The Relationship of CSR Performance and Voluntary CSR Disclosure Extent in the German DAX Indices

Schumpeter School of Business and Economics, University of Wuppertal, 42119 Wuppertal, Germany

Sustainability 2021, 13(9), 4904; https://doi.org/10.3390/su13094904

Submission received: 23 March 2021

/

Revised: 22 April 2021

/

Accepted: 26 April 2021

/

Published: 27 April 2021

(This article belongs to the Special Issue Sustainability Accounting and Reporting)

Abstract

:Empirical studies present mixed evidence on the relationship of CSR performance and CSR disclosure extent, thus spurring academic ambiguity as legitimacy- and voluntary disclosure theory provide competing explanations. By applying content analysis to 144 voluntary GRI reports of listed firms in Germany from 2015 to 2018, I construct environmental and social disclosure indices to capture the reports’ disclosure extents. The contents are extracted from the corresponding GRI content indices in order to mitigate potential coding errors. ESG scores are used as a third-party measure to proxy environmental and social performance. I propose that this approach could be more suitable to address the challenge within the literature concerning methodological heterogeneity. The results show a positive relationship of environmental performance and environmental disclosure, but no relationship of social performance and social disclosure. Hence, there is evidence for an at least partial performance driven reporting behavior as companies seem to signal their superior environmental performance via more extensive disclosure, as predicted by voluntary disclosure theory. This evidence supports the idea of tightening Directive 2014/95/EU.

1. Introduction

In an environment of increasing social scrutiny, companies are required by their various stakeholders to account for sustainability aspects [1,2,3]. The overarching idea of corporate sustainability fosters different terms and nuances, for example corporate social responsibility (CSR), resulting in a synonymous use in previous literature [4]. This study will also draw from this simplification.

According to the European Commission, CSR is defined as the companies’ responsibility to voluntarily address their ecological and social impacts on society, which implies an awareness of their negative externalities [5,6]. CSR therefore marks a paradigm shift, as companies are not held accountable exclusively by their shareholders anymore [7]. As this engagement seems to be beneficial for all parties involved, the role of CSR is transforming from harm mitigation to corporate value enhancement [8,9]. This is generally characterized as providing a social benefit or public service in order to ensure approval by key stakeholders [10]. Therefore, CSR aspects must be integrated into the companies’ reporting systems in order to establish a communication channel [11].

Sustainability reporting in accordance with the Global Reporting Initiative (GRI) developed into the de facto standard in this respect, increasing the availability and comparability of the information provided [12]. Although there are indications that information asymmetries between reporting companies and their stakeholders decrease as information content increases [13,14,15], the voluntary sustainability information availability still does not appear to meet the demand of stakeholders [4,16]. At the same time, the nature of sustainability reporting is evolving, as it is increasingly integrated into mandatory reporting [17]. Empirical studies are therefore investigating the determinants of the extent of voluntary CSR disclosure in order to provide a better understanding of corporate reporting behavior.

The literature theorizes the relationship between corporate CSR performance and the corresponding voluntary CSR disclosure extent by legitimacy theory and voluntary disclosure theory (VDT). Legitimacy theory claims that organizations are required to obtain, maintain, or repair their legitimacy in order to avoid sanctions by society [18]. Particularly in the case of poor environmental performance, organizations would report more intensively in order to prevent a loss of legitimacy, thereby implying a negative relationship of performance and disclosure extent [19]. VDT argues that companies only voluntarily report beyond the regulatory requirements when they intend to communicate their superior performance, hence suggesting a positive relationship [20].

Both theories provide competing explanations for the relationship of CSR performance and the CSR disclosure extent. The mixed empirical evidence spurs the academic ambiguity, while a more recent study suggests a joint influence of both forces on the disclosure extent [21]. Amid the recent regulatory CSR reporting developments and the abstract requirements and leeway of Directive 2014/95/EU, this research subject has gained increasingly practical relevance because performance-oriented CSR reporting could result in an undesirable reporting behavior. In the German case, the law allows the use of a framework for the preparation of the non-financial statement in § 289d of the German Commercial Code (HGB), which motivates the analysis of GRI reports to analyze corporate reporting behavior. For the future development of mandatory CSR reporting, studies investigating voluntary sustainability reporting could be useful [22].

Within the literature, heterogeneity can be observed with regard to the measurement of the disclosure extent and non-financial performance. Disclosure extent is frequently measured by applying content analysis with a self-determined word catalog, whereas non-financial performance is measured by employing self-determined performance indicators [4,21]. The comparability of study results can therefore be described as limited, which explains the call for an objective methodology, and might explain the contrary results [21,23,24,25]. Recent studies also share these concerns and advocate for refraining from counting words to assess disclosure extents, and for the use of ratings to asses CSR performance [26,27].

The contribution of this paper is twofold. Firstly, I provide a way to address the literature’s methodological heterogeneity by applying an objectified research approach to investigate the relationship of disclosure extent and sustainability performance. I take advantage of the improved standardization and the availability of ESG scores, as I directly extract the reports’ contents from the GRI content indices and employ Thomson Reuters ESG scores to gauge the companies’ sustainability performance. Secondly, I analyze the heavily under-researched German sustainability reporting environment. Country-specific cultural conditions, such as the degree of stakeholder orientation, have a significant influence on the CSR reporting behavior by the companies located in the respective countries [28,29,30,31]. As the literature focuses on the topic almost exclusively in the light of the U.S. and the environmental context [23], there is a significant gap in the literature to extend the understanding of corporate CSR reporting behavior to other settings and to the social dimension. Although Germany, as the largest economy in the European Union, represents an interesting research setting, studies on the relationship of the CSR performance and CSR disclosure extent of German GRI reports are not available yet. I aim to close this gap.

The study’s sample contains 144 GRI reports from German companies which are listed in the leading indices DAX, MDAX, SDAX, and TecDAX from the reporting years 2015–2018. For the sake of simplicity, I resort to standardized GRI reports and the available third-party ESG ratings. CSR disclosure is captured and categorized based on a catalog of 30 topic-specific environmental and 35 social GRI indicators according to the topic-specific part of the GRI framework. Due to their increased availability, third-party ESG ratings have become a well-established and widely used method in this school of research to evaluate CSR performance objectively [32,33]. Thus, this study uses Thomson Reuters ESG scores to proxy the companies’ environmental and social performance. Breaking down sustainability into an environmental and a social analysis also provides insights into dimension-specific relationships. I employ an OLS model to investigate the relationship between the environmental and social GRI disclosure extent and the variables of the environmental score, social score, ownership structure, report audit, company age, company size, profitability, and industry affiliation.

The reported results produce evidence that a positive relationship exists between environmental performance and environmental disclosure extent, but also that no such relationship exists for the social dimension. The reported results suggest that companies signal their environmental performance by increasing the extent of their reporting, which is consistent with the argumentation of VDT. The presence of significant industry effects in both dimensions is potentially explained by the GRI’s key concept of materiality analysis. These findings enrich the ongoing academic discourse and underline that voluntary CSR reporting might be subject to a reciprocal relationship of internal and external factors [34].

This paper is structured into five chapters. Section 2 provides an overview of the relevant theoretical approaches and literature, and provides the base for the hypothesis development. Section 3 describes the research design by presenting the sample and the methodology. In Section 4, I present descriptive statistics and subsequently estimate the regression models. The results are discussed in Section 5.

2. Literature Review and Hypothesis Development

2.1. Theory

The relationship of CSR performance and CSR disclosure extent is theorized by legitimacy theory and voluntary disclosure theory (VDT) [34]. Legitimacy theory assumes that companies—as organizations—are integrated into society and are therefore subject to implicit and explicit societal demands [35,36]. In this context, corporate actions must conform to a system of social norms and values in order for the company to be accepted and to avoid adverse consequences [37,38].

In order to maintain, gain or restore legitimacy [18], companies set up a communication channel with their stakeholders for two reasons. On the one hand, they aim to find out about their information needs, and on the other hand, they seek to signal their intention to maintain legitimacy, for example by CSR reporting [39]. The disclosure of CSR information reduces the information asymmetries between the company and the addressed stakeholder groups, and pursues the primary goal of obtaining their support and consent. This, in turn, could result in potential benefits for the company, such as improved reputation, easier access to equity and debt capital, and stronger employee loyalty, which is why these benefits can also be an indirect motivation for CSR reporting [40].

