Trade Credit as a Sustainable Resource during an SME’s Life Cycle

Departamento de Economía Financiera y Dirección de Operaciones, Universidad de Sevilla, 41018 Sevilla, España

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(3), 670; https://doi.org/10.3390/su11030670

Submission received: 25 December 2018

/

Revised: 23 January 2019

/

Accepted: 24 January 2019

/

Published: 28 January 2019

(This article belongs to the Special Issue Sustainable Finance)

Abstract

:Inadequate access to finance for small and medium-sized enterprises (SMEs) can present a major impediment to SMEs’ contribution towards driving sustainable economic growth. The aim of this article is to investigate the role of life cycle on SME financing decisions while focusing on trade credit. To this end, we study whether trade credit and its firm-factor determinants differ depending on the stage of life cycle of the SMEs. For the empirical analysis, a sample is employed of manufacturing SMEs operating in 12 European Union countries over the period 2008–2014 and a panel data model with fixed effects is applied. We find that the business life cycle influences trade credit and that this influence is stronger in young firms, although this relation is non-linear across the firms’ life cycle. We further show that the impact of firm-factor determinants on trade credit differs across the business life cycle in terms of magnitude levels. Our results demonstrate that the business life cycle matters when analysing trade credit, and it should therefore be considered when managers and policymakers strive to solve the financial problems of an SME and to consequently incorporate the SME into the sustainable economy.

1. Introduction

Small and medium-sized enterprises (SMEs) form the backbone of most national economies around the world [1]. In the European Union (EU), they represent 99% of all businesses [2]. These constitute a vital ingredient for the success of the economy and for the adaption of new trends, such as sustainable growth. However, SMEs face serious difficulties in accessing sustainable finance, both via banks and financial markets. It is worthy of note that smaller businesses have reduced access to financial markets [3], and they suffer more restrictions regarding credit [4]. These limitations are exacerbated in the particular case of sustainable finance due to insufficient regulation and knowledge, and implementation of sustainability criteria by SMEs [5]. Consequently, the contribution of SMEs towards driving sustainable growth of economies, such as the EU, can be limited due to this financial restriction.

Trade credit is one of the largest sources of finance for SMEs. In the European Union, trade credit amounts to an estimated 30% of GDP [1], and more specifically in EU SMEs, trade credit is the primary resource after sources through financial intermediaries (Survey on the Access to Finance of EU enterprises (SAFE)). Therefore, trade credit in SMEs could play, from the start, a major role in the provision of finance for investment, by taking into account environmental, social, and governance appreciations, since suppliers can promote sustainability considerations in the supply chain of their customers at the same time as they collaborate in their financing, by offering advantages and incentives through terms and payment conditions [6].

Clearly, trade credit as a sustainable resource is crucial to small businesses, but is trade credit equally important throughout the entire life cycle of SMEs? [7], in one of the first and most relevant studies on the interconnectedness of SME capital structure and age, show that the stage of the life cycle of the company determines the nature of its financial needs and the availability of financial resources. The financial literature has evidenced that firms in the earlier stages of their life cycles are characterized by having larger levels of asymmetric information, more growth opportunities, and are smaller in size, and therefore face different financing choices to those of older firms. Hence, we may conjecture that firms will tend to adopt specific financing strategies as they progress along the phases of their life cycle [8,9,10,11]. From this perspective, trade credit is present at all stages of the business life cycle in SMEs in order to enable these firms to start up, develop, and grow [7]; another key issue involves the required level of trade credit in each of these stages.

To the best of our knowledge, the empirical literature on trade credit is characterized by only a few papers that explicitly analyze the impact of the life cycle of SMEs on supplier financing despite its critical nature. This evidence on trade credit usually introduces the life cycle with the firm-age variable and follows one of two approaches. First and foremost, there is a linear approach, in which differences such as those in reputation, and opacity between young companies and older companies, should explain the various degrees of trade credit between young SMEs and older SMEs. The results of this evidence worldwide are of a mixed nature. From among this evidence, that which was carried out on European SMEs draws particular interest because studies that analyze similar areas have shown divergent results. While Casey and O’Toole [12] observe a positive effect of age on trade credit, Andrieu et al. [13] and Yazdanfar and Öhman [14] show no significant effect of age, and Deloof and La Rocca [15] and Canto-Cuevas et al. [16], among others, find a negative effect of age. Secondly, there is a non-linear approach, in which the empirical evidence strives to examine whether the relationship between trade credit and age is non-linear. The results of this sparse evidence in SMEs across the globe are even less conclusive than the previous approach. For the particular case of European countries, the divergences are also shown. While García-Teruel and Martínez-Solano [17] observe a non-linear relationship between trade credit and age, McGuinness et al. [18] show no such non-linear relationship. To sum up, the literature regarding the relationship between trade credit and business life cycle shows that it has hitherto proved very difficult to determine the precise way firm age influences the use of trade credit [19], and therefore further investigations are necessary into this issue.

Our study has the major advantage of overcoming one of the limitations of the previous literature on trade credit, that is, the relationship between the life cycle and the use of trade credit may differ based on the type of SMEs analyzed [7,14,19]. Previous empirical research, however, has largely failed to take this heterogeneity into account. Specifically, it has been observed that the business sector is extremely important in the financing decisions of SMEs, including trade credit [14,20,21,22]. Moreover, it has been found that the use of trade credit varies considerably across industries but that the variation remains small within each industry, and therefore the determinants of trade credit could also differ depending on the sector [23,24,25]. This leads us to consider a homogeneous type of firm within a sole sector—that of manufacturing—in which trade credit plays a preponderant role in financing companies and presents particular characteristics [12,26].

The aim of our study is to delve into the understanding of trade credit using the perspective of an SME’s life cycle while focusing on the manufacturing business sector. In this analysis, we strive to verify the following: first, whether the life cycle is a relevant factor in trade credit decisions; second, how trade credit varies during the different stages of the life cycle; and third, how firm-factor determinants of trade credit change throughout the life cycle. Our empirical analysis uses a sample of manufacturing SMEs in the European Union over the period 2008–2014. Thanks to this sample, it will be easier to identify and to explain the role of life cycle on trade credit.

Our results show a negative relation of firm age with trade credit. Thus, the youngest firms are forced to rely more on trade credit, due to their greater difficulties in gaining access to other financial resources. However, our results also show a significant non-linear relationship of the firm age with trade credit, which suggests a key role of trade credit in both younger and older SMEs. These findings are of interest, not only to academics, but also to firm managers. Moreover, this research is also relevant in the appropriate design of trade credit initiatives at European level and at country level, given the potential relevance of trade credit as a driver of sustainable economy in all stages of the life cycle of SMEs.

The rest of the article is structured as follows. We review the financial literature of this investigation and state the hypotheses of our study in Section 2. Section 3 presents our sample of SMEs, the variables to be studied, the descriptive statistics for all variables considered, and the model and methodology that we have followed in our research. Section 4 presents our empirical results, and finally, Section 5 concludes the article.

2. Literature Review: Theory and Empirical Evidence

2.1. The Relationship between Life Cycle and Trade Credit

Life cycle is a biological concept which provides a useful tool in the study of organizations [27,28]. The organizational theory of a firm’s life cycle considers that organizations progress through various stages as they grow and develop [29,30], and every stage comprises a set of organizational activities and structures that change over time [31,32]. The importance of this paradigm is that the ability to adapt to a changing environment and to innovate can prevent decline and revitalize a corporation in its last stages. The path of this evolution is related—with internal factors, such as strategy choice, financial resources, and managerial ability, and with external factors, such as a competitive environment and macroeconomic factors [33].

