Model A (Table 4), WOMEN BOD is significant and positively related to ESG performance. However, because we embrace the critical mass theory that posits a non-linear relation between gender diversity and sustainability performance, Model B includes MASS WB (dummy variable that is equal to 1 if the board has at least three women, 0 otherwise).

When interactions are involved, the final sign of the effect of a predictor is not immediately readable from an estimation table. Indeed, computing the sum of the coefficients of WOMEN BOD and of WOMEN BOD X MASS WB results in an effect which is not significant at any conventional level (−0.017 with a robust standard error of 0.116): once the critical mass of three women is reached, an increasing share of women on the board stops exerting a positive effect on ESG SCORE. Therefore, this result does not corroborate Hypothesis 1.

In Model C, WOMEN BOD is also considered in its quadratic term to account for potential non-linearities and to endogenously determine the critical mass (threshold) in terms of proportion of female directors. The significant result confirms a functional form that is non-linear for this variable. Again, Hypothesis 1 does not seem to be confirmed: the relationship between women on the board and the extent of a bank’s sustainability performance is not U-shaped, but is an inverted U-shape. When critical mass is reached, the right branch of the parabola is not increasing.

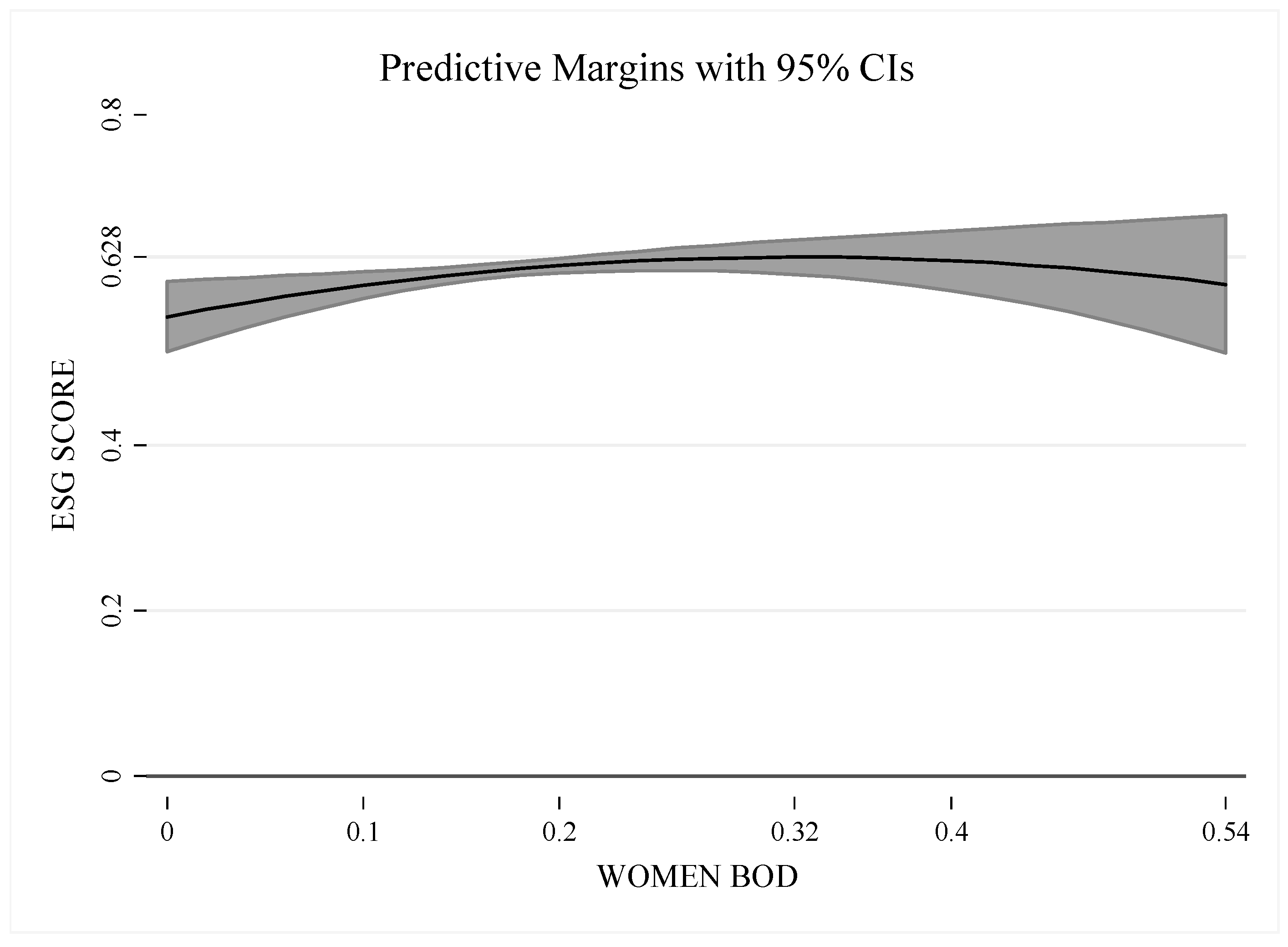

Finally, to more easily read the non-linear effect of WOMEN BOD on ESG SCORE (in Model C), Figure 1 plots the prediction and the confidence interval of ESG SCORE for different values of WOMEN BOD, for the average bank-year. Figure 1 clearly shows that the positive effect of WOMEN BOD stops after a certain proportion of female directors. In particular, after the maximum ESG SCORE reaches 32%for WOMEN BOD, the effect of WOMEN BOD is not significant, if not negative.

In summary, this result does not support the critical mass theory stricto sensu. When the number of women on a bank board reaches three or about a third of the members, including more women on the board, it has a negligible impact on the bank’s sustainability performance. This evidence appears to be in line with the findings of Schwartz-Ziv [109], who coined the “dual critical mass” expression to indicate relatively gender-balanced boards, or boards served by at least three men and three women directors. Schwartz-Ziv [109] finds that “boards with a dual critical mass are found to be at least 79% more likely to request further information or an update or to take an initiative than boards without a dual critical mass”. The conclusion is that “gender-balanced boards are more active than non-gender-balanced boards” [109] (p. 753). Indeed, gender-balanced boards facilitate information flow within the board and debate on a broader range of alternatives and novel solutions. Therefore, gender-balanced boards are associated with a higher quality of communication that in turn facilitates deliberations, enhances board function and leads to more effective problem-solving, improving the board’s strategic outlook. This is especially important when decision-makers must come to an agreement on complex issues or process complex information [110,111]. As a result, these conditions enhance a firm’s performance and corporate strategy. Accordingly, our findings confirm that gender-balanced boards prevail over unbalanced boards in terms of a bank’s ESG performance.