VDT implies a strategic reporting behavior and thus represents a contrary approach to the legitimacy-based argumentation. It argues that companies are only incentivized to voluntarily report beyond the statutory requirements if this enables them to differentiate themselves from other companies [41,42]. When making voluntary disclosure decisions, management always takes into account the cost–benefit ratio of disclosure and signals its performance when it expects to gain advantages for the company by reducing information asymmetries. Signaling theory imposes two core conditions on a signal: it must not be easy to copy and it must correspond to the actual quality of the company [42]. In addition, the decision depends on whether the company’s performance exceeds a certain threshold, otherwise the costs of reporting would not be justified [41,43].

In the context of CSR reporting, the implications of VDT are predominantly examined when analyzing the relationship between environmental reporting and performance. Studies finding a positive relationship argue that the better the individual environmental performance, the more extensive the disclosure [20]. In the context of the legitimacy theory, on the other hand, it could be assumed that disclosure would be increased to prevent a loss of legitimacy, especially in the case of poor environmental performance [19].

2.2. Literature Review and Hypothesis Development

Several studies present evidence for the beneficial effects of CSR reporting [44]. Engaging in CSR and in subsequent reporting reduces information asymmetries between organizations and their stakeholders, hence reducing risk [15]. These activities are also becoming increasingly relevant for internal stakeholders, such as current and potential future employees. Companies benefit from an image as a reputable employer and strong employee retention, as employee productivity is positively correlated to seniority [45]. Employees are increasingly considering organizational CSR activities in their decision making, which creates additional demand [46]. CSR improves employee loyalty and enables them to reach their full potential [47,48]; consequently, CSR is beneficial for recruiting and increases employer attractiveness [49]. Recent studies have also shown that millennial job seekers are attracted by organizational CSR and seem to assign monetary value to it, as they partly prioritize CSR over higher wages [50,51].

The investigation of CSR performance as a determinant of the CSR disclosure extent gained traction with the American Toxic Release Inventory, and is therefore favored by increased regulation and the associated reporting obligations in the area of environmental emissions. The empirical studies focus on the environmental dimension, which can be attributed to the prioritized perception of environmental issues on the part of stakeholders and data availability [23]. The observed heterogeneity of research methods and results motivates further investigation, while allowing for a legitimacy- or performance-driven argumentation structure [34]. The following section presents the most relevant studies to gain a better understanding of the samples tested, the methodology, and the results. It is critical to note that most literature focuses on the ecological dimension of CSR, as the relationship of the social reporting extent and social performance seems to be heavily under-researched. This trend is observable for sustainability literature in general, which could be explained by the limited availability of social performance measurements [52,53].

Al-Tuwaijri et al. studied 198 U.S. companies from the S&P 500 index for the year 1994, and found a positive relationship between environmental performance and voluntary pollution-related information. The authors assessed environmental performance as the ratio of recycled toxic waste to the total toxic waste volume, while environmental reporting was determined by a weighted content index. The study showed that a company’s increasing environmental performance results in an increase of the reporting extent. The finding suggests that there is a link between voluntary disclosure and environmental reporting [54].

Cho and Patten analyzed 100 10-K reports from U.S. companies with a KLD environmental rating in 2001. Using content analysis, the authors created an environmental reporting index and examined how the environmental disclosure extent and the KLD environmental score are interrelated. The paper identified a negative relationship and argued that environmental reporting and its extent are used as legitimacy tools [55].

Clarkson et al. examined the environmental disclosure by 191 U.S. companies from five polluting industries for the year 2003. The extent of disclosure was determined through a content analysis based on GRI indicators, and then environmental performance was approximated based on corporate emissions of toxic chemicals relative to sales. Using a Tobit regression, the authors showed that there is a positive relationship between environmental performance and voluntary environmental disclosure, size, and capital intensity, and a negative relationship with the age of assets [13].

Cho et al. studied 119 U.S. companies in environmentally sensitive industries within the Fortune 500 index for the year 2006. Environmental performance was proxied as company emissions of toxic chemicals relative to sales. Deviating from Clarkson et al. (2008), they found evidence of a negative relationship between performance and disclosure extent, which they explained by the implications of legitimacy theory [56].

Papoutsi and Sodhi analyzed sustainability reports from 331 American, Canadian and European companies from 2014–2015. By applying factor analysis, they found that sustainable companies tend to disclose sustainability practices more frequently, supporting the implications of signaling theory [26].

As the literature review suggests, there is substantial heterogeneity in the literature which investigate CSR performance and the corresponding reporting. The discussion is marked by ambiguous results and seems to be highly sample-specific, as the robustness tests of the research designs partially yielded contradictory results [56]. The implications of VDT in the context of CSR reporting are predominantly based on the findings of financial reporting, and focus on environmental reporting [34]. Companies with superior environmental performance have incentives to inform their stakeholders about their corporate strategy and therefore publish environmental reporting content to a greater extent, thereby differentiating themselves from environmentally inferior companies [20]. This argument is fundamentally different from the implications of legitimacy theory. It assumes that companies with poorer environmental performance engage in more extensive environmental disclosure in order to secure their legitimacy [19,55]. As the link of ecological performance and the ecological disclosure is covered by literature, the analysis of the social dimension of CSR presents a blind spot in the literature. To my best knowledge, no study is available which transfers the research approach of these earlier studies to the social dimension.

In the spirit of an unbiased analysis methodology and in recognition of the mixed empirical evidence, the main hypothesis of this study is undirected, and is split into two dimensions:

Hypothesis 1 (H1).

There is a relationship of corporate environmental performance and environmental GRI disclosure extent.

Hypothesis 2 (H2).

There is a relationship of corporate social performance and social GRI disclosure extent.

3. Research Design

3.1. Sample

In order to analyze the German sustainability reporting environment, I performed an exhaustive survey on all companies in DAX, MDAX, SDAX, and TecDAX for the reporting years 2015–2018. The review of corporate websites and the GRI SDD Database yielded 271 GRI reports.

The analyzed period was subject to regulatory developments: for the years 2015 and 2016, GRI reporting was voluntary. However, with the introduction of the German CSR Directive Implementation Act in 2017, some GRI reports were classified as a mandatory non-financial information. Table 1 presents the sample composition.

As a mix of voluntary and mandatory reports could distort the observed disclosure dynamics, the mandatory reports were excluded from the sample.

Accordingly, the sample comprised, in total, 240 voluntary GRI reports. Due to the data availability of Thomson Reuters ESG scores, the final sample consisted of 144 voluntary GRI reports, for each of which an environmental and social ESG score was available.

The sample’s industry composition is heterogeneous, which makes the inclusion of all industries into the regression models disadvantageous, as the low ratio of observations to model variables would be prone to overfitting [57].

Industries with low sample coverage are bundled, with the condition that the group must not exceed the constituents of the largest identifiable industry. The definition of the industries corresponds to the sector classification of Deutsche Börse [58].

3.2. Methodology

The Global Reporting Initiative (GRI) is an independent international organization that provides the de facto standard for sustainability reporting [4]. Pioneering in the provision of sustainability frameworks, the GRI aims to support organizations to evaluate their own economic, environmental, and social impact, and to provide them with an adequate forum to communicate with their stakeholders. The GRI standard is divided into two parts: the general disclosures section and the topic-specific disclosures section. While the standards for the disclosures in the first section are applicable to all reporting companies and in corollary universal, the standards for the disclosures in the topic-specific section are to be determined by materiality analysis [59]. The underlying paper investigates the disclosure standards which are subject to the topic-specific section, as it reflects the individual disclosure decisions of the companies.

In the literature, various methodological approaches are used to determine the content of CSR reports. The disclosure extent is determined by the number of pages containing CSR information [60], or the number of relevant words [61]. A widely used approach is to construct a disclosure index, as it allows content assessment [54,62]. Quantitative elements receive a score of 3, more specific information receives a score of 2, general information receives a score of 1, and a score of 0 is given if the item is not present [54,55,63,64]. Other studies use a binary approach to measure reporting contents: if the report item is present, the corresponding variable takes a value of 1; otherwise, the value is set to 0 [65,66].

In this study, the contents of the individual GRI content indices are recorded and codified manually following the methodological approach of content analysis [67]. The period under study includes GRI reports based on two versions of the GRI Guidelines, the G4 Standard and the current GRI Sustainability Reporting Standard (2016), the latter of which has been mandatory since 1 July 2018. The two versions of the framework do not differ in their basic reporting principles, but mainly eliminate redundancies.