The study of the relationship between the financial resources of SMEs and their life cycle is a relevant research topic in the corporate finance literature. Overall, there is a certain degree of consensus with respect to small businesses in that they evolve through age, and consequently their financial needs and the availability of financial resources also change [7,34]. Traditionally, empirical studies have focused on bank credit. This abundant literature has shown the significant influence of the life cycle on the leverage of SMEs [10,35,36,37,38,39].

Trade credit, one of the most relevant financial resources in SMEs, is also present in the different stages of the business life cycle [7]; another key research question is to establish the true nature of this relationship, that is, signs of the influence of the life cycle on trade credit. The sparse empirical literature on this topic usually introduces the life cycle with the firm-age variable and follows one of two approaches: a linear approach or a non-linear approach.

First and foremost, the impact of the life cycle on supplier financing has been analyzed by assuming a linear relationship between age and trade credit. This approach implies that a single or unique sign, positive or negative, would explain the changes that the trade credit experiences throughout the life of the company. On the one hand, a negative relationship between a firm’s life cycle and trade credit has mainly been explained by the asymmetric information financial theory. This theory states that the use of the financing choices of a firm depends on its opacity regarding the relevant financial information available to lenders [40]; the age of the firm can be considered a proxy of the firm’s financial transparency [10] and it is an efficient way to deal with asymmetry information problems [41]. Moreover, the firm age also indicates how long the firm has survived, and from the lender’s point of view is a good proxy for the reputation of the firm. According to Diamond [34], lenders learn certain characteristics of borrowers over the years, and decide whether to grant credit according to the obtained information. Thus, trade credit may play a relevant role for younger firms that have not yet acquired a sufficient level of reputation, credit worthiness, and size, and therefore present low debt capacity. In this case, suppliers could be able to channel trade credit to customers with a lack of financial resources, acting as lenders due to their greater skill in obtaining soft information regarding its borrowers [42]. As firms mature, the role of trade credit could become less important, since older firms have had time to build up a track record and a relationship with creditors [43,44].

Related with the asymmetric information perspective, the pecking-order theory of Myers and Majluf [45] establishes that firms prefer to use retained earnings, followed by debt (first the cheapest and then the most expensive), and finally by equity. Thus, as firms adjust the use of financial resources in response to their financial needs over their life cycle, it is possible that firms at the earlier stages may lack the capacity to generate internal financial resources and the possibility to access bank credit. This would imply that younger firms use more trade credit [16], although it is a more expensive type of credit [46]. By comparison, older companies have a greater capacity to generate internal resources and they have more access to debt, and consequently trade credit plays a more residual role in the financing of older SMEs [47].

On the other hand, the supply effect of trade credit assumes that firms with more years of operation should maintain a lasting relationship with their suppliers [46]. This supply effect would provide easier trade credit to older firms due to a trusting relationship built up over the years [48]. In this case, suppliers may be willing to concede credit to their customers because the former have broader interests than being simply financial intermediaries. Thus, suppliers may try to benefit in the long term by helping to maintain the business of their customers, and consequently, maintain their own business and future sales [12,49]. This argument implies a positive relationship between a firm’s life cycle and trade credit.

The empirical research, carried out on SMEs worldwide, studies the linear relationship between trade credit and age, and is of a mixed nature, even when the same period or geographical area are analyzed (Table 1). First, a negative relation is shown in the United Kingdom [43,50], Finland [51], Spain and Portugal [16,26], Japan [44], Italy [15], and in emerging countries [52]; second, a positive linear relation is observed in studies carried out on the US [49], Japan [53], and the European Union [12]; and third, no relationship is observed in Sweden [14] and in the European Union [13].

The second approach in the study on the influence of life cycle on trade credit analyzes the possibility of a non-linear relationship between the age of a firm and supplier financing, and therefore considers that the sign of this relationship could vary with the specific stages of the life cycle of the companies [48,54]. The empirical research on this topic has mostly used age and the square of this variable to account for the possibility of non-linearity and opposite behaviour at different ages. The results of scarce research carried on SME samples around the world (Table 2) are also non-conclusive: a non-linear relationship is shown in the United States [19,48] and in European countries [17]; while no such non-linear relation is observed in the United Kingdom [55], in Ireland [54], and in the European Union countries [18].

2.2. Research Hypotheses

Overall, research on the complex relationship between life cycle and trade credit has made numerous advances, which form the basis of this study, however, the controversy regarding the precise influence of firm age on the use of trade credit can mean that a one-size-fits-all approach to SMEs is inappropriate since that relationship differs depending on the type of SMEs analyzed [7,14,19]. Most empirical studies in Table 1 and all studies in Table 2 analyze SMEs across all industries (with the exception of the financial sector) and control the business sector with a dummy variable. However, it has been observed that the business sector is a highly relevant determinant of trade credit [14,20,21,22], and that firms in a given industry show similar use of trade credit, while trade credit varies considerably across industries. Therefore, the determinants of trade credit, including that of age, could also differ in terms of sector [23,24,25].

We focus on the manufacturing sector in order to clarify the relationship between age and trade credit in SMEs. Manufacturing is a highly relevant sector, which in 2014, was the second largest sector within the non-financial business economy of the European Union in terms of its contribution to employment (22%), and the largest contributor to non-financial business economy value added (25%); in the EU, manufacturing SMEs employed 59% of the workforce of the whole manufacturing sector and provided 44% of total value added [2]. Moreover, the manufacturing sector presents specific characteristics related to trade credit. In manufacturing companies, the purchases from suppliers represent a major percentage of firm costs [25,26,56], and the suppliers consider the value of the inputs delivered as strong collateral [57,58]. Therefore, manufacturing companies obtain trade credit more easily than others [13,22], and trade credit represents a relevant role as a financial resource of these firms [18,55].

On the basis of previous studies and on considering manufacturing SMEs, the following hypotheses are put forward in this research.

Hypothesis 1.

Younger manufacturing SMEs use more trade credit.

Younger manufacturing SMEs experience greater difficulties in accessing conventional financial resources, such as bank credit, due to their higher level of information asymmetry, however, at the same time, these firms establish a relationship with their suppliers from the first moment in their life cycle in order to ensure their production. This favors a greater use of trade credit in younger manufacturing firms, as has been observed by Mateut et al. [43], Matias-Gama and Van Auken [26], and Tsuruta [44].

Hypothesis 2.

The relationship between age and trade credit in manufacturing SMEs is non-linear.

As companies progress through their life cycle, their capacity to generate internal resources becomes higher and they become more transparent and use financial resources of a more formal nature, such as bank credit, and less supplier financing, following the pecking-order theory [8]. However, this negative relationship between age and trade credit is not indefinite, and once a manufacturing firm enters a later stage of its life cycle, this firm is no longer interested in continuing to reduce its levels of trade credit, and hence the supply effect gains strength, thanks to the continued need for the supplier-company relationship that has been built up over many years. The suppliers are interested in granting trade credit to old customers with the aim of maintaining turnover. Moreover, in old age, investment in fixed assets may no longer be necessary for a firm, although investment in stock does remain a requirement, and therefore also their financing.

Hypothesis 3.

The relevance of determinants of trade credit differs across the different stages of the life cycle of manufacturing SMEs.