Hypothesis 2 predicts a relationship between independent board members and the extent of ESG performance, even though the sign is uncertain. In other words, according to existing literature, board independence can both positively and negatively impact ESG performance. Our results show a negative relationship: the coefficient related to BOARD INDEP is negative and significant in all three models (Models A, B, and C; see Table 4). This result is in line with the studies of Walls et al. [40], Haniffa and Cooke [64], Ortiz-de-Mandojana et al. [71], and Baselga-Pascual et al. [112]. It is likely that an excessive number of independent board members is self-defeating and leads to the decimation of expertise, experience and reputation provided by insiders [113], who act as critical components increasing the bank’s sustainability performance [40].

Hypothesis 3 predicts a positive relationship between board size and ESG performance. In this case, the hypothesis seems to be confirmed. In Models A and C (Table 4), BOARD SIZE is significant and positively related to ESG SCORE. Hence, consistent with correlation results (see Table 3), the econometric model indicates that financial institutions with larger boards are associated with better sustainability performance. This positive effect is broadly consistent with the findings of Baselga-Pascual et al. [112] for financial firms, and Bear et al. [26], Rao et al. [7], and Jizi [59] for non-financial firms. It is more likely that larger boards are served by directors with different skills and attitudes, including directors characterized by a strong propensity towards a culture of sustainability. Moreover, larger boards exercise oversight activities more effectively, encourage the comparison of views, a broader vision of strategic goals and also encourage management to support the non-financial performance. The Basel Committee states that “the board should be comprised of individuals with a balance of skills, diversity and expertise, who collectively possess the necessary qualifications commensurate with the size, complexity and risk profile of the bank” [2] (p. 13).

On the contrary, we reject Hypothesis 4, which predicts a positive relationship between the number of board meetings and the extent of sustainability performance. In our regression results (Models A, B and C), BOARD MEET shows a positive coefficient, but it is never significant.

Finally, Hypothesis 5 is verified very slightly: the establishment of a CSR committee seems to positively impact a bank’s ESG performance (see Table 4). According to stakeholder theory, this result confirms that a CSR committee helps banks build credibility for sustainability issues and gain legitimacy of all stakeholders. This occurs because the members of such committees have the experience, skills and knowledge specialized in CSR issues [42]. Finally, although it does not refer to the CSR committee, Basel Committee on Banking Supervision encourages banks to establish specialized board committees in order “to increase efficiency and allow deeper focus in specific areas. The number and nature of committees depend on many factors, including the size of the bank and its board, the nature of the business areas of the bank, and its risk profile” [2] (p. 16).

Regarding the control variables (see Table 4), in line with several studies, it is interesting to point out that both bank size and economic performance (ROE) have a positive and significant impact on ESG performance. These findings show that better sustainability performance is particularly achieved by larger and more profitable banks [112]. Finally, the transparency of every board member’s professional experience and skills (BACK SKILLS) is also strongly and positively connected with a bank’s sustainability performance, demonstrating that appropriate public disclosure constitutes a virtuous behavior that conforms to business ethics principles. Hence, disclosure constitutes a very ethical behavior per se. Moreover, providing this information, the bank demonstrates compliance with higher corporate governance principles for banks [2], which urge these financial intermediaries to assure their boards are served by individuals with a wide range of knowledge, experience and variety of backgrounds to promote diversity of views, higher-quality debate and to avoid a conflict of interests.

4.4. Robustness Tests

Our sample covers banks belonging to two different regions. For this reason, we conduct a robustness test to ascertain the robustness of our empirical findings and to ensure that the relationship between board composition and ESG performance is not affected by the specificity of certain regions. Therefore, we re-estimate the econometric model by splitting the sample in two sub-samples. The first sub-sample only includes U.S. banks for a total of 153 observations, while the second sub-sample only consists of European banks for a total of 253 observations. It is important to note that the variable background and skills drops out of the USA regression because of collinearity likely due to the smaller number of observations. The estimates of these additional regressions are consistent with our main analysis. The “Europe” column of Table 5 shows that the relationship between ESG performance and women directors is non-linear and that ESG performance is statistically positively connected with board size, CSR committee, background and skills, and economic performance (ROE), while board independence confirms its negative impact and number of board meetings remains not significant. Removing U.S. banks from the analysis does not affect the main results of the baseline econometric approach for the European banks. The less significant results for the American banks can be ascribed to the low number of observations (only 153) on which panel data estimation is run.

5. Conclusions

Based on prior literature demonstrating that boards play a key monitoring role in financial institutions, this study investigates the relationship between board composition (gender diversity, independence, size, activity and CSR committee) and sustainability performance in a large sample of 108 European and U.S. listed banks for the period 2011–2016.

Main findings reveal that gender diversity positively impacts a bank’s ESG performance only up to a certain threshold of women on the board. For this reason, we support the “dual critical mass” perspective [109] that emphasizes gender-balanced boards, which are boards served by a balanced number of male and female directors. In addition, other board characteristics such as board size and a CSR committee are also very important to enhancing a bank’s ESG performance. The relationship between board independence and ESG performance, on the other hand, is negative.

This study has important implications, especially for managers and regulators. From a managerial point of view, our work suggests that managers and CEOs should pay more attention to the gender diversity of their boardrooms. To enhance sustainability performance, it is important to appoint a number of women to the board and ensure gender-balanced boards. Since larger boards positively influence ESG performance, bank managers should select both male and female directors to increase board size. In addition, our study suggests the importance of establishing a CSR committee, which is a very strategic tool that demonstrates the bank’s strong commitment toward sustainability.