The environmental and social disclosure index in this study combine the structures and classify the collected reporting content according to the official transition documents [68]. If an indicator variable is listed in the GRI Content Index with a page reference or a reference, it is reported and equal to 1, otherwise it is set to 0. The sum of the codified GRI indicators represents the individual report’s environmental and social disclosure index. Full disclosure for each dimension is achieved when 30 environmental or 35 social indicators are codified.

The analysis of the report’s GRI Content Index is more appropriate, as it provides an objectified coding approach with small scope for misinterpretation. In corollary, ESG ratings help to eliminate subjectivity associated with CSR performance. Thus, this approach could be more suitable to address the methodological heterogeneity mentioned in the literature.

Thomson Reuters ESG scores (the successor of Thomson Reuters ASSET 4, nowadays superseded by Refinitiv) represent an established tool for the approximation of corporate CSR performance [69,70]. According to Thomson Reuters, they draw from information extracted from corporate communication channels (annual reports, CSR reports, capital market announcements, Internet presence) and from external sources such as NGO Internet presences and news media. Thomson Reuters ESG scores are constructed to represent the companies’ performance relative to their industry peers; therefore, the companies’ scores throughout the different industries are comparable. The Environmental Pillar Score captures ecological performance, and represents an aggregated score of the subcategories Resource Use, Emissions, and Innovation. The Social Pillar Score approximates social performance, and consists of the subcategories Workforce, Human Rights, Community, and Product Responsibility.

3.3. Regression Analysis

The underlying panel data consists of 2.6 reports per company. The panel setting allowed for a pooled OLS regression with company clustered standard errors, as the data set is unbalanced and offers a favorable ratio of 56 individual panels to only four observed time periods [71].

All of the model variables were collected based on the respective reporting year. The hypotheses were tested separately for the environmental and social dimension, and were estimated by the following models:

Hypothesis 1 (H1).

ENit = ß0 + ß1 (ENSit) + ß2 (WIDEit) + ß3 (ASSUREit) + ß4 (EMPLit) + ß4 (ROAit) + ß4 (AGEit) + ß4 (INDUSTRYit) + ß4 (YEARit) + εit

Hypothesis 2 (H2).

SOCit = ß0 + ß1 (SOCSit) + ß2 (WIDEit) + ß3 (ASSUREit) + ß4 (EMPLit) + ß4 (ROAit) + ß4 (AGEit) + ß4 (INDUSTRYit) + ß4 (YEARit) + εit

The dependent variables EN and SOC correspond to the values of the environmental and social disclosure indices, which were constructed based on the content analysis of the individual GRI content indices. The maximum achievable index value corresponds to 30 indicators for EN and 35 for SOC.

ENS and SOCS capture the environmental (Environmental Pillar Score) and social performance (Social Pillar Score) of the observed companies in ascending order, with values from 0 to 100. Inconclusive empirical evidence shows either a negative [55,56] or a positive [20,54,72] relationship, which can be explained by legitimacy theory and, for the latter, by VDT.

WIDE maps the ownership structure of a company. La Porta et al. argued that a dispersed ownership structure could be present when no investor owns 10% or more of the company’s shares [73]. In this study, the variable takes a value of 0 if this threshold is exceeded. Empirical evidence suggests that conflicts of interest and information asymmetries among shareholders increase as the ownership structure is more concentrated [74]. In the CSR context, in particular for GHG information, there seems to be a positive relationship between a dispersed ownership structure and the corresponding reporting extent [24,75]. However, the direction of this relationship could also be industry-sensitive, as some industry-exclusive studies identified conflicting evidence of a positive relationship between the disclosure extent and the size of the main investor [76,77].

ASSURE registers whether the GRI report has been audited by an independent third party and takes a value of 1 if it was audited, and 0 otherwise. Companies have their CSR reports audited to signal credibility and quality [78,79,80]. The audit of the report implies intrinsic CSR motivation, because companies with a high level of CSR commitment have their reports audited more frequently, which explains a positive relationship of the reporting extent and the presence of an audit [77,81].

EMPL reflects the size of the company, and corresponds to the natural logarithm of the number of employees in the respective reporting year. Large companies could publish more extensive CSR information because they impact many stakeholder groups through their diversified business areas and business regions [82]. Companies tend to increase their sustainability reporting extent in order to secure legitimacy, as their impact results in an increased need for information and monitoring on the part of stakeholders [83]. At the same time, larger companies have more resources at their disposal for reporting and take advantage of economies of scale in the production of information [20]. Empirical studies tend to find a positive relationship between company size and the CSR disclosure extent [4,84], while there are also studies that found no significant relationship [85,86].

INDUSTRY captures the industry affiliation on the basis of the first sector level of Deutsche Börse. Companies in environmentally sensitive industries are subject to higher social scrutiny and therefore larger public pressure, which can be relieved by increased reporting [87]. At the same time, industries differ in their social and environmental impacts on stakeholders. Chemical companies, for example, focus their reporting on environmental issues, compared to banks, which might focus more extensively on social issues [72,88]. As is consistent with the implications of legitimacy theory, empirical studies have discovered a positive relationship between the environmental reporting extent and the level of the company’s environmental exposure [89]. In this study, industry affiliation is of inherent relevance, as materiality analysis is the key concept of the GRI framework. The company-specific materiality analysis generates the report contents which are examined within this study. It enables the reporters to identify those sustainability aspects which are subject to the economic, ecological or social influence of the company, and which at the same time are substantially relevant for the decision-making of the stakeholders.

ROA captures profitability, and is the company’s return on assets, which is calculated as the ratio of the net income before interest on debt to total assets. The literature employs a legitimacy- or VDT-based explanation, as the findings are ambiguous, because it finds either a positive [90,91,92], a negative [84], or no relationship [24,93,94].

AGE corresponds to the company’s age, and is defined for this study as the period beginning with the company’s listing on the stock exchange. This corresponds to the natural logarithm of the difference between the reporting year and the year of the IPO. A constant of 1 is added to the difference in order to allow for a consistent calculation. Older companies have a more accurate perception of the demands of their stakeholders and the required level of CSR reporting [95]. Empirical results tend to document a positive relationship [96,97].

YEAR represents the respective reporting year. For companies with a fiscal year that differs from the calendar year, the attribution was made to the calendar year in which the majority of the fiscal year was conducted.

4. Results

4.1. Descriptive Analysis

According to the individual reports’ GRI Content Indices, the reports cover on average 51.9% of the environmental and 57.9% of the social reportable topic-specific GRI indicators. The reporting scope is comparable to results from other studies, where this seemingly low reporting scope is often criticized because the authors see room for plenty of improvement [98,99,100].

The literature frequently assesses the reporting quality via the sum of the reporting contents [72], but the appropriateness of this conclusion is questionable and may no longer be up-to-date, particularly due to the development of the GRI reporting standard [101]. The increased focus on the principle of materiality in GRI reporting since the GRI 4 framework implies that the full reporting of performance indicators is not required, as the contents to be reported should be prioritized via materiality analysis. Accordingly, a high reporting quality could also be achieved without a complete coverage of the reporting spectrum. In this context, reporting on insignificant aspects could even result in a lower quality due to the implications of information overload [102].

Table 2 presents the descriptive statistics for the variables of the regression model.

On average, the companies scored 70.86 on environmental and 76.47 on social performance, indicating that the examined reports are disclosed by companies with superior, above-average performance. This impression is reinforced by considering the median, which—at 77.20 and 81.68—is significantly higher than the mean in each case.

The audit rate of 84% for GRI reports clearly stands out from the results of previous studies [103]. Due to the regional differences, a universally valid statement is impossible, but the IÖW study on German CSR reporting from 2018, with an observed rate of 71% for large companies, could be used to frame this observation [104]. The high audit rate and the strong CSR performance of the companies in the sample could be related to the observation that companies have their reports audited when they are convinced of their high quality and performance [105]. In general, a report audit is desirable from the point of view of the report’s audience, as it signals credibility and reliability [79].

The ownership structure is balanced with regard to the absence of major shareholders, at around 48%. The distribution of company sizes is characterized by a wide range, with the median number of employees at the time of the report being 40,754. In order to reduce the influence of extreme observations, the number of employees is log-transformed. The return on assets shows an ordinary normal distribution, so no transformation is performed.

The literature frequently hypothesizes that a higher reporting scope is expected in environmentally sensitive industries, which can only partly be observed in this sample.