The relevance of changes in the environment, structures, activities, and characteristics of a firm through the different stages of its life cycle also affects the determinant factors of the firm’s financial resources [27]. Along these lines, Serrasqueiro and Nunes [59] observe that there are considerable differences in the relationships between determinants of debt for young and old SMEs. La Rocca et al. [10] also show that there are systematic differences across the firm’s life cycle in the determinants of its capital structure. Therefore, not only may trade credit be affected by the firm’s progression through the different stages of its life cycle, but the determinant factors of trade credit could also change the way in which they affect supplier financing, depending on the stage within the life cycle in which the firm is situated.

3. Data, Variables, and Research Methodology

3.1. Sample and Data

The AMADEUS database (Analyze Major Databases from European Sources), collected by Bureau Van Dijk, was used for the selection of the firms contained in our study sample.

The sample of firms studied includes manufacturing SMEs. According to the Standard Industrial Classification of Economic Activities 2009 (NACE Rev. 2), manufacturing corresponds to Section 3. Apart from the fact that the companies must belong to the manufacturing sector, they must also be SMEs. We have followed the European Commission definition of SMEs as the criteria for the choice of the sample of companies. According to this definition, the number of employees should range between 10 and 250, sales should be between 2 million and 50 million euros, and total assets should range from 2 million to 43 million euros. Furthermore, SMEs are not required to have been active for every year studied.

The SMEs of our sample belong to 12 EU countries during the period 2008–2014, which is characterized by low or negative economic growth in the euro area. All these countries, which formed part of the Eurozone for the entire period analyzed, have been considered. This geographical area presents a certain degree of homogeneity thanks to sharing a common currency. To sum up, we use an unbalanced panel with 140,358 observations. Table 3 presents the number of total observations per year and country for our sample of manufacturing SMEs.

3.2. Variables

Trade credit (TCPAY) is our dependent variable and is defined as the ratio of trade payables to total assets [17,48,60,61]. To measure the influence of a firm’s life cycle over trade credit, we use the AGE variable, which is the number of years of a firm’s activity [54] and the quadratic term of age (AGE2) in order to investigate whether the relation of age with trade credit is non-linear [8,18,54].

In accordance with previous empirical studies, as control variables, classic firm-determinants of trade credit are included. First, we consider firm size (SIZE) as the logarithm of the total assets [48,54,61]. Second, the profitability of a firm (PROFIT) is defined as the ratio of earnings before interest and taxes to total assets [47,54]. Third, growth (GROWTH) is estimated as the percentage of the annual sales growth [17,48]. Fourth, liquidity (CASH) is measured as the ratio of cash to total assets [47,61]. Fifth and finally, we include short-term bank credit (STDEBT), measured as the ratio of short-term debts to total assets [17,62], and long-term bank credit (LTDEBT), measured as the ratio of long-term debts to total assets [63].

3.3. Descriptive Statistics

Table 4 shows the mean, median, standard deviation, minimum, and maximum for all the variables of the study in the whole sample. In order to control for outliers in the data, all variables are winsorized at 1% and 99%. Table 4 shows that EU manufacturing SMEs have a mean of approximately 23 years of operation and make major use of supplier financing: on average, 27.7% of their resources are trade credit. In addition, trade credit usage exceeds the use of bank credit (10.7% for short-term bank credit, and 8.1% for long-term bank credit). The relevance of supplier financing for manufacturing SMEs has also been shown in other previous empirical studies, such as those by García-Teruel and Martínez-Solano [17], McGuinness et al. [18], and Palacín-Sánchez et al. [63].

Table 5 presents the correlations between all the variables of the study. The correlations among the independent variables are comparatively low, which provides evidence that multicollinearity is not a problem.

3.4. Model and Methodology

In order to verify Hypotheses 1 and 2, in the baseline study of the influence of a firm’s life cycle on trade credit the variables AGE and the quadratic term of age, AGE2, are included in the following equation model. The model additionally includes firm-specific variables and time dummies as control variables:

where i is the firm, and t is the time period; µi represents the firm-specific effects, and εit represents the measurement errors. Moreover, following relevant studies on trade credit and the life cycle, in the equation, AGE is transformed into the logarithm of (1+age), and AGE2 into the logarithm of (1+age)2.

TCPAYit = β0 + β1 AGEit + β2 AGE2it + β3 SIZEit + β4 PROFITit + β5 GROWTHit + β6 CASHit + β7 STDEBTit + β8 LTDEBTit + time dummies + µit +εit,

We estimate the Equation (1) using estimators of fixed and random effects to take the individual effects into account (µit), with clustered standard errors at firm level. The Hausman test is performed to ascertain whether the individual effects are fixed or random. If the null hypothesis is not rejected, then correlation between the independent variables and the individual unobservable effects exists and the random effects model is not considered a good estimator since it is inconsistent. In the analysis, the Hausman test verifies that the fixed effects model is better than the random effects model. The tables below, therefore, show the results of estimation with only a fixed effects model.

On the other hand, to delve into the relationship between a firm’s life cycle and trade credit and to test whether the determinants of trade credit differ across the various stages of the life cycle of SMEs (Hypothesis 3), a cluster partition method has been applied for the identification of groups of SMEs at a similar stage of their life cycle. This approach is innovative in trade credit research, although it has already been used in capital structure research, for example, La Roca et al. [10] and Keasey et al. [39].

The financial literature has empirically determined life-cycle stages by using different quantitative discriminating variables, however there is no consensus concerning the number of stages, the nature of each stage, or the reasons for moving between them [64]. In accordance with Bulan and Yan [65], La Rocca et al. [10], and Serrasqueiro and Nunes [59], we perform our cluster analysis using the firm age as a relevant discriminating variable to differentiate stages in a business’s life cycle. A hierarchical clustering method, called Average-linkage cluster analysis, is used. This method calculates the distance between the groups of observations based on the distances in pairs between the observations, in which all the distances contribute equally to each calculated average.

4. Results

4.1. Baseline Analysis

This section presents the regressions that estimate the influence of age on trade credit. Table 6 reports the results from the fixed effects panel model, while controlling firm characteristics and year dummies. Our results show a negative relationship between AGE and trade credit and this effect is statistically significant at the 1% level. This finding verifies H1 and suggests that younger firms, which usually present more problems related to asymmetric information, tend to use more trade credit due to experiencing greater difficulties in obtaining conventional financial resources. Therefore, the asymmetric information financial theory is confirmed. This negative effect may also be favoured by the early relationship that is established in manufacturing companies with their suppliers. This result has also occurred in previous studies carried out on manufacturing SMEs [26,43,44].