Our study did not investigate the composition of such a committee, but future research could go in this direction. Recent empirical evidence for non-financial firms shows that a CSR committee is more effective in improving a firm’s corporate social responsibility when it is characterized by a larger proportion of independent directors, by a female chair and a smaller size [114]. Furthermore, having a Chief Sustainability Officer (CSO), who works directly for the CEO and with the CSR committee, could represent another strategic tool for maximizing a bank’s sustainability opportunities.

For regulators, our results reveal the need to strengthen corporate governance principles for the banking sector in order to focus especially on a gender-balanced board composition and a CSR committee.

However, our study presents some limitations. First, our empirical analysis relies on the assumption that ESG performance is an effective measure of the sustainability performance for financial institutions. It would be interesting to analyze the same relationship by adopting other measures of ESG performance, like the KLD rating and/or Bloomberg ESG score. Besides, since we used data covering two developed markets (Europe and U.S.), our results cannot be extended to emerging economies. It would be interesting to use a larger sample of financial institutions and a longer window of time to examine how ESG performance is affected by board characteristics and, especially by changes in the composition of such body and its internal committees. To date, however, availability of data continues to be an issue for these investigations.

Author Contributions

This article is the result of the joint efforts of the authors, who equally contributed to the work.

Funding

Marco Savioli gratefully acknowledge financial support from the intervention co-funded by the 2007-2013 Development and Cohesion Fund—APQ Research Puglia Region “Programma regionale a sostegno della specializzazione intelligente e della sostenibilità sociale ed ambientale—FutureInResearch”.

Conflicts of Interest

The authors declare no conflict of interest.

References

- García-Sánchez, I.M.; Martánez-Ferrero, J.; García-Meca, E. Board of Directors and CSR in Banking: The Moderating Role of Bank Regulation and Investor Protection Strength. Aust. Account. Rev. 2018, 86, 428–445. [Google Scholar] [CrossRef]

- BCBS—Basel Committee on Banking Supervision, Guidelines. Corporate Governance Principles for Banks, July 2015; BCBS: Basel, Switzerland, 2015.

- HLEG—High-Level Expert Group on Sustainable Finance Financing a Sustainable European Economy, Interim Report 2017. Available online: https://ec.europa.eu/info/publications/170713-sustainable-finance-report_en (accessed on 10 January 2017).

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- HLEG—High-Level Expert Group on Sustainable Finance Financing a Sustainable European Economy, Final Report 2018. Available online: https://ec.europa.eu/info/publications/180131-sustainable-finance-report_en (accessed on 6 July 2018).

- Post, C.; Rahman, N.; Rubow, E. Green Governance: Boards of Directors’ Composition and Environmental Corporate Social Responsibility. Bus. Soc. 2011, 50, 189–223. [Google Scholar] [CrossRef]

- Rao, K.K.; Tilt, C.A.; Lester, L.H. Corporate governance and environmental reporting: An Australian study. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 143–163. [Google Scholar] [CrossRef]

- Zhang, L. Board demographic diversity, independence, and corporate social performance. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 686–700. [Google Scholar] [CrossRef]

- Setó-Pamies, D. The relationship between women directors and corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 334–345. [Google Scholar] [CrossRef]

- Kyaw, K.; Olugbode, M.; Petracci, B. Can board gender diversity promote corporate social performance? Corp. Gov. Int. J. Bus. Soc. 2017, 17, 789–802. [Google Scholar] [CrossRef] [Green Version]

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corp. Soc. Responsib. Environ. Manag. 2018, 1–19. [Google Scholar] [CrossRef]

- Helfaya, A.; Moussa, T. Do Board’s Corporate Social Responsibility Strategy and Orientation Influence Environmental Sustainability Disclosure? UK Evidence. Bus. Strategy Environ. 2017, 26, 1061–1077. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L.; Gonçalves, L.M.V. The Value Relevance of Environmental, Social, and Governance Performance: The Brazilian Case. Sustainability 2018, 10, 574. [Google Scholar] [CrossRef]

- Busch, T.; Friede, G. The Robustness of the Corporate Social and Financial Performance Relation: A Second-Order Meta-Analysis. Corp. Soc. Responsib. Environ. Manag. 2018. [Google Scholar] [CrossRef]

- Barako, D.; Brown, A. Corporate social reporting and board representation: Evidence from the Kenyan banking sector. J. Manag. Gov. 2008, 12, 309–324. [Google Scholar] [CrossRef]

- Khan, M.H.U.Z.; Halabi, A.K.; Samy, M. Corporate social responsibility (CSR] reporting: A study of selected banking companies in Bangladesh. Soc. Responsib. J. 2009, 5, 344–357. [Google Scholar] [CrossRef]

- Htay, S.N.N.; Ab Rashid, H.M.; Adnan, M.A.; Meera, A.K.M. Impact of corporate governance on social and environmental information disclosure of Malaysian listed banks: Panel data analysis. Asian J. Financ. Account. 2012, 4, 1. [Google Scholar] [CrossRef]

- Jizi, M.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef]

- Kiliç, M.; Kuzey, C.; Uyar, A. The impact of ownership and board structure on Corporate Social Responsibility (CSR] reporting in the Turkish banking industry. Corp. Gov. Int. J. Bus. Soc. 2015, 15, 357–374. [Google Scholar] [CrossRef]

- Kanter, R. Some effects of proportions on group life: Skewed sex ratios and responses to token women. Am. J. Sociol. 1977, 82, 965–990. [Google Scholar] [CrossRef]

- Kramer, V.W.; Konrad, A.M.; Erkut, S. Critical Mass on Corporate Boards: Why Three or More Women Enhance Governance. (Wellesley Centers for Women, Report No. WCW 11); Wellesley Centers for Women: Wellesley, MA, USA, 2006; Available online: http://www.wcwonline.org/pubs/title.php?id=487 (accessed on 10 August 2017).

