Employee-Related Disclosure: A Bibliometric Review

by

, , and

, , and

Albertina Paula Monteiro

1,* ,

,

Beatriz Aibar-Guzmán

2,

María Garrido-Ruso

2 and

Cristina Aibar-Guzmán

2 1

Porto Accounting and Business School, Polytechnic of Porto, 4465-004 Matosinhos, Portugal

2

Department of Financial Economics and Accounting, University of Santiago de Compostela, 15782 Santiago de Compostela, Spain

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(10), 5342; https://doi.org/10.3390/su13105342

Submission received: 26 March 2021

/

Revised: 23 April 2021

/

Accepted: 1 May 2021

/

Published: 11 May 2021

Abstract

:Academic research specifically focused on employee-related disclosure practices is needed to enhance understanding on CSR reporting. This paper aims to provide an overview of the state-of-the-art in research on employee-related disclosure, analyzing the characteristics of the scientific production on this topic. A bibliometric analysis is conducted on the papers specifically focused on employee-related disclosure published from 2000 to 2019 in journals indexed on the Web of Science database. The findings show that relatively few studies specifically focused on employee-related disclosure have been published over the last two decades (63 papers). Most articles were published during the last 8 years (93.6%), although the highest interest in the study of employee-related disclosure among scholars concentrates on a short period around 2017. Six journals concentrate 31.75% of the publications on the subject. Most papers are empirical studies, using the content analysis technique to analyze corporate reports. Papers are spread over three research subtopics: (1) extent, quality and drivers of human resource disclosures, (2) occupational health and safety disclosures, human rights disclosures and employee-related disclosures as a legitimization tool, and (3) diversity reporting. In all research subtopics, most of the papers have been published during the last four years, confirming that employee-related disclosure is a topic of current interest to researchers. The studies found that the overall level of employee-related disclosure is low, with an increasing or irregular tendency over time. Furthermore, not all items/categories got the same attention by firms. It can be concluded that this research subject is still far from reaching the level of research on environmental reporting and important issues remain to be resolved, both theoretically and empirically.

1. Introduction

Nowadays, Corporate Social Responsibility (CSR) constitutes a key element in firms’ corporate agenda worldwide [1]. In essence, CSR posits that firms ought to assume their responsibility towards society, which implies going beyond the search for economic profits and integrating social and environmental concerns in their operations and objectives [2,3]. At the same time, CSR supposes a new way of dealing with a company’s stakeholders, in which transparency plays an essential role [4]. In this sense, CSR reporting is the means used by companies to convey information regarding their CSR performance to stakeholders [5].

Although CSR reporting has been extensively studied from both a theoretical and empirical viewpoint over the last decades [6], most research has been focused on environmental reporting and/or the overall set of CSR disclosure dimensions, whereas relatively few studies laid emphasis on employee-related disclosures, analyzing them in isolation [7,8,9,10,11]. Furthermore, issues related to human resources management, such as work environment, occupational health and safety (OHS), work-life balance or diversity and equal opportunities, have been understudied by academic literature [12,13]. This lack of research attention can not only produce an imbalanced understanding of how firms are actually addressing the overall CSR agenda [11,14], since human resources management is a key aspect of a company’s CSR efforts [15,16,17,18], but also is surprising given the critical role played by employees in business success [19,20] and the growing stakeholder interest in human resources management practices and human rights [9,17,21,22].

In this sense, employee-related disclosures in corporate reports provide stakeholders with an indication of the value that firms place on their human resources [8,23] and what they are doing to develop quality workforce and enhance employees’ welfare [7,24]. Furthermore, employee-related disclosures may be a driving force to improve the companies’ working environment and their employees’ quality of life [10,11]. Consequently, academic research specifically focused on employee-related disclosure practices is not only needed to enhance understanding on CSR reporting but could also provide a basis for improving human resources management and reporting [11].

With these premises, this paper aims to provide an overview of the state of the art in the field of employee-related disclosure, as a specific category of CSR reporting, in order to systematize the existing studies and identify trends and gaps in the academic research on this topic. To achieve this overall objective, a bibliometric analysis is carried out on the papers specifically focused on employee-related disclosure published from 2000 to 2019 in journals indexed on the Web of Science (WoS) database by assessing the impact of authors, journals, countries/regions, and topics, as well as their temporal evolution.