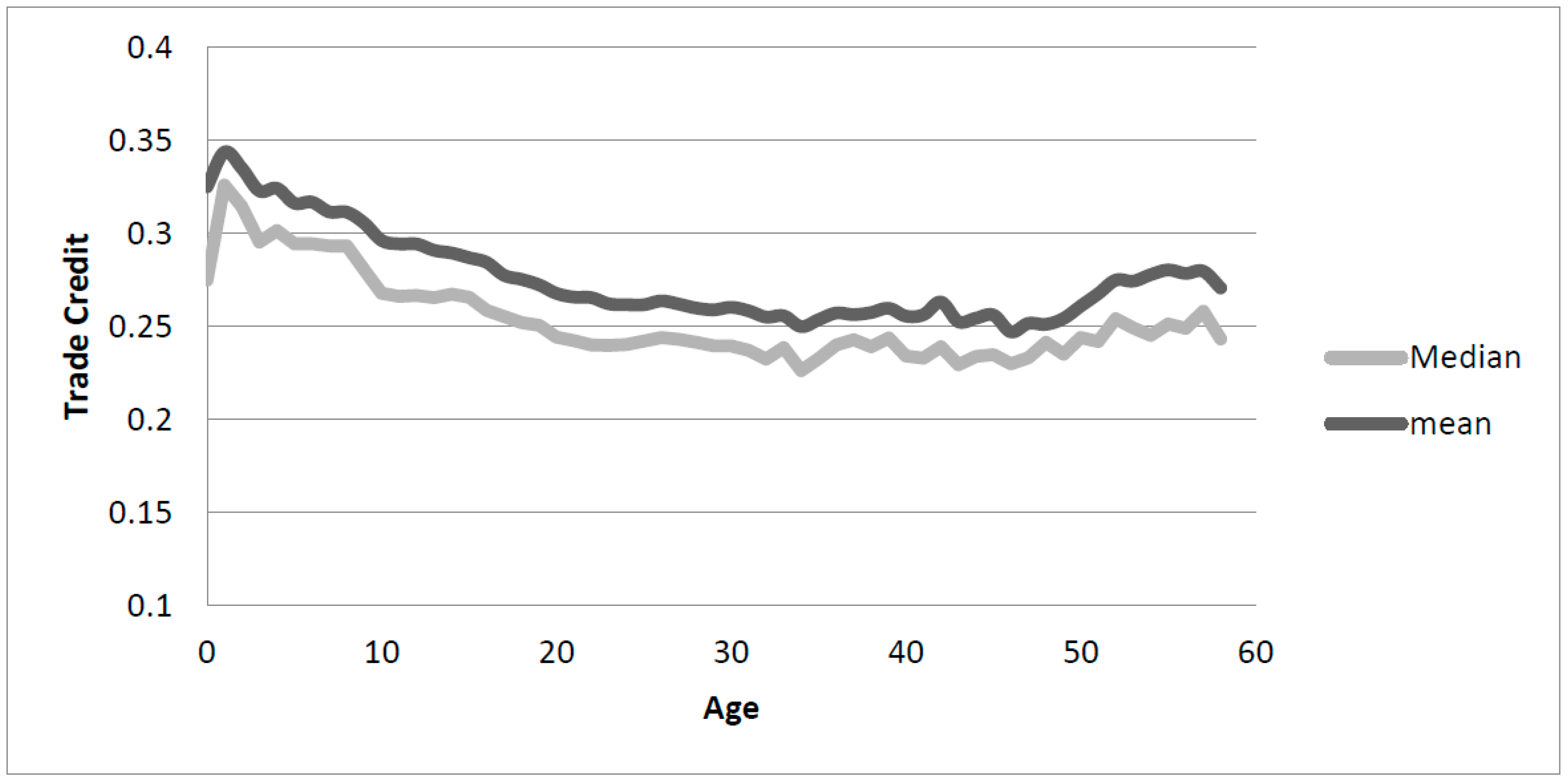

On the other hand, the square of age (AGE2) is significant in explaining the level of trade credit, and its coefficient has a positive sign. The change of sign of AGE2 regarding AGE shows a significant non-linear relationship with trade credit, thereby verifying H2. Compared with the very few previous empirical studies carried out on samples of all sectors, which had also confirmed a non-linear relationship between age and trade credit [17,19,48], it is noteworthy that, in our study, which focuses on manufacturing SMEs, the signs of this relationship in the specific stages of the life cycle vary in the opposite direction. Figure 1 provides a clearer illustration of the true nature of this non-linear relationship of trade credit as a function of age in manufacturing SMEs. In the start-up stage, firms use trade credit as a critical financial resource to sustain their business; subsequently, as younger firms progress along their life cycle, they accumulate more earnings and acquire more reputation and solvency, and therefore attain a greater capacity to finance with cheaper resources, such as bank credit. Consequently, the role of trade credit as a financial resource in SMEs gradually decreases thanks to the rebalancing of their capital structure, thereby confirming the pecking-order theory [46]. In the mature and consolidation stages, the sign of the relationship between trade credit and age ceases to be negative, and as Figure 1 shows, trade credit still plays a central role in these later stages but to a slightly lesser extent than in the earlier stages. The supply side effect of trade credit helps to partially explain the role of trade credit in older firms. Suppliers grant trade credit to older SMEs more easily due to a relationship of trust built over years. On the other hand, since customers need to continue investing in stock, they also need supplier financing, and these same suppliers consider the value of the inputs delivered to these manufacturing SMEs as strong collateral [57].

We subsequently investigate whether the influence of age on trade credit changes over time. Table 7 reports the estimation results of AGE and AGE2 from 2008 to 2014. All the other control variables are enclosed. The results are mostly statistically significant over time, and the non-linear relation between age and trade credit for manufacturing SMEs is shown for our period under study (with the exception of 2013 and 2014, where AGE2 presents a positive sign, although it is not significant). Therefore, Table 7 shows the existence of a significant pattern in the use of trade credit throughout the life cycle of manufacturing SMEs that is fairly constant over the time.

With regard to control variables (Table 6), SIZE and GROWTH present a positive relation with trade credit which shows that larger SMEs use more supplier financing, since the amount of assets of a firm is a proxy of the firm’s solvency for [16,48], and that SMEs use trade credit to finance their growth [16,56]. The negative coefficient of PROFIT clearly indicates the pecking-order theory and implies that firms of a greater profitability use less trade [17,55]. CASH shows a negative coefficient, which suggests that SMEs with a large liquidity cushion have a reduced reliance on credit from suppliers [66]. Finally, the negative coefficients of short-term bank credit (STDEBT) and long-term bank credit (LTDEBT) provide evidence that firms use more trade credit when they have difficulties in accessing short-term debt and long-term debt [14,60,63], thereby showing that trade credit and bank credit are substitute financing resources. Moreover, the coefficients of long-term bank credit are lower than the coefficients of short-term bank credit. Therefore, the substitutive relation of trade credit with long-term bank credit shows less importance than with short-term debt. This is due to the higher probability of trade credit being related with other short-term resources, as is commonly shown in previous empirical studies [54,66].

4.2. Cluster Analysis

In this section, with the aim of investigating further into the relationship between a firm’s life cycle and trade credit, and also to verify the existence of differences in trade credit determinants for manufacturing SMEs in terms of the different stages of their life cycle, we perform a cluster analysis using age as a relevant discriminating variable. Three different clusters have been identified which are statistically significant: Cluster 1 represents 35.5% of the whole sample and consists of young firms with an average age of 9.118 years; cluster 2 (approximately 39.8% of the whole sample) comprises mature firms with an average age of 23.33 years; and cluster 3 (approximately 24.7 of the whole sample) included mainly old firms (of an average of 45 years old).

Table 8 presents the descriptive statistics for the three clusters. The mean values of each and every variable in the three life-cycle stages show significant differences according to the analysis of variance (ANOVA) performed. The level of trade credit of young firms, with an average of 30.5%, is almost four percentage points higher than in mature and old firms; however, in mature and old age, the role of trade credit remains important and relatively stable. Therefore, Hypotheses 1 and 2 are again verified. Moreover, Table 8 shows how the financial literature has previously shown that SMEs in the earlier stages of their life cycles are characterized by having more growth opportunities (GROWTH) and are smaller in SIZE, CASH, and PROFIT (although PROFIT does decline in the cluster of old firms).

Table 9 presents regressions using the fixed effects model relating to the trade credit determinants in terms of the three clusters. The coefficients of all independent variables for the three clusters are statistically significant and maintain the same sign as in the whole sample (Table 6), however, differences in the magnitude of these coefficients are appreciated. The Wald test is applied to check global differences for the set of trade credit determinants. The null hypothesis of this test is that there are no differences in the estimated coefficients regarding relationships between determinants and trade credit in the three clusters considered. The Wald test in Table 9 shows that the three regressions are different, and therefore the determinant factors vary in their influence on trade credit depending on the stage of the firm’s life cycle. This result verifies H3.