- Konrad, A.M.; Kramer, V.; Erkut, S. Critical mass: The impact of three or more women on corporate boards. Organ. Dyn. 2008, 37, 145–164. [Google Scholar] [CrossRef]

- Joecks, J.; Pull, K.; Vetter, K. Gender Diversity in the Boardroom and Firm Performance: What Exactly Constitutes a “Critical Mass?”. J. Bus. Ethics 2013, 118, 61–72. [Google Scholar] [CrossRef]

- Farag, H.; Mallin, C. Board diversity and financial fragility: Evidence from European banks. Int. Rev. Financ. Anal. 2017, 49, 98–112. [Google Scholar] [CrossRef]

- Williams, R. Women on corporate boards of directors and their influence on corporate philanthropy. J. Bus. Ethics 2003, 42, 1–10. [Google Scholar] [CrossRef]

- Bear, S.; Rahman, N.; Post, C. The impact of board diversity and gender composition on corporate social responsibility and firm reputation. J. Bus. Ethics 2010, 97, 207–221. [Google Scholar] [CrossRef]

- Eagly, A.H.; Johannesen-Schmidt, M.C.; van Engen, M.L. Transformational, transactional, and laissez–faire leadership styles: A meta-analysis comparing women and men. Psychol. Bull. 2003, 129, 569–591. [Google Scholar] [CrossRef] [PubMed]

- Zhang, J.Q.; Zhu, H.; Ding, H. Board composition and corporate social responsibility: An empirical investigation in the post Sarbanes–Oxley era. J. Bus. Ethics 2013, 114, 381–392. [Google Scholar] [CrossRef]

- Nielsen, S.; Huse, M. The contribution of women on boards of directors: Going beyond the surface. Corp. Gov. Int. Rev. 2010, 18, 136–148. [Google Scholar] [CrossRef]

- Wang, J.; Coffey, B. Board composition and corporate philanthropy. J. Bus. Ethics 1992, 11, 771–778. [Google Scholar] [CrossRef]

- Ciocirlan, C.; Pettersson, C. Does workforce diversity matter in the fight against climate change? An analysis of Fortune 500 companies. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 47–62. [Google Scholar] [CrossRef]

- Rupley, K.H.; Brown, D.; Marshall, R.S. Governance, media, and the quality of environmental disclosure. J. Account. Public Policy 2012, 31, 610–640. [Google Scholar] [CrossRef]

- Cabeza-García, L.; Fernández-Gago, R.; Matilla, L. Análisis de los determinantes de la transparencia en RSC desde la perspectiva del buen gobierno. Ekon. Rev. Vasca Econ. 2013, 83, 273–296. [Google Scholar]

- García-Sánchez, I.M.; Cuadrado–Ballesteros, B.; Sepulveda, C. Does media pressure moderate CSR disclosures by external directors? Manag. Decis. 2014, 52, 1014–1045. [Google Scholar] [CrossRef]

- Lone, E.J.; Amjad, A.; Khan, I. Corporate governance and corporate social responsibility disclosure: Evidence from Pakistan. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 787–797. [Google Scholar] [CrossRef]

- Sundarasen, S.D.D.; Je-Yen, T.; Rajangam, N. Board composition and corporate social responsibility in an emerging market. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 79–95. [Google Scholar] [CrossRef]

- Liu, C. Are women greener? Corporate gender diversity and environmental violations. J. Corp. Financ. 2018, 52, 118–142. [Google Scholar] [CrossRef]

- Glass, C.; Cook, A.; Ingersoll, A.R. Do Women Leaders Promote Sustainability? Analyzing the Effect of Corporate Governance Composition on Environmental Performance. Bus. Strategy Environ. 2016, 25, 495–511. [Google Scholar] [CrossRef]

- Khan, M.H.U.Z. The effect of corporate governance elements on corporate social responsibility (CSR] reporting: Empirical evidence from private commercial banks of Bangladesh. Int. J. Law Manag. 2010, 52, 82–109. [Google Scholar] [CrossRef]

- Walls, J.L.; Berrone, P.; Phan, P.H. Corporate governance and environmental performance: Is there really a link? Strateg. Manag. J. 2012, 33, 885–913. [Google Scholar] [CrossRef]

- Mallin, C.A.; Michelon, G.; Raggi, D. Monitoring intensity and stakeholders’ orientation: How does governance affect social and environmental disclosure? J. Bus. Ethics 2013, 114, 29–43. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Bus. Strategy Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Alazzani, A.; Hassanein, A.; Aljanadi, Y. Impact of gender diversity on social and environmental performance: Evidence from Malaysia. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 266–283. [Google Scholar] [CrossRef]

- Prado-Lorenzo, J.M.; García-Sánchez, I.M.; Gallego-Alvarez, I. Características del consejo de administración e información en materia de responsabilidad social corporativa. Rev. Esp. Financ. Contab. 2009, 141, 107–135. [Google Scholar]

- Deschênes, S.; Rojas, M.; Boubacar, H.; Prud’homme, B.; Ouedraogo, A. The impact of board traits on the social performance of Canadian firms. Corp. Gov. Int. Rev. 2015, 15, 293–305. [Google Scholar] [CrossRef]

- Grey, S. Does Size Matter? Critical Mass and New Zealand’s Women MPs’. Parliam. Aff. 2002, 55, 19–29. [Google Scholar] [CrossRef]

- Childs, S.; Krook, M.L. Critical Mass Theory and Women’s Political Representation. Political Stud. 2008, 56, 725–736. [Google Scholar] [CrossRef]

- Boulouta, I. Hidden connections: The link between board gender diversity and corporate social performance. J. Bus. Ethics 2013, 113, 185–197. [Google Scholar] [CrossRef]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Does board gender composition affect corporate social responsibility reporting? Int. J. Bus. Soc. Sci. 2012, 3, 31–38. [Google Scholar]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz-Blanco, S. Women on boards: Do they affect sustainability reporting? Corp. Soc. Responsib. Environ. Manag. 2014, 21, 351–364. [Google Scholar] [CrossRef]

- Cabeza-García, L.; Fernández-Gago, R.; Nieto, M. Do Board Gender Diversity and Director Typology Impact CSR Reporting? Eur. Manag. Rev. 2017. [Google Scholar] [CrossRef]

- Manita, R.; Bruna, M.G.; Dang, R.; Houanti, L.H. Board gender diversity and ESG disclosure: Evidence from the USA. J. Appl. Account. Res. 2018, 19, 206–224. [Google Scholar] [CrossRef]