The industrial and utility industries exhibit a significantly lower environmental and social disclosure extent than, for example, the chemical and automobile industries, which can also be counted among the environmentally exposed industries. This observation could be an indication of the impact of the materiality principle in GRI reporting, as previous studies found a high reporting volume in the utilities industry in particular [24,106,107]. It is possible that while the stakeholder impact is high, the business activity is at the same time sharply narrowed down, resulting in streamlined reporting. This train of thought could be supported by the high score values and the observation that each report was externally audited. Evidently, the relationship between the reporting extent and performance cannot yet be conclusively determined, as a low reporting extent does not always go hand in hand with poor performance.

Table 3 provides an insight into the industry-specific disclosure extents and the CSR performance.

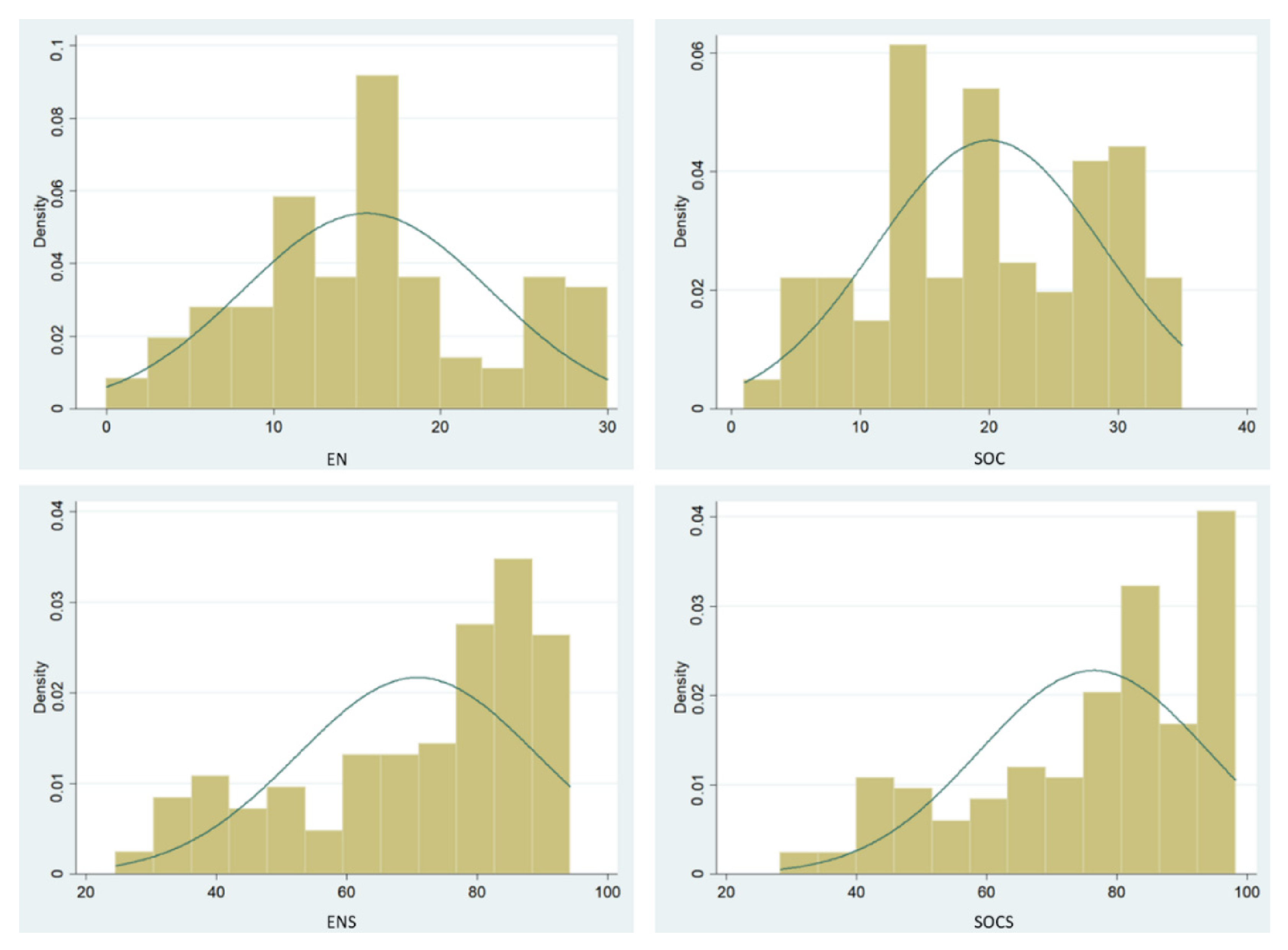

Figure 1 exhibits the distributions of the disclosure extents and ESG scores. While the environmental and social extents are approximately normally distributed, the distribution of the scores is overweighted, especially at the upper end of the distribution.

4.2. Correlation Analysis

Table 4 shows the Pearson correlations between the model variables. The variables INDUSTRY and YEAR are not included for the sake of brevity. The correlation matrix identifies a strong correlation between the environmental and social disclosure extents. The extents are significantly positively correlated with environmental and social performance, which may indicate performance-based reporting. The environmental disclosure extent is significantly positively correlated with the company size, supporting legitimacy theory. The strong positive correlation of the company size and score values support the empirical observation that larger companies perform more strongly in CSR in order to meet the demands of stakeholders and society [108].

It must be examined whether the latter observation could be attributed to the positive relationship of the environmental disclosure extent and corresponding performance, or whether it also persists in a multivariate analysis. The analysis of the correlation coefficients within the explanatory variables yielded values below 0.8, indicating no obvious signs of multicollinearity.

4.3. OLS Regression

An OLS regression analysis was performed in order to capture the joint relationship of the reporting extent and its determinants in Table 5. Multicollinearity seems unlikely as the VIF analysis resulted in values of less than 3 for all of the variables. The models explain a substantial proportion of the variance in the environmental and social reporting extents within the sample: 41.45% and 46.70%, respectively. The results allow a confirmation of Hypothesis 1, as the environmental report extent is positively related to environmental performance (p < 0.10). The positive relationship supports the argumentation of VDT and the implications of signaling theory, as the companies in this sample appear to signal their environmental performance via an increased environmental reporting extent. On the contrary, such a relationship cannot be demonstrated for social reporting. In contrast, the results reject Hypothesis 2, as a corresponding relationship cannot be found for social reporting.

The chemical industry was selected as the base industry in all of the estimations. The results provide evidence for significant industry-specific differences in disclosure extent, hence supporting the frequent empirical observations of disclosure extent’s sensibility to industry affiliation [4,89]. The significant model constants reflect the high disclosure extent in the chemical industry and show an extensive cross-industry base of the disclosure contents. Furthermore, the variation in social reporting seems to be even smaller, as there are only three industries which exhibit a significant difference to the chemical industry.

Auditing, ownership structure, size, profitability and age do not seem to be significantly related to the extent of environmental reporting. The absence of a relationship of size and reporting extent is noteworthy, as many studies identified a positive relationship here [4,89]. Hummel and Schlick stated that this observation could be attributed to the fact that the sample is limited to companies which are already exposed due to their size and index membership [21]. The findings regarding the social analysis show more and different significant relationships compared to the environmental dimension.

In contrast to the environmental reporting, a dispersed ownership structure seems to be positively related (p < 0.01) to the social disclosure extent. This finding adds to earlier empirical results, as the literature only presents findings for the environmental dimension [24,77], stating that a dispersed ownership structure favors information flow and mitigates information asymmetries. Still, it does not seem consistent that this effect is only found for the social dimension, which is yet to be explained by further research.

The companies’ age seems to be negatively related (p < 0.1) to the social reporting extent. Again, the literature exclusively found this observation for the environmental dimension, and commonly with a positive relation. As older companies could have a more accurate picture of the demands of their stakeholders and the required level of CSR reporting, this finding could imply that there is general trend to overreport on social indicators [95].

The reporting year 2016 was chosen as the baseline, as it provides the most observations and represents a caesura due to the introduction of mandatory sustainability reporting in Germany. In reporting year 2018, there seemed to be a significant increase of reported social indicators (p < 0.05).

The differences between the environmental and social analysis dimension provide new insights into corporate sustainability reporting behavior. In contrast to the environmental dimension, social performance does not seem to be related to social reporting. Still, there seem to be other determinants which are related to the disclosure extent. It remains to be explored how these differences could be consistently theorized, as these results could promote increased academic research interest and further analysis.