It is worthy of note that the variation of the coefficients across clusters carries greater importance for short-term debt (STDEBT) and long-term debt (LTDEBT), which are followed by PROFIT, CASH, GROWTH, and SIZE. With regard to short-term debt (STDEBT) and long-term debt (LTDEBT), the change of magnitude of their negative coefficients through the three clusters show that the substitutive relation between trade credit and bank credit, already observed in Table 6, is moderated by the life-cycle stage of manufacturing SMEs. In this case, this type of relation between these financial resources is weaker in the early stage and becomes more intense as SMES reach the stage of maturity (although, the magnitudes of both variables decrease in the third cluster). In the mature stage, firms tend to increase the use of financial resources of a more formal nature, such as bank credit, and are willing to reduce the more expensive types of financial sources, such as trade credit.

With respect to PROFIT, its negative coefficient presents a higher magnitude in the early stage and then decreases through the next two stages (clusters of mature firms and old firms). This result suggests that the more profitable manufacturing SMEs in the cluster of young firms may have less reliance on trade credit, while in older life-stages the relevance of this factor declines. On the other hand, the negative coefficient of CASH increases its magnitude through the three clusters, showing that liquidity is a more relevant factor in the most advanced life-cycle stages of a company, because at an early age, companies cannot afford to have high levels of cash, and therefore the residual role of liquidity as a determinant of trade credit makes sense in the cluster of young firms.

Finally, regarding the variables with positive influence on trade credit, while GROWTH slightly increases its magnitude from one cluster to another, and is therefore moderated by the life-cycle stage of manufacturing SMEs, the coefficient of SIZE on trade credit is similar across the clusters of young firms and mature firms, however it does undergo a major increase in the third cluster.

5. Conclusions

This paper examines the effect of a firm’s life cycle on trade credit, a relatively under-researched topic with controversial results in the SME financial literature. We assume that the controversy in the previous empirical literature regarding the precise influence of firm age on the use of trade credit is probably based on the failure to consider the heterogeneity of companies. Therefore, this paper focuses on European manufacturing SMEs, and studies whether the trade credit and its firm-factor determinants differ depending on the stage of life cycle in which the SMEs are situated.

The results show a negative relationship between a firm’s life cycle and trade credit. Thus, younger manufacturing SMEs, which are less transparent and experience greater difficulty in accessing conventional financial resources, tend to use more trade credit. This is in direct contrast to older firms, which enjoy more financing choices, such as internal resources and bank financing to rebalance their capital structure. The information asymmetry theory and the pecking-order theory are confirmed by this finding.

Our results also provide evidence that the negative relationship between life cycle and trade credit is not maintained for the whole life cycle of the firm, which shows a non-linear relation of trade credit as a function of age. This suggests that in the mature and consolidation stages, the sign of the relationship between trade credit and age ceases to be negative, although trade credit still plays a central role in these older stages, but to a slightly lesser extent than in younger stages. This change of behaviour is mainly due to the supply side effect of trade credit, which seems to be highly relevant in manufacturing SMEs.

In addition, we observe that the effects of all the determinant factors over trade credit change in their degree of importance depending on the cluster of age to which the firm belongs. Therefore, the explanation of the use of trade credit depends on the stage of a firm’s life cycle.

These results should further the understanding of the relevance of the relationship between trade credit and the life cycle of SMEs in the manufacturing sector. From the point of view of managers, age clearly differentiates certain companies from others, although trade credit is a highly relevant financial resource in all stages of the life cycle. Therefore, managers can take advantage of their relationships with suppliers by initiating their integration into the sustainable economy. This conclusion should also be considered when the policymakers regulate this relevant financial resource in order to solve the financial problems of SMEs. The incorporation of SMEs, in which the manufacturing sector is highly significant, into investment with sustainable criteria requires financing, and trade credit can be used by the policymakers as a driver of sustainable finance, through which it is possible to promote the sustainable growth of SMEs of all ages. However, bearing in mind our results, it could be interesting to consider the age of firms in these trade credit regulations

Finally, this study presents two limitations. On the one hand, the life cycle of the SMEs is defined using, above all, the age variable, and on the other hand, it focuses on manufacturing SMEs. Therefore, as future research along these lines it would be of interest, first, to consider other variables together with age to define the life cycle of firms, and second, to consider other industries, such as those of the biotechnological or service sector, with specific characteristics regarding trade credit, in order to analyze their own relationship between the firm’s life cycle and trade credit.

Author Contributions

Conceptualization M.-J.P.-S. Literature review, F.-J.C.-C. and M.-J.P.-S. Research methodology and data analysis, F.D. Result analysis and discussions, M.-J.P.-S., F.-J.C.-C., and F.D. Writing of manuscript, M.-J.P.-S. and F.-J.C.-C. All authors agree on the final version.

Acknowledgments

We acknowledge the financial support of the Regional Government of Andalusia, Spain (Research Group SEJ-555).

Conflicts of Interest

The authors declare no conflicts of interest.

References

- OCDE. Financing SMEs and Entrepreneurs 2018: An OECD Scoreboard; OCDE Publishing: Paris, France, 2018. [Google Scholar] [CrossRef]

- European Commission. Annual Report on European SMEs 2014/2015; European Union: Luxembourg, 2018. [Google Scholar] [CrossRef]

- Chant, E.M.; Walker, D.A. Small business demand for trade credit. Appl. Econ. 1988, 20, 861–876. [Google Scholar] [CrossRef]

- Andrieș, A.M.; Marcu, N.; Oprea, F.; Tofan, M. Financial Infrastructure and Access to Finance for European SMEs. Sustainability 2018, 10, 3400. [Google Scholar] [CrossRef]

- European Union. Final Report of the High-Level Expert Group on Sustainable Finance. 2018. Available online: https://ec.europa.eu/info/publications/180131-sustainable-finance-report_en (accessed on 14 May 2018).

- Bancilhon, C.; Karge, C.; Norton, T. Win-Win-Win: The Sustainable Supply Chain Finance Opportunity. Report BSR, Paris 2018. Available online: https://www.bsr.org/reports/BSR_The_Sustainable_Supply_Chain_Finance_Opportunity.pdf (accessed on 14 May 2015).

- Berger, A.N.; Udell, G.F. The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. J. Bank. Financ. 1998, 22, 613–673. [Google Scholar] [CrossRef]

- Fluck, Z.; Holtz-Eakin, D.; Rosen, H. Where Does the Money Come From? The Financing of Small Entrepreneurial Enterprises; Working paper; Stern School of Business: New York, NY, USA, 1998. [Google Scholar]

- Teixeira, G.; dos Santos, M. Do Firms Have Financing Preferences Along Their Life Cycles? Theory, and Evidence from Iberia; Working paper; Financial Management Association: Tampa, FL, USA, 2006. [Google Scholar]

- La Rocca, M.; La Rocca, T.; Cariola, A. Capital structure decisions during a firms’s life cycle. Small Bus. Econ. 2011, 37, 107–130. [Google Scholar] [CrossRef]

- Hirsch, J.; Walz, U. Financing decisions along a firm’s life-cycle: Debt as a commitment device. Eur. Financ. Manag. 2011, 17, 898–927. [Google Scholar] [CrossRef]

- Casey, E.; O’Toole, C.M. Bank lending constraints, trade credit and alternative financing during the financial crisis: Evidence from European SMEs. J. Corp. Financ. 2014, 27, 173–193. [Google Scholar] [CrossRef]