- Ben-Amar, W.; Chang, M.; McIlkenny, P. Board Gender Diversity and Corporate Response to Sustainability Initiatives: Evidence from the Carbon Disclosure Project. J. Bus. Ethics 2017, 142, 369–383. [Google Scholar] [CrossRef]

- Shoham, A.; Almor, T.; Lee, S.M.; Ahammad, M.F. Encouraging environmental sustainability through gender: A micro-foundational approach using linguistic gender marking. J. Organ. Behav. 2017, 38, 1356–1379. [Google Scholar] [CrossRef]

- Liu, Y.; Wei, Z.; Xie, F. Do women directors improve firm performance in China? J. Corp. Financ. 2014, 28, 169–184. [Google Scholar] [CrossRef]

- Owen, A.L.; Temesvary, J. The performance effects of gender diversity on bank boards. J. Bank. Financ. 2018, 90, 50–63. [Google Scholar] [CrossRef] [Green Version]

- Cucari, N.; De Falco, E.S.; Orlando, B. Diversity of Board of Directors and Environmental Social Governance: Evidence from Italian Listed Companies. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 250–266. [Google Scholar] [CrossRef]

- Ortas, E.; Álvarez, I.; Zubeltzu, E. Firms’ Board Independence and Corporate Social Performance: A Meta-Analysis. Sustainability 2017, 9, 1006. [Google Scholar] [CrossRef]

- Jizi, M. The Influence of Board Composition on Sustainable Development Disclosure. Bus. Strategy Environ. 2017, 26, 640–655. [Google Scholar] [CrossRef]

- Ahmed, K.; Hossain, M.; Adams, M.B. The effects of board composition and board size on the informativeness of annual accounting earnings. Corp. Gov. Int. Rev. 2006, 14, 418–431. [Google Scholar] [CrossRef]

- Cheng, E.C.M.; Courtenay, S.M. Board composition, regulatory regime and voluntary disclosure. Int. J. Account. 2006, 41, 262–289. [Google Scholar] [CrossRef]

- Ibrahim, N.A.; Howard, D.P.; Angelidis, J.P. Board members in the service industry: An empirical examination of the relationship between corporate social responsibility orientation and directorial type. J. Bus. Ethics 2003, 47, 393–401. [Google Scholar] [CrossRef]

- Chau, G.; Gray, S.J. Family ownership, board independence and voluntary disclosure: Evidence from Hong Kong. J. Int. Account. Audit. Tax. 2010, 19, 93–109. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef] [Green Version]

- Lim, S.; Matolcsy, Z.; Chow, D. The association between board composition and different types of voluntary disclosure. Eur. Account. Rev. 2007, 16, 555–583. [Google Scholar] [CrossRef]

- Nurhayati, R.; Taylor, G.; Tower, G. Investigating social and environmental disclosure practices by listed Indian textile firms. J. Dev. Areas 2015, 49, 361–372. [Google Scholar] [CrossRef]

- Walls, J.L.; Hoffman, A.J. Exceptional boards: Environmental experience and positive deviance from institutional norms. J. Organ. Behav. 2013, 34, 253–271. [Google Scholar] [CrossRef]

- Benomran, N.A.; Haat, M.H.C.; Hashim, H.B.; Mohamad, N.R.B. Influence of Corporate Governance on the Extent of Corporate Social Responsibility and Environmental Reporting. J. Environ. Ecol. 2015, 6, 48–68. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C.A. Board diversity and CSR reporting: An Australian study. Med. Account. Res. 2016, 24, 182–210. [Google Scholar] [CrossRef]

- Walls, J.L.; Berrone, P. The Power of One to Make a Difference: How Informal and Formal CEO Power Affect Environmental Sustainability. J. Bus. Ethics 2017, 145, 293–308. [Google Scholar] [CrossRef]

- Ortiz-de-Mandojana, N.; Aguilera-Caracuel, J.; Morales-Raya, M. Corporate Governance and Environmental Sustainability: The Moderating Role of the National Institutional Context. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 150–164. [Google Scholar] [CrossRef]

- Hossain, M.; Reaz, M. The Determinants and Characteristics of Voluntary Disclosure by Indian Banking Companies. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 274–288. [Google Scholar] [CrossRef]

- Jensen, M.C. The modern industrial revolution, exit, and the failure of internal control mechanisms. J. Financ. 1993, 6, 831–880. [Google Scholar] [CrossRef]

- De Andres, P.; Azofra, V.; Lopez, F. Corporate Boards in OECD Countries: Size, composition, functioning and effectiveness. Corp. Gov. Int. Rev. 2005, 13, 197–210. [Google Scholar] [CrossRef]

- Dey, A. Corporate governance and agency conflicts. J. Account. Res. 2008, 46, 1143–1181. [Google Scholar] [CrossRef]

- Laksmana, I. Corporate board governance and voluntary disclosure of executive compensation practices. Contemp. Account. Res. 2008, 25, 1147–1182. [Google Scholar] [CrossRef]

- Guest, P.M. The impact of board size on firm performance: Evidence from the UK. Eur. J. Financ. 2009, 15, 385–404. [Google Scholar] [CrossRef]

- John, K.; Senbet, L.W. Corporate governance and board effectiveness. J. Bank. Financ. 1998, 22, 371–403. [Google Scholar] [CrossRef] [Green Version]

- Beiner, S.; Drobetz, W.; Schmid, F.; Zimmermann, H. Is board size an independent corporate governance mechanism? Kyklos 2004, 57, 327–356. [Google Scholar] [CrossRef]

- Larmou, S.; Vafeas, N. The relation between board size and firm performance in firm with a history of poor operating performance. J. Manag. Gov. 2010, 14, 61–85. [Google Scholar] [CrossRef]

- Krishnan, G.; Visvanathan, G. Do auditors price audit committee’s expertise? The case of accounting versus non-accounting financial experts. J. Account. Audit. Financ. 2009, 24, 115–144. [Google Scholar] [CrossRef]