Bibliometric analyses have become popular in recent years with the aim of exploring, organizing, and evaluating the scientific production that has been developed on a specific subject of study [25,26,27,28,29]. This type of analysis provides a better understanding of a subject identifying the issues that have received greatest research attention and assessing the characteristics and impact of the published papers [30,31], which allows researchers to identify trends and gaps in academic research on a subject. Bibliometric studies have been widely used in CSR reporting [26,27] and human resource management [32]; however, to the author’s knowledge, there is no previous bibliometric study of the research on employee-related disclosure.

In this sense, this study contributes to CSR literature by carrying out a systematization of the existing research on employee-related disclosure that provides a better understanding of the subject by assessing the characteristics (i.e., publication year, authors, country of origin, journals, etc.) and impact of the published papers, identifying the topics that have received the greatest research attention, and summarizing and critically analyzing the research that has been done on this subject. Thus, this study’s findings depict the current status of research on employee-related disclosure and provide a reference frame that could guide researchers regarding the direction of future studies on this subject.

This paper contains seven sections. After this introduction, the next section briefly addresses the overall characteristics of human resource information disclosure. The third section sets out the empirical framework of the bibliometric study, after which we present the main findings of the bibliometric analysis. In the fifth section, a critical discussion of the papers is carried out. The sixth section presents the complementary analysis. Finally, in section seven, the main conclusions of the study are drawn, the implications of the findings are discussed, the limitations of the study are acknowledged and some topics for future research are suggested.

2. Human Resource Information Disclosure

In a globalized environment that produces new employment models and poses new human resources management challenges, stakeholders pay increasing attention to the firms’ working conditions and treatment of employees, as well as issues such as diversity and equal opportunities [7,14,21]. In this sense, a company’s CSR agenda is considered unfeasible if it does not take into account the physical and emotional well-being of its employees [15] and integrates CSR principles into human resource management implementing policies to develop a quality workforce and enhance employees’ welfare [33].

Guidelines for socially responsible human resource management are defined through the principles, standards, and regulations issued by international organizations that promote CSR, decent work, and human rights [20,34]. In 1998, the International Labour Organization (ILO) issued the Declaration on Fundamental Principles and Rights at Work, which addresses a broad range of issues related to labour rights, inclusion, and social justice. More recently, the Sustainable Development Goals (SDGs), established in 2015 by the United Nations (UN) as part of the 2030 Agenda for Sustainable Development, incorporate decent work and the defense of human rights into the targets of a large number of goals. Thus, companies are expected to assume these societal goals and replace cost-driven human resources practices by others that contribute to improving employees’ quality of life [20,23], and promote egalitarian treatment of the workforce regardless of gender or race [35].

As noted by Deegan et al., “where there is limited concern, there will be limited disclosure” [36] (p. 335), accordingly to the extent and quality of employee-related disclosures provide stakeholders with a sign of a firm’s commitment with its employees’ welfare [7,24]. In this sense, several international organizations, both public (e.g., the UN, the Organization for Economic Co-operation and Development (OECD), and the European Union) and private (e.g., the Global Reporting Initiative (GRI), the International Organization for Standardization (ISO) and the International Integrated Reporting Council (IIRC), have stressed the importance of disclosing information related to companies’ human resource management practices in corporate reports and have actively promoted the disclosure of employee-related information. In Europe, non-financial information disclosure has been the subject of several initiatives by the European Commission (Directive 2003/51/EC and Directive 2014/95/EU), national legislators, and professional accounting organizations [37,38].

According to Cahaya et al. [10], employee-related disclosures can be viewed from two perspectives: intellectual capital disclosures [8,9] and labor-related CSR disclosures [14,18,39]. As regards the former perspective, employees are part of a firm’s human capital, which includes “knowledge, skills and technical ability, and personal qualities such as aptitude, attitude, energy, intelligence, commitment, the ability to learn, aptitude, creativity, imagination, collaboration, team participation and a focus on achieving the objectives of the employer company” [40] (p. 257). Accordingly, from this perspective, disclosures should refer to the employees’ ability to create value and, hence, their contribution to the company’s current and future performance [8,41]. On the other hand, labor-related CSR disclosures are aimed at enhancing corporate transparency and accountability through the provision of information related to the labor standards and principles of the ILO [7,13,42], including information regarding workforce profile, working conditions, diversity policies, work safety programs, and training programs, for example.

Employee-related disclosures are mostly voluntary and can be conveyed to stakeholders through different means, i.e., annual reports, sustainability/CSR reports, integrated reports, intellectual capital reports, human resources reports, corporate websites, etc. [20,21]. Prior research has shown that, in spite of the scant research attention that employee-related disclosures have received, companies do not report less employee-related information than environmental information [23], although some issues, such as diversity and equal opportunities, tend to be overlooked [11,12,17,18,26,30] and, in many cases, employee-related disclosure can be considered as a kind of public relation exercise [21]. Furthermore, prior studies suggest that the extent and quality of employee-related disclosures are associated with some variables related to firm characteristics (e.g., company size, ownership structure, organizational culture, strategy, industry affiliation, etc.) and institutional context characteristics, such as the country’s legal and economic system, cultural background, etc. [9,17,24,39,43].