- Andrieu, G.; Staglianò, R.; Van der ZwanBank, P. Bank debt and trade credit for SMEs in Europe: Firm-, industry-, and country-level determinants. Small Bus. Econ. 2018, 51, 245–264. [Google Scholar] [CrossRef]

- Yazdanfar, D.; Öhman, P. Substitute or complement? The use of trade credit as a financing source among SMEs. Manag. Res. Rev. 2017, 40, 10–27. [Google Scholar] [CrossRef]

- Deloof, M.; La Rocca, M. Local financial development and the trade credit policy of Italian SMEs. Small Bus. Econ. 2015, 44, 905–924. [Google Scholar] [CrossRef]

- Canto-Cuevas, F.J.; Palacín-Sánchez, M.J.; di Pietro, F. Trade credit in SMEs: A quantile regression approach. Appl. Econ. Lett. 2016, 23, 945–948. [Google Scholar] [CrossRef]

- García-Teruel, P.J.; Martínez-Solano, P. Determinants of trade credit: A comparative study of European SMEs. Int. Small Bus. J. 2010, 28, 215–233. [Google Scholar] [CrossRef]

- McGuinness, G.; Hogan, T.; Powell, R. European trade credit use and SME survival. J. Corp. Financ. 2018, 49, 81–103. [Google Scholar] [CrossRef]

- Alphonse, P.; Ducret, J.; Severin, E. When Trade Credit Facilitates Access to Bank Finance: Evidence from US Small Business Data; SSRN Working Paper; University of Lille I: Lille, France, 2006. [Google Scholar] [CrossRef]

- Fisman, R.; Love, I. Trade credit, financial intermediary development and industry growth. J. Financ. 2003, 58, 353–374. [Google Scholar] [CrossRef]

- Giannetti, M. Do better institutions mitigate agency problems? Evidence from corporate finance choices. J. Financ. Quant. Anal. 2003, 38, 185–212. [Google Scholar] [CrossRef]

- Psillaki, M.; Eleftheriou, K. Trade Credit, Bank Credit, and Flight to Quality: Evidence from French SMEs. J. Small Bus. Manag. 2015, 53, 1219–1240. [Google Scholar] [CrossRef]

- NG, C.K.; Smith, J.K.; Smith, R.L. Evidence on the determinants of credit terms used in interfirm trade. J. Financ. 1999, 54, 1109–1129. [Google Scholar] [CrossRef]

- Wilson, N.; Summers, B. Trade credit terms offered by small firms: Survey evidence and empirical analysis. J. Bus. Financ. Account. 2002, 29, 317–351. [Google Scholar] [CrossRef]

- Marotta, G. When Do Trade Credit Discounts Matter? Evidence from Italian Firm-Level Data. Appl. Econ. 2005, 37, 403–416. [Google Scholar] [CrossRef]

- Matias Gama, A.P.; Van Auken, H. The interdependence between trade credit and bank lending: Commitment in intermediary firm relationships. J. Small Bus. Manag. 2015, 53, 886–904. [Google Scholar] [CrossRef]

- Lester, D.L.; Parnell, J.A.; Carraher, S. Organizational life cycle: A five-stage empirical scale. Int. J. Organ. Anal. 2003, 11, 339. [Google Scholar] [CrossRef]

- Hoy, F. The complicating factor of life cycles in corporate venturing. Entrep. Theory Pract. 2006, 30, 831–836. [Google Scholar] [CrossRef]

- Mintzberg, H. Power and organization life cycles. Acad. Manag. Rev. 1984, 9, 207–224. [Google Scholar] [CrossRef]

- Dodge, H.R.; Fullerton, S.; Robbins, J.E. Stage of the organizational life cycle and competition as mediators of problem perception for small businesses. Strateg. Manag. J. 1994, 15, 121–134. [Google Scholar] [CrossRef]

- Van de Ven, A.H. Suggestions for studying strategy process: A research note. Strateg. Manag. J. 1992, 13, 169–188. [Google Scholar] [CrossRef]

- Hanks, S.H.; Watson, C.J.; Jansen, E.; Chandler, G.N. Tightening the life-cycle construct: A taxonomic study of growth stage configurations in high-technology organizations. Entrep. Theory Pract. 1994, 18, 5–29. [Google Scholar] [CrossRef]

- Dickinson, V. Cash flow patterns as a proxy for firm life cycle. Account. Rev. 2011, 86, 1969–1994. [Google Scholar] [CrossRef]

- Diamond, D. Reputation acquisition in debt markets. J. Political Econ. 1989, 97, 828–862. [Google Scholar] [CrossRef]

- Petersen, M.; Rajan, R. The benefits of lending relationships: Evidence from small business data. J. Financ. 1994, 49, 3–37. [Google Scholar] [CrossRef]

- Michaelas, N.; Chittenden, F.; Poutzioris, P. Financial policy and capital structure choice in U.K. SMEs: Empirical evidence from company panel data. Small Bus. Econ. 1999, 12, 113–130. [Google Scholar] [CrossRef]

- Fluck, Z. Capital Structure Decisions in Small and Large Firms: A Life-Time Cycle Theory of Financing; Working paper; Stern School of Business: New York, NY, USA, 2000. [Google Scholar]

- Hall, G.; Hutchinson, P.; Michaelas, N. Determinants of the capital structures of European SMEs. J. Bus. Financ. Account. 2004, 31, 711–728. [Google Scholar] [CrossRef]

- Keasey, K.; Martínez, B.; Pindado, J. Young family firms: Financing decisions and the willingness to dilute control. J. Corp. Financ. 2015, 34, 47–63. [Google Scholar] [CrossRef] [Green Version]

- Smith, J.K. Trade credit and informational asymmetry. J. Financ. 1987, 42, 863–872. [Google Scholar] [CrossRef]

- Rodríguez-Rodríguez, O.M. Trade credit in small and medium size firms: An application of the system estimator with panel data. Small Bus. Econ. 2006, 27, 103–126. [Google Scholar] [CrossRef]

- Taketa, K.; Udell, G.F. Lending Channels and Financial Shocks: The Case of Small and Medium-Sized Enterprise Trade Credit and the Japanese Banking Crisis. Monet. Econ. Stud. 2007, 25, 1–44. [Google Scholar]

- Mateut, S; Bougheas, S; Mizen, P. Trade credit, bank lending and monetary policy transmission. Eur. Econ. Rev. 2006, 50, 603–629. [Google Scholar] [CrossRef] [Green Version]

- Tsuruta, D. Bank loan availability and trade credit for small businesses during the financial crisis. Q. Rev. Econ. Financ. 2015, 55, 40–52. [Google Scholar] [CrossRef]

- Myers, S.; Majluf, N. Corporate financing and investment decision when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef]

- Atanasova, C. Access to institutional finance and the use of trade credit. Financ. Manag. 2007, 36, 49–67. [Google Scholar] [CrossRef]

- Kestens, K.; Van Cauwenberge, P.; Bauwhede, H.V. Trade credit and company performance during the 2008 financial crisis. Account. Financ. 2012, 52, 1125–1151. [Google Scholar] [CrossRef]

- Petersen, A.; Rajan, G. Trade credit: Theories and Evidence. Rev. Financ. Stud. 1997, 10, 669–691. [Google Scholar] [CrossRef]

- Danielson, M.G.; Scott, J.A. Bank Loan Availability and Trade Credit Demand. Financ. Rev. 2004, 39, 579–600. [Google Scholar] [CrossRef] [Green Version]