- Pathan, S. Strong boards, CEO power and bank risk-taking. J. Bank. Financ. 2009, 33, 1340–1350. [Google Scholar] [CrossRef]

- Akhtaruddin, M.; Hossain, M.A.; Hossain, M.; Yao, L. Corporate governance and voluntary disclosure in corporate annual reports of Malaysian listed firms. J. Appl. Manag. Account. Res. 2009, 7, 1–19. [Google Scholar]

- Said, R.; Hj Zainuddin, Y.; Haron, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef]

- Esa, E.; Mohd Ghazali, N.A. Corporate social responsibility and corporate governance in Malaysian government-linked companies. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 292–305. [Google Scholar] [CrossRef]

- Ntim, C.G.; Soobaroyen, T. Corporate Governance and Performance in Socially Responsible Corporations: New Empirical Insights from a Neo-Institutional Framework. Corp. Gov. Int. Rev. 2013, 21, 468–494. [Google Scholar] [CrossRef] [Green Version]

- Arena, C.; Bozzolan, S.; Michelon, G. Environmental reporting: Transparency to stakeholders or stakeholder manipulation? An analysis of disclosure tone and the role of the board of directors. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 346–361. [Google Scholar] [CrossRef]

- Vafeas, N. Board meeting frequency and firm performance. J. Financ. Econ. 1999, 53, 113–142. [Google Scholar] [CrossRef]

- Dienes, D.; Velte, P. The Impact of Supervisory Board Composition on CSR Reporting. Evidence from the German Two-Tier System. Sustainability 2016, 8, 63. [Google Scholar] [CrossRef]

- Lipton, M.; Lorsch, J. A modest proposal for improved corporate governance. Bus. Lawyer 1992, 48, 59–77. [Google Scholar]

- Conger, J.; Finegold, D.; Lawler, E., III. Appraising Boardroom Performance. Harv. Bus. Rev. 1998, 76, 136–148. [Google Scholar]

- Ricart, J.E.; Rodríguez, M.Á.; Sánchez, P. Sustainability in the boardroom: An empirical examination of Dow Jones Sustainability World Index leaders. Corp. Gov. Int. J. Bus. Soc. 2005, 5, 24–41. [Google Scholar] [CrossRef]

- Adawi, M.; Rwegasira, K. Corporate boards and voluntary implementation of best disclosure practices in emerging markets: Evidence from the UAE listed companies in the Middle East. Int. J. Discl. Gov. 2011, 8, 272–293. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does Corporate Governance Affect Sustainability Disclosure? A Mixed Methods Study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Liao, L.; Luo, L.; Tang, Q. Gender diversity, board independence, environmental committee and greenhouse gas disclosure. Br. Account. Rev. 2015, 47, 409–424. [Google Scholar] [CrossRef]

- Ullman, A.H. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance of US firms. Acad. Manag. Rev. 1985, 10, 540–557. [Google Scholar]

- Adnan, S.M.; Van Staden, C.; Hay, D. Do culture and governance structure influence CSR reporting quality: Evidence from China, India, Malaysia and the United Kingdom. In Proceedings of the 6th Asia Pacific Interdisciplinary Research in Accounting Conference, Sydney, Australia, 12–13 July 2010. [Google Scholar]

- Spitzeck, H. The development of governance structures for corporate responsibility. Corp. Gov. Int. J. Bus. Soc. 2009, 9, 495–505. [Google Scholar] [CrossRef]

- Michelon, G.; Parbonetti, A. The effect of corporate governance on sustainability disclosure. J. Manag. Gov. 2012, 16, 477–509. [Google Scholar] [CrossRef]

- Pätäri, S.; Jantunen, A.; Kyläheiko, K.; Sandström, J. Does sustainable development foster value creation? Empirical evidence from the global energy industry. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 317–326. [Google Scholar] [CrossRef]

- Ferrero-Ferrero, I.; Fernández-Izquierdo, M.A.; Muñoz-Torres, M.J. The effect of the environmental, social and governance consistency on economic results. Sustainability 2016, 8, 1005. [Google Scholar] [CrossRef]

- Kassinis, G.; Panayiotou, A.; Dimou, A.; Katsifaraki, G. Gender and Environmental Sustainability: A Longitudinal Analysis. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 399–412. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Giannarakis, G.; Konteos, G.; Sariannidis, N. Financial, governance and environmental determinants of corporate social responsible disclosure. Manag. Decis. 2014, 52, 1928–1951. [Google Scholar] [CrossRef]

- Mervelskemper, L.; Streit, D. Enhancing market valuation of ESG performance: Is integrated reporting keeping its promise? Bus. Strategy Environ. 2017, 26, 536–549. [Google Scholar] [CrossRef]

- Hu, V.I.; Scholtens, B. Corporate social responsibility policies of commercial banks in developing countries. J. Sustain. Dev. 2014, 22, 276–288. [Google Scholar] [CrossRef]

- Baltagi, B.H. Econometrics, 5th ed.; Springer: Berlin, Germany, 2011. [Google Scholar]

- Schwartz-Ziv, M. Gender and Board Activeness: The Role of a Critical Mass. J. Financ. Quant. Anal. 2017, 52, 751–780. [Google Scholar] [CrossRef] [Green Version]

- Van Knippenberg, D.; De Dreu, C.K.W.; Homan, A.C. Work group diversity and group performance: An integrative model and research agenda. J. Appl. Psychol. 2004, 89, 1008–1022. [Google Scholar] [CrossRef]

- Glass, C.; Cook, A. Do Women Leaders Promote Positive Change? Analyzing the Effect of Gender on Business Practices and Diversity Initiatives. Hum. Resour. Manag. 2017. [Google Scholar] [CrossRef]

- Baselga-Pascual, L.; Trujillo-Ponce, A.; Vähämaa, E.; Vähämaa, S. Ethical Reputation of Financial Institutions: Do Board Characteristics Matter? J. Bus. Ethics 2018, 148, 489–510. [Google Scholar] [CrossRef]

- Dalton, D.R.; Hitt, M.A.; Certo, S.T.; Dalton, C.M. The fundamental agency problem and its mitigation. Acad. Manag. Ann. 2007, 1, 1–64. [Google Scholar] [CrossRef]

- Eberhardt-Toth, E. Who should be on a board corporate social responsibility committee? J. Clean. Prod. 2017, 140, 1926–1935. [Google Scholar] [CrossRef]

Figure 1.