5. Discussion

The empirical literature presents mixed results for the relationship of CSR performance and CSR disclosure extent. It is unclear whether companies with poorer environmental performance engage in more extensive environmental reporting for legitimacy reasons [19,55], or whether companies with superior environmental performance report to a greater extent in order to differentiate themselves from companies with inferior performance [20,54,72].

I analyzed the relationship of disclosure extent and sustainability performance based on 144 GRI reports from German companies which are listed in the leading indices DAX, MDAX, SDAX, and TecDAX from the reporting years 2015–2018. For the sake of objectivity, I resorted to standardized GRI reports and the available third-party ESG ratings. CSR disclosure was captured and categorized based on a catalog of 30 topic-specific environmental and 35 social GRI indicators according to the topic-specific part of the GRI framework. Due to their increased availability, third-party ESG ratings have become a well-established and widely used method to evaluate CSR performance objectively [32,33]. Thus, this study used Thomson Reuters ESG scores to proxy the companies’ environmental and social performance. Breaking down sustainability into an environmental and a social analysis also provides insights into dimension-specific relationships. I employed an OLS model to investigate the relationship between the environmental and social GRI disclosure extent and the variables of the environmental score, social score, ownership structure, report audit, company age, company size, profitability, and industry affiliation.

The results present evidence for a positive relationship of environmental performance and environmental disclosure extent, but show no such relationship for the social dimension. This observation suggests that the observed companies signal their environmental performance by increasing the extent of their reporting, which is consistent with the argumentation of VDT. In terms of the legitimacy theory, a negative relationship between CSR performance and extent would have been expected. The more inferior an organization’s CSR performance would be, the more transparent it would have to become in order not to risk its legitimacy, which would negatively affect its business operations. The literature found empirical evidence that supports both theoretical explanations, so the results are consistent with certain studies [20,54,72], but at the same time also represent a contrary result to other studies [19,55,56]. One key finding was the differences between the disclosure extent determinants for the environmental and social dimensions, which calls for additional studies.

Out of the GRI’s and the report’s audience point of view, the results of this study are appealing, especially for the environmental dimension. The lack of significance for other determinants of disclosure extent could therefore be attributed to the power of standardization and harmonization. The reporting behavior seems to match the GRI’s, and therefore the stakeholders’ expectations. Compared to the highly significant industry effects, the positive relationship of environmental performance and disclosure extent does not seem to be the main driver of the variation of the reporting extent between companies. More likely, and consistent with the intention of the GRI’s key concept of materiality analysis, the industry affiliation seems to be the driving force within disclosure extent variation.

The GRI framework specifies that reporters must employ materiality analysis to identify the indicators which are important to stakeholders. Empirical studies show that companies in environmentally sensitive industries report more extensively [94,109], which probably stems from the greater number of material topics. In this study, the chemical industry was chosen as the reference category for the analysis of industry effects, as it is the largest identifiable industry with a high level of reporting coverage. The high environmental as well as social disclosure extents of the chemical, automotive, consumer goods, and transportation industries appear conclusive, as they can be counted among the environmentally sensitive industries. One exception, however, are utility companies, whose reports in this sample show a clearly restrained reporting behavior, although their ecological impact tends to be perceived as high. This observation could be explained by the fact that although they have a high social impact, their business operations are limited to fewer impact dimensions. The literature tends to assign environmentally sensitive industries (ESI) using NAICS codes. Due to the different industry classification in this study, this observation is counted as anecdotal evidence.

It should be emphasized that even after taking industry effects into account, there is a base of essential GRI indicators. Apparently, GRI reporting in Germany consists of sector-specific material indicators and a base of material indicators. While the former could be explained within the framework of stakeholder theory, the latter could be interpreted as an indication of the implications of legitimacy theory, and could be attributed to the societal and cross-stakeholder information needs that companies generally fulfill [37]. An example could be GHG emissions, which are not necessarily material for every company, but are nevertheless required due to the societal context and perception.

This assumption could also apply to the topic area of social reporting, wherein the lower reporting variation could imply an even broader need for information. At the same time, however, the lower variation could also be due to the employee-oriented legal situation in Germany, and consequently the better and easier data availability within the companies. Isomorphism as a process of homogenization also supports the argument for a distinct base of report content. DiMaggio and Powell defined isomorphism within institutional theory as a constraining process that forces one unit in a population to resemble other units exposed to the same conditions. Mimetic isomorphism could be a driver of some uniformity in reporting, as one organization takes its cue from the behavior of another organization when there is uncertainty about its own behavior [35,110].

The approaches in earlier studies to capture the disclosure extent are frequently based on counting keywords. In my opinion, this approach does not provide a balanced perspective on corporate sustainability reporting, as the number of keywords might not equal the actual variety of information which is supplied in sustainability reports. Intuitively, larger companies require more space when they report about their sustainability issues. The main question is whether the reporting scope should be measured by counting the individual sustainability issues within an issue dimension–which is probably prone to redundancy–or the explicit number of issue dimensions. By counting the reported GRI indicators, this study takes the latter approach. The disclosure extent in this literature represents the variety of topics that companies address, which might be more suitable to the analysis of the reports’ actual content message.

This study refrains from assessing reporting quality. Michelon et al. stated that the literature uses the disclosure extent to gauge the reporting quality, mostly with the expectation that the reporting should be complete as possible. However, in consideration of the materiality principle, which became the main concept after the introduction of the GRI G4 reporting standard, they argue that this expectation may no longer be relevant [101]. The focus on the principle of materiality from the G4 framework onwards implies that the complete reporting of performance indicators is not required, but that the content to be report should be prioritized via materiality analysis. It therefore seems conclusive that high reporting quality could be achieved even without the full coverage of the reporting spectrum.

The noticeably high environmental and social scores in the sample provide grounds for the limiting assumption that there is a possible self-selection of companies with an above-average CSR performance within CSR reporting. This observation could be driven by methodological aspects of this study, but at the same time could be interpreted as an argument for the implications of VDT.

Since Directive 2014/95/EU, the self-selection of companies into CSR reporting—at least for larger companies—was limited to supplementary voluntary reporting. In future, more precise analyses of the relationship of CSR performance and disclosure extent will be possible, as the companies concerned will have to—even if not to the same extent as in voluntary GRI reporting—report on non-financial aspects.

Considering the VDT implications, it can be assumed that good CSR performers will also report more within the non-financial statement or refer to their continued voluntary CSR reporting. Poor CSR performers will probably only cover the reporting minimum, as they will hold back as much as possible in terms of content in order not to reveal their actual performance.

My results support the idea of sharpening Directive 2014/95/EU. The identified positive relationship of environmental performance and reporting extent could result in potential adverse reporting behavior due to the possibility of performance-related reporting. Performance-related under-reporting would be inconsistent with the intention of Directive 2014/95/EU, which is to enable the various stakeholders to be informed about the influences that have a negative impact on them. We should prevent companies that exert those very influences on them not reporting about them sufficiently.

The current version of the CSR Directive may allow companies with poor CSR performance to obfuscate their performance, as quantitative reporting content such as CSR metrics are not yet mandatory. Within voluntary CSR reporting, Hummel and Schlick showed that companies with poor CSR performance prefer soft reporting with low quality because they cannot provide hard reporting with high quality, which is a signal of high CSR performance. Within their study, they classified hard reporting content as the content that is found in the GRI reporting in the topic-specific section and allows for a quantitative evaluation of the issues [21].

Venturelli et al. identified significantly higher quality within mandatory CSR reporting among Italian companies that have already voluntarily reported on CSR prior to Directive 2014/95/EU compared to companies reporting on non-financial content for the first time. Companies with non-financial reporting experience appear to report more comprehensively and completely in mandatory reporting [111]. Still, Tarquinio et al. presented evidence that Italian companies exhibited reduced CSR disclosure extents after the introduction of mandatory CSR reporting [112].

The stakeholders’ reactions shown in the review process of Directive 2014/95/EU in 2020 reflect an awareness of this matter [113]. In total, 69% of the responses advocated that specific environmental reporting content from the EU Commission’s environmental taxonomy should be included in mandatory non-financial reporting. The EU Commission’s environmental taxonomy comprises six environmental objectives, all of which are covered by the GRI reporting standard within the specific environmental reporting section. In the future, it would be conceivable that companies are obliged to report corresponding indicators, as this would be consistent with the intention of Directive 2014/95/EU. This implies that the companies concerned would have to deal in detail with specific performance indicators, either for reasons of performance improvement or because they would no longer be able to deal with the content requirements by means of abstract qualitative statements.