- Atanasova, C. How do firms choose between intermediary and supplier finance? Financ. Manag. 2012, 41, 207–228. [Google Scholar] [CrossRef]

- Niskanen, J.; Niskanen, M. The determinants of corporate trade credit policies in a bank dominated financial environment: The case of Finnish small firms. Eur. Financ. Manag. 2006, 12, 81–102. [Google Scholar] [CrossRef]

- Couppey-Soubeyran, J.; Héricourtb, H. The relationship between trade credit, bank credit and financial structure: From firm-level non-linearities to financial development heterogeneity. A study on MENA firm-level data. Documents de Travail du Centre d’Economie de la Sorbonne 2011, 8, 1–30. [Google Scholar]

- Tsuruta, D. Bank information monopoly and trade credit: Do only banks have information about small business. Appl. Econ. 2008, 40, 981–996. [Google Scholar] [CrossRef]

- McGuinness, G.; Hogan, T. Bank credit and trade credit: Evidence from SMEs over the financial crisis. Int. Small Bus. J. 2014. [Google Scholar] [CrossRef]

- García-Teruel, P.J.; Martínez-Solano, P. A Dynamic Perspective on the Determinants of Accounts Payable. Rev. Quant. Financ. Account. 2010, 34, 439–457. [Google Scholar] [CrossRef]

- Cuñat, V. Trade credit: Suppliers as Debt Collectors and Insurance Providers. Rev. Financ. Stud. 2007, 20, 491–527. [Google Scholar] [CrossRef]

- Biais, B.; Gollier, C. Trade credit and credit rationing. Rev. Financ. Stud. 1997, 10, 903–957. [Google Scholar] [CrossRef]

- Mian, S.; Smith, C. Accounts receivables management policy: Theory and evidence. J. Financ. 1992, 47, 169–200. [Google Scholar] [CrossRef]

- Serrasqueiro, Z.; Nunes, P.M. Is age a determinant of SMEs’ financing decisions? Empirical evidence using panel data models. Entrep. Theory Pract. 2012, 36, 627–654. [Google Scholar] [CrossRef]

- Fukuda, S.I.; Kasuya, M.; Akashi, K. The Role of trade credit for Small Firms: An Implication from Japan’s Banking Crisis. Jpn. Public Policy Rev. 2007, 3, 27–50. [Google Scholar]

- Yang, X. The role of trade credit in the recent subprime financial crisis. J. Econ. Bus. 2011, 63, 517–529. [Google Scholar] [CrossRef]

- Huang, H.; Shi, X.; Zhang, S. Counter-cyclical substitution between trade credit and bank credit. J. Bank. Financ. 2011, 35, 1859–1878. [Google Scholar] [CrossRef]

- Palacín-Sánchez, M.J.; Canto-Cuevas, F.J.; Di-Pietro, F. Trade credit vesus bank credit: A simultaneous analysis in European SMEs. Small Bus. Econ. 2018. [Google Scholar] [CrossRef]

- Levie, J.; Lichtenstein, B. A terminal assessment of stages theory: Introducing a dynamic states approach to entrepreneurship. Enterp. Theory Pract. 2010, 34, 317–350. [Google Scholar] [CrossRef]

- Bulan, L.; Yan, Z. The pecking order theory and the firm’s life cycle. Bank. Financ. Lett. 2009, 1, 129. [Google Scholar]

- Love, I.; Preve, L.A.; Sarría-Allende, V. Trade credit and bank credit: evidence from recent financial crisis. J. Financ. Econ. 2007, 83, 453–469. [Google Scholar] [CrossRef]

Figure 1.

The general effect of age on trade credit. Note: Trade credit is the ratio of trade payables to total assets.

Figure 1.

The general effect of age on trade credit. Note: Trade credit is the ratio of trade payables to total assets.

{kind=link}

Table 1.

Studies analysing the linear relation between trade credit and age on small and medium-sized enterprises (SMEs) worldwide.

Table 1.

Studies analysing the linear relation between trade credit and age on small and medium-sized enterprises (SMEs) worldwide.

| Study | Coefficient Sign of Age | Area |

|---|---|---|

| Danielson and Scott, 2004 [49] | + | USA |

| Mateut et al., 2006 [43] | − | UK |

| Niskanen and Niskanen, 2006 [51] | − | Finland |

| Tsuruta, 2008 [53] | + | Japan |

| Couppey-Soubeyran and Héricourtb, 2011 [52] | − | Emerging countries |

| Atanasova, 2012 [50] | − | UK |

| Casey and O’Toole, 2014 [12] | + | European Union |

| Tsuruta, 2015 [44] | − | Japan |

| Deloof and La Rocca, 2015 [15] | − | Italy |

| Matias-Gama and Van Auken, 2015 [26] | − | Portugal, Spain |

| Canto-Cuevas et al., 2016 [16] | − | Spain |

| Yazdanfar and Öhman, 2017 [14] | Not significant | Sweden |

| Andrieu et al., 2018 [13] | Not significant | European Union |

Table 2.

Studies analysing the non-linear relation between trade credit and age on SMEs worldwide.

| Study | Coefficient Sign of Age | Coefficient Sign of Age2 | Non-Linear | Area |

|---|---|---|---|---|

| Petersen and Rajan, 1997 [48] | + | − | Yes | US |

| Alphonse et al., 2006 [19] | + | − | Yes | US |

| García-Teruel and Martínez-Solano, 2010a [17] | + | − | Yes | European Union |

| García-Teruel and Martínez-Solano, 2010b [55] | Not significant | Not significant | No | UK |

| McGuinnes and Hogan, 2014 [54] | − | Not significant | No | Ireland |

| McGuinness et al., 2018 [18] | − | − | No | European Union |

Table 3.

Observations per year and country.

| Year | No. of Observations | % of Total | Country | No. of Observations | % of Total |

|---|---|---|---|---|---|

| 2008 | 18,635 | 13.28 | Austria | 2580 | 1.84 |

| 2009 | 19,110 | 13.62 | Belgium | 11,976 | 8.53 |

| 2010 | 19,621 | 13.98 | Germany | 11,341 | 8.08 |

| 2011 | 20,168 | 14.37 | Spain | 27,384 | 19.51 |

| 2012 | 20,680 | 14.73 | Finland | 3347 | 2.38 |

| 2013 | 21,519 | 15.33 | France | 39,182 | 27.92 |

| 2014 | 20,625 | 14.69 | Greece | 1244 | 0.89 |

| Ireland | 1085 | 0.77 | |||

| Italy | 34,415 | 24.52 | |||

| Netherlands | 641 | 0.46 | |||

| Portugal | 5873 | 4.18 | |||

| Slovenia | 1290 | 0.92 | |||

| Total | 140,358 | 100 | Total | 140,358 | 100 |

Table 4.

Descriptive statistics.

| Variables | Mean | Median | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| TCPAY | 0.277 | 0.250 | 0.201 | 0.000 | 0.784 |

| AGE | 22.921 | 20.000 | 15.767 | 0.000 | 197.000 |

| SIZE | 8.925 | 8.923 | 0.752 | 6.757 | 10.725 |

| PROFIT | 0.040 | 0.027 | 0.094 | −0.352 | 0.390 |

| GROWTH | 0.085 | 0.025 | 0.372 | −0.501 | 2.819 |

| CASH | 0.098 | 0.050 | 0.124 | 0.000 | 0.649 |

| STDEBT | 0.107 | 0.037 | 0.152 | 0.000 | 0.57 |

| LTDEBT | 0.081 | 0.022 | 0.291 | 0.000 | 0.8 |

Notes: TCPAY is defined as the ratio of trade payables to total assets, AGE is the number of years of a firm’s activity, SIZE is the logarithm of the total assets, PROFIT is the ratio of earnings before interest and taxes to total assets, GROWTH is the percentage of the annual sales growth, CASH is measured as the ratio of cash to total assets, STDEBT is the ratio of short-term debts to total assets, and LTDEBT is the ratio of long-term debts to total assets.