Predictions and confidence intervals of ESG SCORE (Model C) as a function of WOMEN BOD. This figure shows the prediction and the confidence interval of ESG SCORE (Model C) for each value of WOMEN BOD for the average bank-year. Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

Figure 1.

Predictions and confidence intervals of ESG SCORE (Model C) as a function of WOMEN BOD. This figure shows the prediction and the confidence interval of ESG SCORE (Model C) for each value of WOMEN BOD for the average bank-year. Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

{kind=link}

Table 1.

Independent variables.

| Name of Variable (Acronym) | Measurement | Expected Relationship with ESG SCORE | Sources |

|---|---|---|---|

| Women on the board of directors (WOMEN BOD) | Total number of women on the board of directors divided by the total number of board members | Non-linear | Rao et al. [7] Barako and Brown [15] Rupley et al. [32] |

| Critical mass of women on the board of directors (MASS WB) | Dummy variable that is equal to 1 if boards have at least three women, 0 otherwise | Positive | Post et al. [6] Fernandez-Feijoo et al. [49,50] Liu [37] Ben-Amar et al. [53] Shoham et al. [54] |

| Board independence (BOARD INDEP) | Percentage of independent board members divided by the total number of board members | Positive/Negative | Ahmed et al. [60] Chau and Gray [63] Lim et al. [65] |

| Board size (BOARD SIZE) | Total number of directors on the bank’s board | Positive | Jensen [73] De Andres et al. [74] Laksmana [76] |

| Board meetings (BOARD MEET) | Number of board meetings per year | Positive | Laksmana [76] Lipton and Lorsch [90] Conger et al. [91] |

| CSR sustainability committee (CSR COM) | Dummy variable that is equal to 1 if the bank has a CSR sustainability committee, 0 otherwise | Positive | Hussain et al. [94] Liao et al. [96] |

| Background and skills (BACK SKILLS) | Dummy variable that is equal to 1 if the bank describes the professional experience or skills of every board member or provides information about the age of individual board members, 0 otherwise | Positive | BCBS [2] |

| Bank size (BANK SIZE) | Total assets (Euro) of the bank | Positive | Setó-Pamies [9] Helfaya and Moussa [12] |

| Return on equity (ROE) | Bank’s net income divided by the value of its total shareholders’ equity | Positive/Negative | Setó-Pamies [9] Helfaya and Moussa [12] |

| Leverage (LEV) | Tier 1 Capital as percentage of total assets (proxy for the Basel 3 leverage ratio) | Positive | Helfaya and Moussa [12] |

| GDP per capita, PPP (GDP) | Gross Domestic Product (GDP) per capita based on purchasing power parity (PPP) | Positive/Negative | Fernandez-Feijoo et al. [50] Hu and Scholtens [107] |

Table 2.

Summary statistics of ESG SCORE and explanatory variables.

| Variable | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|

| ESG SCORE | 0.608 | 0.237 | 0.097 | 1 |

| WOMEN BOD | 0.197 | 0.111 | 0 | 0.540 |

| MASS WB | 0.493 | 0.501 | 0 | 1 |

| BOARD INDEP | 0.609 | 0.273 | 0 | 1 |

| BOARD SIZE | 14.148 | 4.674 | 6 | 30 |

| BOARD MEET | 12.406 | 6.587 | 4 | 60 |

| CSR COMM | 0.594 | 0.492 | 0 | 1 |

| BACK SKILLS | 0.842 | 0.365 | 0 | 1 |

| BANK SIZE | 320,200,000 | 515,500,000 | 1,093,000 | 2,211,000,000 |

| ROE | −0.009 | 0.577 | −6.873 | 0.356 |

| LEV | 0.076 | 0.032 | 0.015 | 0.216 |

| GDP | 44,902.697 | 10,444.942 | 22,729.184 | 67,974.164 |

This table shows the summary statistics of ESG SCORE and explanatory variables. The number of bank-year observations is 406 for all the variables. The variables MASS WB, BACK SKILLS and CSR COMM are dummy variables. Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

Table 3.

Correlation matrix.

| Variable | ESG SCORE | WOMEN BOD | MASS WB | BOARD INDEP | BOARD SIZE | BOARD MEET | CSR COMM | BACK SKILLS | BANK SIZE | ROE | LEV | GDP |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ESG SCORE | 1 | |||||||||||

| WOMEN BOD | 0.47 *** | 1 | ||||||||||

| MASS WB | 0.47 *** | 0.72 *** | 1 | |||||||||

| BOARD INDEP | −0.01 | 0.11 ** | 0.01 | 1 | ||||||||

| BOARD SIZE | 0.19 *** | −0.07 | 0.30 *** | −0.27 *** | 1 | |||||||

| BOARD MEET | 0.02 | −0.06 | −0.04 | −0.10 ** | 0.08 | 1 | ||||||

| CSR COMM | 0.66 *** | 0.32 *** | 0.30 *** | −0.04 | 0.15 *** | 0.06 | 1 | |||||

| BACK SKILLS | −0.08 * | 0.03 | −0.16 *** | 0.31 *** | −0.47 *** | −0.31 *** | −0.14 *** | 1 | ||||

| BANK SIZE | 0.56 *** | 0.44 *** | 0.39 *** | 0.07 | 0.13 *** | −0.02 | 0.43 *** | 0.05 | 1 | |||

| ROE | 0.01 | 0.11 ** | 0.08 | 0.12 ** | −0.11 ** | −0.26 *** | −0.06 | 0.22 *** | 0.004 | 1 | ||

| LEV | 0.22 *** | −0.15 *** | −0.19 *** | 0.36 *** | −0.21 *** | −0.13 ** | −0.32 *** | 0.22 *** | −0.36 *** | 0.21 *** | 1 | |

| GDP | −0.21 *** | 0.12 ** | −0.06 | 0.45 *** | −0.42 *** | −0.24 *** | −0.15 *** | 0.44 *** | −0.07 | 0.17 *** | 0.17 *** | 1 |

Significant correlation coefficients are indicated by the usual significance levels: ***, 1%; **, 5%; *, 10%. Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

Table 4.