Future research is required to discuss the validity of the assumption that reporters exhibit a comparable reporting behavior for voluntary and mandatory reporting. Hypothetically, an improvement of reporting quality could also imply a change in corporate reporting behavior. Empirical studies have shown that the introduction of mandatory CSR improvement seems to improve reporting quality [114,115], but does not result in more sustainable organizational behavior [116,117].

In the European context, recent empirical literature has investigated the impacts of mandatory sustainability reporting on reporting quality. Several studies identified an improvement but were inherently limited by the regulation’s recency [111,118]. Another study and the stakeholder’s reactions in the review process of Directive 2014/95/EU still showed that improvement is necessary in order to achieve satisfactory reporting quality [113,119].

After providing further evidence on this fundamental research question, robustness checks of my approach would be beneficial, especially for the evaluation of CSR performance. Even though ESG scores and ESG ratings provide an objectified approach, they are subject to methodological criticism [69,120]. Several recent studies identified significant differences between the ESG evaluations of major ESG scores and ratings [121,122,123].

These insights call for robustness checks by applying different ESG scores to my obtained disclosure data. Due to the impacts of cultural conditions on CSR reporting behavior, the relationship of CSR performance and CSR should be investigated for a wider array of countries.

Consequently, this study is subject to various limitations. Its results cannot be generalized, as only reports from large and listed companies in Germany were examined. Even with the full sample conducted within the indices, the proportion of GRI reporters in relation to the population is limited. The Thomson Reuters ESG score is also subject to limitations, as the collection, composition and weighting of the processed data points are not presented in a transparent and replicable manner. Furthermore, it remains unclear according to which criteria Thomson Reuters prioritizes the provision of ESG scores. The lack of availability of ESG scores for certain companies in the sample may be coincidental, but may also have other reasons.

6. Conclusions

This study’s results present evidence for a positive relationship of environmental disclosure extent and environmental performance in the German context, and therefore allow of a ratification of Hypothesis 1. Hypothesis 2 is rejected because no relationship could be shown for social disclosure extent and social disclosure. Still, these results support the idea of tightening Directive 2014/95/EU in order to limit potential adverse reporting behavior due to the possibility of performance-related reporting.

With regard to the report’s audience point of view, the results of this study are appealing, as the lack of significance for other determinants of disclosure extent could be attributed to the power of standardization and harmonization. The partially inconsistent results of the environmental and social analysis dimension call for an expansion of the research scope into the social dimension.

Funding

This research received no external funding.

Data Availability Statement

The disclosure data presented in this study is available on request from the corresponding author. The remaining data is unavailable for sharing as it belongs to Thomson Reuters.

Acknowledgments

I appreciate the helpful comments of the anonymous reviewers. I also acknowledge support from the Open Access Publication Fund of the University of Wuppertal.

Conflicts of Interest

The author declares no conflict of interest.

References

- Newell, P. Citizenship, Accountability and Community: The Limits of the CSR Agenda. Int. Aff. 2005, 81, 541–557. [Google Scholar] [CrossRef] [Green Version]

- Pisani, N.; Kourula, A.; Kolk, A.; Meijer, R. How Global Is International CSR Research? Insights and Recommendations from a Systematic Review. J. World. Bus. 2017, 52, 591–614. [Google Scholar] [CrossRef]

- Pope, S.; Lim, A. The Governance Divide in Global Corporate Responsibility: The Global Structuration of Reporting and Certification Frameworks, 1998–2017. Organ. Stud. 2020, 41, 821–854. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of Sustainability Reporting: A Review of Results, Trends, Theory, and Opportunities in an Expanding Field of Research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- European Commission COM (2011) 681 final. A renewed EU strategy 2011-14 for Corporate Social Responsibility. In CELEX# 52011DC0681; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- Kinderman, D.P. Corporate Social Responsibility in the EU, 1993-2013: Institutional Ambiguity, Economic Crises, Business Legitimacy and Bureaucratic Politics. J. Common. Market. Stud. 2013, 51, 701–720. [Google Scholar] [CrossRef] [Green Version]

- Cooper, S.M.; Owen, D.L. Corporate Social Reporting and Stakeholder Accountability: The Missing Link. Account. Org. Soc. 2007, 32, 649–667. [Google Scholar] [CrossRef]

- Księżak, P. The Benefits from CSR for a Company and Society. J. Corp. Responsib. Leadersh. 2016, 3, 53–65. [Google Scholar] [CrossRef]

- Luetkenhorst, W. Corporate Social Responsibility and the Development Agenda. Intereconomics 2004, 39, 157–168. [Google Scholar] [CrossRef]

- Mohanty, J. Who decides on what to spend in CSR? Moving from compulsion to consensus. Int. J. Econ. Behav. Organ. 2014, 2, 13–19. [Google Scholar] [CrossRef] [Green Version]

- Brønn, P.S.; Vrioni, A.B. Corporate Social Responsibility and Cause-Related Marketing: An Overview. Int. J. Advert. 2001, 20, 207–222. [Google Scholar] [CrossRef]

- Fortanier, F.; Kolk, A.; Pinkse, J. Harmonization in CSR Reporting. Manag. Int. Rev. 2011, 51, 665. [Google Scholar] [CrossRef] [Green Version]

- Cui, J.; Jo, H.; Na, H. Does Corporate Social Responsibility Affect Information Asymmetry? J. Bus. Ethics 2018, 148, 549–572. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Rodríguez-Ariza, L.; García-Sánchez, I.M.; Cuadrado-Ballesteros, B. Corporate Social Responsibility Disclosure and Information Asymmetry: The Role of Family Ownership. Rev. Manag. Sci. 2018, 12, 885–916. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Sustainability Assurance and Cost of Capital: Does Assurance Impact on Credibility of Corporate Social Responsibility Information? Bus. Ethics Eur. Rev. 2017, 26, 223–239. [Google Scholar] [CrossRef]

- Thijssens, T.; Bollen, L.; Hassink, H. Secondary Stakeholder Influence on CSR Disclosure: An Application of Stakeholder Salience Theory. J. Bus. Ethics 2015, 132, 873–891. [Google Scholar] [CrossRef] [Green Version]

- Gatti, L.; Vishwanath, B.; Seele, P.; Cottier, B. Are We Moving Beyond Voluntary CSR? Exploring Theoretical and Managerial Implications of Mandatory CSR Resulting From the New Indian Companies Act. J. Bus. Ethics 2019, 160, 961–972. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef] [Green Version]

- Patten, D.M. The Relation between Environmental Performance and Environmental Disclosure: A Research Note. Account. Org. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the Relation between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Account. Org. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Hummel, K.; Schlick, C. The Relationship between Sustainability Performance and Sustainability Disclosure—Reconciling Voluntary Disclosure Theory and Legitimacy Theory. J. Account. Publ. Pol. 2016, 35, 455–476. [Google Scholar] [CrossRef] [Green Version]

- Dyduch, J.; Krasodomska, J. Determinants of Corporate Social Responsibility Disclosure: An Empirical Study of Polish Listed Companies. Sustainability 2017, 9, 1934. [Google Scholar] [CrossRef] [Green Version]

- Dragomir, V.D. How Do We Measure Corporate Environmental Performance? A Critical Review. J. Clean. Prod. 2018, 196, 1124–1157. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of Voluntary CSR Disclosure: Empirical Evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef] [Green Version]

- Masip, M. Desperately Seeking a Standard Metric for Corporate Social Performance. In Non-Financial Disclosure and Integrated Reporting: Practices and Critical Issues; Songini, L., Pistoni, A., Baret, P., Kunc, M.H., Eds.; Emerald Publishing Limited: Bingley, UK, 2020; pp. 9–35. [Google Scholar]

- Papoutsi, A.; Sodhi, M.S. Does Disclosure in Sustainability Reports Indicate Actual Sustainability Performance? J. Clean. Prod. 2020, 260, 121049. [Google Scholar] [CrossRef]

- Papoutsi, A.; Sodhi, M. A Sustainability Disclosure Index Using Corporate Sustainability Reports. J. Sustain. Res. 2020, 2, e200020. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Radhakrishnan, S.; Tsang, A.; Yang, Y.G. Nonfinancial Disclosure and Analyst Forecast Accuracy: International Evidence on Corporate Social Responsibility Disclosure. Account. Rev. 2012, 87, 723–759. [Google Scholar] [CrossRef]