Table 5.

Correlation coefficient matrix.

| Correlation | TCPAY | AGE | SIZE | PROFIT | GROWTH | CASH | STDEBT | LTDEBT |

|---|---|---|---|---|---|---|---|---|

| TCPAY | 1.000 | |||||||

| AGE | −0.120 | 1.000 | ||||||

| SIZE | −0.162 | 0.218 | 1.000 | |||||

| PROFIT | −0.039 | 0.007 | −0.062 | 1.000 | ||||

| GROWTH | 0.064 | −0.149 | −0.083 | 0.033 | 1.000 | |||

| CASH | −0.059 | −0.015 | −0.155 | 0.145 | 0.023 | 1.000 | ||

| STDEBT | −0.088 | −0.008 | 0.113 | −0.136 | −0.031 | −0.270 | 1.000 | |

| LTDEBT | −0.078 | −0.024 | −0.006 | −0.056 | 0.005 | −0.055 | −0.004 | 1.00 |

Table 6.

Relationship between age and trade credit.

| Variables | ||

|---|---|---|

| AGE | −0.417 | *** |

| (0.000) | ||

| AGE2 | 0.162 | *** |

| (0.000) | ||

| SIZE | 0.022 | *** |

| (0.001) | ||

| PROFIT | −0.019 | *** |

| (0.003) | ||

| GROWTH | 0.020 | *** |

| (0.001) | ||

| CASH | −0.043 | *** |

| (0.004) | ||

| STDEBT | −0.187 | *** |

| (0.004) | ||

| LTDEBT | −0.013 | *** |

| (0.001) | ||

| Constant | 0.950 | *** |

| (0.010) | ||

| Year dummies | Yes | |

| Hausman test | 2208.52 | |

| Observations | 119,008 | |

Notes: AGE is the logarithm of (1+age), AGE2 is the logarithm of (1+age)2. Standard errors in parentheses; *** indicates significance at the 1% level.

Table 7.

Relationship between age and trade credit per year.

| Year | Constant | AGE | AGE2 | Obs. | Adjusted R-Squared | |||

|---|---|---|---|---|---|---|---|---|

| 2008 | 0.822 | *** | −0.193 | *** | 0.078 | *** | 15,217 | 0.131 |

| (0.019) | (0.000) | (0.000) | ||||||

| 2009 | 0.829 | *** | −0.244 | *** | 0.101 | *** | 15,901 | 0.122 |

| (0.019) | (0.000) | (0.000) | ||||||

| 2010 | 0.882 | *** | −0.149 | *** | 0.055 | * | 16,532 | 0.133 |

| (0.019) | (0.000) | (0.000) | ||||||

| 2011 | 0.926 | *** | −0.174 | *** | 0.069 | * | 17,240 | 0.106 |

| (0.019) | (0.000) | (0.000) | ||||||

| 2012 | 1.036 | *** | −0.044 | * | 0.006 | * | 17,927 | 0.152 |

| (0.018) | (0.000) | (0.000) | ||||||

| 2013 | 0.908 | *** | −0.061 | *** | 0.044 | 18,327 | 0.106 | |

| (0.019) | (0.000) | (0.000) | ||||||

| 2014 | 0.906 | *** | −0.011 | * | 0.009 | 17,864 | 0.101 | |

| (0.019) | (0.000) | (0.000) |

Notes: Ordinary least squares regressions (OLS); Robust standard errors in parentheses; *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Table 8.

Descriptive statistics per cluster.

| Cluster of Young Firms | Cluster of Mature Firms | Cluster of Old Firms | Anova F Statistic | |||||

|---|---|---|---|---|---|---|---|---|

| Variables | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | ||

| TCPAY | 0.305 | 0.226 | 0.266 | 0.185 | 0.251 | 0.175 | 1022.480 | *** |

| AGE | 9.118 | 4.567 | 23.325 | 4.185 | 45.014 | 14.263 | 24000.000 | *** |

| SIZE | 8.741 | 0.805 | 8.976 | 0.697 | 9.143 | 0.673 | 3661.370 | *** |

| PROFIT | 0.039 | 0.102 | 0.043 | 0.090 | 0.039 | 0.087 | 34.150 | *** |

| GROWTH | 0.161 | 0.503 | 0.047 | 0.267 | 0.034 | 0.256 | 1584.680 | *** |

| CASH | 0.099 | 0.124 | 0.098 | 0.121 | 0.098 | 0.126 | 3.670 | ** |

| STDEBT | 0.103 | 0.148 | 0.110 | 0.141 | 0.101 | 0.134 | 62.020 | *** |

| LTDEBT | 0.089 | 0.446 | 0.080 | 0.123 | 0.069 | 0.128 | 53.480 | *** |

Notes: Standard errors in parentheses; ** and *** indicate statistical significance at the 95% and 99% levels, respectively.

Table 9.

Determinants of trade credit for the three clusters.

| Variables | Cluster of Young Firms | Cluster of Mature Firms | Cluster of Old Firms | |||

|---|---|---|---|---|---|---|

| SIZE | 0.024 | *** | 0.023 | *** | 0.042 | *** |

| (0.002) | (0.002) | (0.002) | ||||

| PROFIT | −0.032 | *** | −0.022 | *** | −0.018 | *** |

| (0.006) | (0.005) | (0.006) | ||||

| GROWTH | 0.018 | *** | 0.021 | *** | 0.023 | *** |

| (0.001) | (0.001) | (0.002) | ||||

| CASH | −0.031 | *** | −0.054 | *** | −0.074 | *** |

| (0.008) | (0.006) | (0.007) | ||||

| STDEBT | −0.145 | *** | −0.280 | *** | −0.228 | *** |

| (0.007) | (0.006) | (0.007) | ||||

| LTDEBT | −0.006 | *** | −0.238 | *** | −0.096 | *** |

| (0.001) | (0.006) | (0.005) | ||||

| Constant | 0.139 | *** | 0.142 | *** | −0.073 | *** |

| (0.017) | (0.016) | (0.021) | ||||

| Year dummies | Yes | Yes | Yes | |||

| Hausman test | 570.94 | 398.52 | 1246.15 | |||

| Wald test | 879.81 | |||||

| Observations | 42,293 | 47,282 | 29,433 | |||

Notes: Standard errors in parentheses; *** indicates significance at the 1% level.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Canto-Cuevas, F.-J.; Palacín-Sánchez, M.-J.; Di Pietro, F. Trade Credit as a Sustainable Resource during an SME’s Life Cycle. Sustainability 2019, 11, 670. https://doi.org/10.3390/su11030670

AMA Style

Canto-Cuevas F-J, Palacín-Sánchez M-J, Di Pietro F. Trade Credit as a Sustainable Resource during an SME’s Life Cycle. Sustainability. 2019; 11(3):670. https://doi.org/10.3390/su11030670

Chicago/Turabian StyleCanto-Cuevas, Francisco-Javier, María-José Palacín-Sánchez, and Filippo Di Pietro. 2019. "Trade Credit as a Sustainable Resource during an SME’s Life Cycle" Sustainability 11, no. 3: 670. https://doi.org/10.3390/su11030670

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.