Fixed effects panel regression models of ESG SCORE.

| Model | (A) | (B) | (C) |

|---|---|---|---|

| Coefficient (Robust SE) | Coefficient (Robust SE) | Coefficient (Robust SE) | |

| WOMEN BOD (lag) | 0.166 * (0.089) | 0.298 ** (0.140) | 0.446 ** (0.184) |

| MASS WB (lag) | 0.073 * (0.038) | ||

| WOMEN BOD X MASS WB (lag) | −0.315 * (0.161) | ||

| WOMEN BOD ^2 (lag) | −0.693 * (0.361) | ||

| BOARD INDEP (lag) | −0.055 * (0.030) | −0.059 ** (0.029) | −0.062 ** (0.030) |

| BOARD SIZE (lag, log) | 0.076 ** (0.038) | 0.053 (0.036) | 0.066 * (0.036) |

| BOARD MEET (lag, log) | 0.013 (0.017) | 0.013 (0.016) | 0.012 (0.016) |

| CSR COMM (lag) | 0.033 (0.022) | 0.038 * (0.022) | 0.036 * (0.022) |

| BACK SKILLS ((lag) | 0.033 ** (0. 014) | 0.035 *** (0. 013) | 0.035 ** (0. 014) |

| BANK SIZE (lag, log) | 0.110 *** (0.037) | 0.115 *** (0.037) | 0.113 *** (0.038) |

| ROE (lag) | 0.014 *** (0.005) | 0.014 *** (0.005) | 0.015 *** (0.005) |

| LEV (lag) | 0.390 (0.739) | 0.409 (0.753) | 0.333 (0.741) |

| GDP (lag, log) | 0.014 (0.151) | 0.009 (0.137) | 0.005 (0.147) |

| Observations | 406 | 406 | 406 |

| Groups | 108 | 108 | 108 |

| Year dummies χ2 | 10.39 *** | 9.48 *** | 9.28 *** |

| RegressionF | 18.71 *** | 15.67 *** | 17.31 *** |

Fixed effects panel regressions: the dependent variable is ESG SCORE; all the explanatory variables are lagged by 1 year (lag); natural logarithmic transformations of BOARD SIZE, BOARD MEET, GDP and BANK SIZE are used (log); the robust standard errors of the estimated coefficients reported in parentheses are clustered at the bank level. All the model specifications include year dummies and a constant (not reported for brevity) and have 1% significant Hausman test pointing to the fixed effects (within) estimations. The usual significance levels for the tests of the reported coefficients statistically different from zero are: ***, 1%; **, 5%; *, 10%. Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

Table 5.

Fixed effects panel regression models of ESG SCORE by geographic area.

| Model | (All) | (US) | (Europe) |

|---|---|---|---|

| Coefficient (Robust SE) | Coefficient (Robust SE) | Coefficient (Robust SE) | |

| WOMEN BOD (lag) | 0.446 ** (0.184) | 0.357 (0.228) | 0.552 *** (0.189) |

| WOMEN BOD^2 (lag) | −0.693 * (0.361) | −0.481 (0.457) | −0.664 * (0.365) |

| BOARD INDEP (lag) | −0.062 ** (0.030) | −0.007 (0.027) | −0.110 *** (0.033) |

| BOARD SIZE (lag, log) | 0.066 * (0.036) | 0.008 (0.03) | 0.114 ** (0.047) |

| BOARD MEET (lag, log) | 0.012 (0.016) | −0.016 (0. 010) | 0.032 (0.021) |

| CSR COMM (lag) | 0.036 * (0.022) | −0.027 (0.019) | 0.049 ** (0.022) |

| BACK SKILLS (lag) | 0.035 ** (0.014) | - | 0.043 *** (0.016) |

| BANK SIZE (lag, log) | 0.113 *** (0.038) | 0.023 (0.059) | −0.039 (0.066) |

| ROE (lag) | 0.015 *** (0.005) | 0.073 (0.068) | 0.019 *** (0.005) |

| LEV (lag) | 0.333 (0.741) | −0.348 (0.751) | 0.189 (1.085) |

| GDP (lag, log) | 0.005 (0.147) | 13.944 *** (2.775) | −0.004 (0.150) |

| Observations | 406 | 153 | 253 |

| Groups | 108 | 42 | 66 |

| Year dummies χ * | 9.28 *** | 15.44 *** | 4.63 *** |

| Regression F | 17.31 *** | 166.30 *** | 6.94 *** |

Fixed effects panel regressions: the dependent variable is ESG SCORE; all the explanatory variables are lagged by 1 year (lag); natural logarithmic transformations of BOARD SIZE, BOARD MEET, GDP and BANK SIZE are used (log); BACK SKILLS drops out from the USA regression because of collinearity; the robust standard errors of the estimated coefficients reported in parentheses are clustered at the bank level. All the model specifications include year dummies and a constant (not reported for brevity) and have 1% significant Hausman test pointing to the fixed effects (within) estimations. The usual significance levels for the tests of the reported coefficients statistically different from zero are: ***, 1%; **, 5%; *, 10%). Data source: Asset4 Thomson Reuters, The World Bank and Datastream.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Birindelli, G.; Dell’Atti, S.; Iannuzzi, A.P.; Savioli, M. Composition and Activity of the Board of Directors: Impact on ESG Performance in the Banking System. Sustainability 2018, 10, 4699. https://doi.org/10.3390/su10124699

AMA Style

Birindelli G, Dell’Atti S, Iannuzzi AP, Savioli M. Composition and Activity of the Board of Directors: Impact on ESG Performance in the Banking System. Sustainability. 2018; 10(12):4699. https://doi.org/10.3390/su10124699

Chicago/Turabian StyleBirindelli, Giuliana, Stefano Dell’Atti, Antonia Patrizia Iannuzzi, and Marco Savioli. 2018. "Composition and Activity of the Board of Directors: Impact on ESG Performance in the Banking System" Sustainability 10, no. 12: 4699. https://doi.org/10.3390/su10124699

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.