- Dhaliwal, D.; Li, O.Z.; Tsang, A.; Yang, Y.G. Corporate Social Responsibility Disclosure and the Cost of Equity Capital: The Roles of Stakeholder Orientation and Financial Transparency. J. Account. Publ. Pol. 2014, 33, 328–355. [Google Scholar] [CrossRef]

- Kinderman, D.P. The Political Economy of Corporate Responsibility in Germany, 1995–2008. Mario Einaudi Center Int. Stud. Work. Paper 2008. [Google Scholar] [CrossRef] [Green Version]

- Matten, D.; Moon, J. “Implicit” and “Explicit” CSR: A Conceptual Framework for a Comparative Understanding of Corporate Social Responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef] [Green Version]

- Ahi, P.; Searcy, C.; Jaber, M.Y. A Quantitative Approach for Assessing Sustainability Performance of Corporations. Ecol. Econ. 2018, 152, 336–346. [Google Scholar] [CrossRef]

- Xiao, C.; Wang, Q.; van der Vaart, T.; van Donk, D.P. When Does Corporate Sustainability Performance Pay off? The Impact of Country-Level Sustainability Performance. Ecol. Econ. 2018, 146, 325–333. [Google Scholar] [CrossRef]

- Patten, D.M. Seeking Legitimacy. Sustain. Account. Manag. Pol. J. 2019, 11, 1009–1021. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Socio. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Meyer, J.W.; Rowan, B. Institutionalized Organizations: Formal Structure as Myth and Ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef] [Green Version]

- Deegan, C. Introduction: The Legitimising Effect of Social and Environmental Disclosures—A Theoretical Foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social Values and Organizational Behavior. Pac. Socio. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Mobus, J.L. Mandatory Environmental Disclosures in a Legitimacy Theory Context. Account. Audit. Account. J. 2005, 18, 492–517. [Google Scholar] [CrossRef]

- Gray, R.; Owen, D.; Adams, C. Accounting & Accountability: Changes and Challenges in Corporate Social and Environmental Reporting; Prentice Hall: London, UK, 1996. [Google Scholar]

- Verrecchia, R.E. Discretionary Disclosure. J. Account. Econ. 1983, 5, 179–194. [Google Scholar] [CrossRef]

- Morris, R.D. Signalling, Agency Theory and Accounting Policy Choice. Account. Bus. Res. 1987, 18, 47–56. [Google Scholar] [CrossRef]

- Lang, M.; Lundholm, R. Cross-Sectional Determinants of Analyst Ratings of Corporate Disclosures. J. Account. Res. 1993, 31, 246–271. [Google Scholar] [CrossRef]

- Weber, M. The Business Case for Corporate Social Responsibility: A Company-Level Measurement Approach for CSR. Eur. Manag. J. 2008, 26, 247–261. [Google Scholar] [CrossRef]

- Das, B.; Baruah, M. Employee Retention: A Review of Literature. IOSR J. Bus. Manag. 2013, 14, 08–16. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Corporate Social Responsibility, multi-faceted job-products, and employee outcomes. J. Bus. Ethics 2015, 131, 319–335. [Google Scholar] [CrossRef] [Green Version]

- Glavas, A. Corporate Social Responsibility and Employee Engagement: Enabling employees to employ more of their whole selves at work. Front. Psychol. 2016, 7, 796. [Google Scholar] [CrossRef]

- Slack, R.E.; Corlett, S.; Morris, R. Exploring Employee Engagement with (Corporate) Social Responsibility: A Social Exchange Perspective on Organisational Participation. J. Bus. Ethics 2015, 127, 537–548. [Google Scholar] [CrossRef] [Green Version]

- Duarte, A.P.; Gomes, D.R.; das Neves, J.G. Tell me your socially responsible practices, I will tell you how attractive for recruitment you are! The impact of perceived CSR on organizational attractiveness. Tékhne 2014, 12, 22–29. [Google Scholar] [CrossRef]

- Klimkiewicz, K.; Oltra, V. Does CSR enhance employer attractiveness? The role of millennial job seekers’ attitudes. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 449–463. [Google Scholar] [CrossRef]

- Waples, C.J.; Brachle, B.J. Recruiting Millennials: Exploring the Impact of CSR Involvement and Pay Signaling on Organizational Attractiveness. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 870–880. [Google Scholar] [CrossRef]

- Hutchins, M.J.; Richter, J.S.; Henry, M.L.; Sutherland, J.W. Development of indicators for the social dimension of sustainability in a US business context. J. Clean. Prod. 2019, 212, 687–697. [Google Scholar] [CrossRef]

- Čuček, L.; Klemeš, J.J.; Kravanja, Z. A review of footprint analysis tools for monitoring impacts on sustainability. J. Clean. Prod. 2012, 34, 9–20. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E., II. The Relations among Environmental Disclosure, Environmental Performance, and Economic Performance: A Simultaneous Equations Approach. Account. Org. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The Role of Environmental Disclosures as Tools of Legitimacy: A Research Note. Account. Org. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Cho, C.H.; Freedman, M.; Patten, D.M. Corporate Disclosure of Environmental Capital Expenditures. A Test of Alternative Theories. Account. Audit. Account. J. 2012, 25, 486–507. [Google Scholar] [CrossRef]

- Burnham, K.P.; Anderson, D.R. Model Selection and Multimodel Inference: A Practical Information-Theoretic Approach, 2nd ed.; Springer: New York, NY, USA, 2002. [Google Scholar]

- Deutsche Börse Gelistete Unternehmen. Available online: https://www.deutsche-boerse-cash-market.com/dbcm-de/instrumente-statistiken/statistiken/gelistete-unternehmen (accessed on 21 December 2020).

- GRI (Global Reporting Initiative) GRI 101: Foundation 2016. Available online: https://www.globalreporting.org/media/55yhvety/gri-101-foundation-2016.pdf?page=23 (accessed on 17 December 2020).

- Gray, R.; Javad, M.; Power, D.M.; Sinclair, C.D. Social and Environmental Disclosure and Corporate Characteristics: A Research Note and Extension. J. Bus. Finance Account. 2001, 28, 327–356. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A Study of the Environmental Disclosure Practices of Australian Corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Freedman, M.; Jaggi, B. Global Warming, Commitment to the Kyoto Protocol, and Accounting Disclosures by the Largest Global Public Firms from Polluting Industries. Int. J. Account. 2005, 40, 215–232. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I.; Lozano, M.B.; Rodríguez-Rosa, M. An Analysis of the Environmental Information in International Companies According to the New GRI Standards. J. Clean. Prod. 2018, 182, 57–66. [Google Scholar] [CrossRef]

- Zeng, S.X.; Xu, X.D.; Dong, Z.Y.; Tam, V.W. Towards Corporate Environmental Information Disclosure: An Empirical Study in China. J. Clean. Prod. 2010, 18, 1142–1148. [Google Scholar] [CrossRef]

- Dangelico, R.M.; Pontrandolfo, P. From Green Product Definitions and Classifications to the Green Option Matrix. J. Clean. Prod. 2010, 18, 1608–1628. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I.; Vicente-Villardón, J.L. Analysis of Environmental Indicators in International Companies by Applying the Logistic Biplot. Ecol. Indicat. 2012, 23, 250–261. [Google Scholar] [CrossRef]

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology; SAGE Publications Ltd.: Thousand Oaks, CA, USA, 2004. [Google Scholar]

- GRI (Global Reporting Initiative) Mapping G4 to GRI Standards. Available online: https://www.globalreporting.org/standards/media/1100/mapping-g4-to-the-gri-standards-disclosures-quick-reference.pdf (accessed on 21 December 2020).

- Drempetic, S.; Klein, C.; Zwergel, B. The Influence of Firm Size on the ESG Score: Corporate Sustainability Ratings under Review. J. Bus. Ethics 2020, 167, 330–360. [Google Scholar] [CrossRef]

- Rajesh, R. Exploring the Sustainability Performances of Firms Using Environmental, Social, and Governance Scores. J. Clean. Prod. 2020, 247, 119600. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental Reporting and Its Relation to Corporate Environmental Performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A. Corporate Ownership around the World. J. Finance 1999, 54, 471–517. [Google Scholar] [CrossRef]

- Gomes, A.R.; Novaes, W. Sharing of Control versus Monitoring as Corporate Governance Mechanisms. SSRN Electron. J. 2005. [Google Scholar] [CrossRef] [Green Version]

- Tauringana, V.; Chithambo, L. The Effect of DEFRA Guidance on Greenhouse Gas Disclosure. Br. Account. Rev. 2015, 47, 425–444. [Google Scholar] [CrossRef] [Green Version]

- Drobetz, W.; Merikas, A.; Merika, A.; Tsionas, M.G. Corporate Social Responsibility Disclosure: The Case of International Shipping. Transport. Res. E Logist. Transport. Rev. 2014, 71, 18–44. [Google Scholar] [CrossRef]

- Prado-Lorenzo, J.M.; Gallego-Alvarez, I.; Garcia-Sanchez, I.M. Stakeholder Engagement and Corporate Social Responsibility Reporting: The Ownership Structure Effect. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 94–107. [Google Scholar] [CrossRef]

- Ballou, B.; Heitger, D.; Landes, C. The Future of Corporate Sustainability Reporting: A Rapidly Growing Assurance Opportunity. J. Account. 2006, 202, 65–74. [Google Scholar]

- Ballou, B.; Chen, P.C.; Grenier, J.H.; Heitger, D.L. Corporate Social Responsibility Assurance and Reporting Quality: Evidence from Restatements. J. Account. Publ. Pol. 2018, 37, 167–188. [Google Scholar] [CrossRef]

- Cho, C.H.; Michelon, G.; Patten, D.M.; Roberts, R.W. CSR Report Assurance in the United States: An Empirical Investigation of Determinants and Effects. Sustain. Account. Manag. Pol. J. 2014, 5, 130–148. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Voluntary Environmental Disclosures by Large UK Companies. J. Bus. Financ. Account, 2006, 33, 1168–1188. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M. An Examination of Social and Environmental Reporting Strategies. Account. Audit. Account. J. 2001, 14, 587–617. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Jennifer Ho, L.C.; Taylor, M.E. An Empirical Analysis of Triple Bottom-Line Reporting and Its Determinants: Evidence from the United States and Japan. J. Int. Financ. Manag. Account. 2007, 18, 123–150. [Google Scholar] [CrossRef]

- Morhardt, J.E. Corporate Social Responsibility and Sustainability Reporting on the Internet. Bus. Strat. Environ. 2010, 19, 436–452. [Google Scholar] [CrossRef]

- Rouf, D. Corporate Characteristics, Governance Attributes and the Extent of Voluntary Disclosure in Bangladesh. Afr. J. Bus. Manag. 2011, 5, 7836–7845. [Google Scholar] [CrossRef] [Green Version]

- Patten, D.M. Exposure, Legitimacy, and Social Disclosure. J. Account. Publ. Pol. 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Kolk, A. Trends in Sustainability Reporting by the Fortune Global 250. Bus. Strat. Environ. 2003, 12, 279–291. [Google Scholar] [CrossRef]

- Dienes, D.; Sassen, R.; Fischer, J. What Are the Drivers of Sustainability Reporting? A Systematic Review. Sustain. Account. Manag. Pol. J. 2016, 7, 154–189. [Google Scholar] [CrossRef]

- Bayoud, N.S.; Kavanagh, M.; Slaughter, G. Factors Influencing Levels of Corporate Social Responsibility Disclosure Libyan Firms: A Mixed Study. Int. J. Econ. Finance 2012, 4, 13–29. [Google Scholar] [CrossRef] [Green Version]

- Marquis, C.; Qian, C. Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.O. What Explains the Extent and Content of Social and Environmental Disclosures on Corporate Websites: A Study of Social and Environmental Reporting in Swedish Listed Corporations. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Andrikopoulos, A.; Samitas, A.; Bekiaris, M. Corporate Social Responsibility Reporting in Financial Institutions: Evidence from Euronext. Res. Int. Bus. Financ. 2014, 32, 27–35. [Google Scholar] [CrossRef]

- Michelon, G. Sustainability Disclosure and Reputation: A Comparative Study. Corp. Reput. Rev. 2011, 14, 79–96. [Google Scholar] [CrossRef]

- Waluyo, W. Firm Size, Firm Age, and Firm Growth on Corporate Social Responsibility in Indonesia: The Case of Real Estate Companies. Eur. Res. Stud. J. 2017, 20, 360–369. [Google Scholar] [CrossRef] [Green Version]

- Gunawan, A.; Puntoro, H.R.; Pakolo, R.P. The Effect of Profitability, Company Age, and Public Ownership on Corporate Social Responsibility Disclosure. J. Akunt. Trisakti 2019, 5, 291–298. [Google Scholar] [CrossRef] [Green Version]

- Lucyanda, J.; Siagian, L.G. The Influence of Company Characteristics toward Corporate Social Responsibility Disclosure. In Proceedings of the International Conference on Business and Management, Phuket, Thailand, 6–7 September 2012. [Google Scholar]

- Lackmann, J. Nachhaltigkeitsberichterstattung nach GRI im HDAX. In Die Auswirkungen der Nachhaltigkeitsberichterstattung auf den Kapitalmarkt; Lackmann, J., Ed.; Gabler Verlag: Wiesbaden, Germany, 2010; pp. 121–132. [Google Scholar]

- Littkemann, J.; Schwarzer, S.; Miller, J. Nachhaltigkeitsberichterstattung von DAX-Unternehmen: Eine empirische Analyse. Controlling 2018, 30, 47–55. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An Analysis of Indicators Disclosed in Corporate Sustainability Reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR Reporting Practices and the Quality of Disclosure: An Empirical Analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef] [Green Version]

- Coombs, T.W.; Holladay, S.J. The Pseudo-Panopticon: The Illusion Created by CSR-Related Transparency and the Internet. Corp. Comm. Int. J. 2013, 18, 212–227. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Tsang, A. Causes and Consequences of Voluntary Assurance of CSR Reports. Account. Audit. Account. J. 2019, 32, 2451–2474. [Google Scholar] [CrossRef]

- IÖW & Future e.V. CSR-Reporting in Deutschland 2018. Available online: https://www.ranking-nachhaltigkeitsberichte.de/data/ranking/user_upload/2018/Ranking_Nachhaltigkeitsberichte_2018_Ergebnisbericht_lang.pdf (accessed on 21 December 2020).

- Ruhnke, K.; Gabriel, A. Determinants of Voluntary Assurance on Sustainability Reports: An Empirical Analysis. J. Bus. Econ. Manag. 2013, 83, 1063–1091. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. Environmental Reporting Management: A Continental European Perspective. J. Account. Publ. Pol. 2003, 22, 43–62. [Google Scholar] [CrossRef]

- Dobler, M.; Lajili, K.; Zéghal, D. Corporate Environmental Sustainability Disclosures and Environmental Risk: Alternative Rests of Socio-Political Theories. J. Account. Organ. Chang. 2015, 11, 301–332. [Google Scholar] [CrossRef]

- Udayasankar, K. Corporate Social Responsibility and Firm Size. J. Bus. Ethics 2008, 83, 167–175. [Google Scholar] [CrossRef]

- Helfaya, A.; Moussa, T. Do Board’s Corporate Social Responsibility Strategy and Orientation Influence Environmental Sustainability Disclosure? UK Evidence. Bus. Strat. Environ. 2017, 26, 1061–1077. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Coercive, Normative and Mimetic Isomorphism as Determinants of the Voluntary Assurance of Sustainability Reports. Int. Bus. Rev. 2017, 26, 102–118. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, F.; Cosma, S.; Leopizzi, R.; Pizzi, S. Directive 2014/95/EU: Are Italian Companies Already Compliant? Sustainability 2017, 9, 1385. [Google Scholar] [CrossRef] [Green Version]

- Tarquinio, L.; Posadas, S.C.; Pedicone, D. Scoring Nonfinancial Information Reporting in Italian Listed Companies: A Comparison of before and after the Legislative Decree 254/2016. Sustainability 2020, 12, 4158. [Google Scholar] [CrossRef]

- European Commission Ref. Ares (2020)3997889: Summary Report of the Public Consultation on the Review of the Non-Financial Reporting Directive. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=PI_COM:Ares(2020)3997889&from=EN (accessed on 17 December 2020).

- Lock, I.; Seele, P. The credibility of CSR (corporate social responsibility) reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef] [Green Version]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting. SSRN Electron. J. 2017. [Google Scholar] [CrossRef] [Green Version]

- Maniora, J. Is integrated reporting really the superior mechanism for the integration of ethics into the core business model? An empirical analysis. J. Bus. Ethics 2017, 140, 755–786. [Google Scholar] [CrossRef]