3. Data and Methods

3.1. Sample Selection

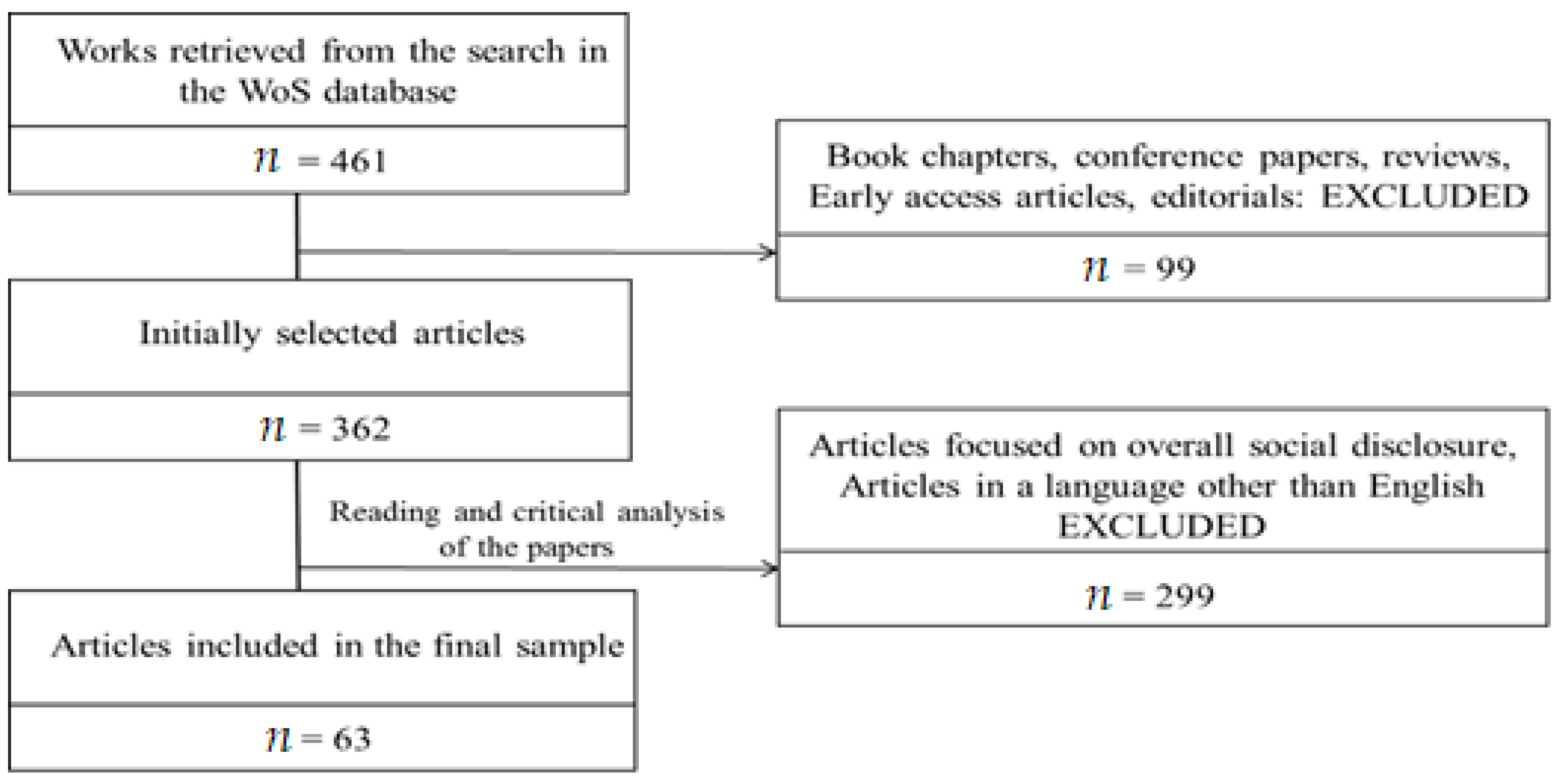

We conducted a comprehensive search to collect the papers specifically focused on employee-related disclosure published over the past 20 years (2000–2019). Papers were selected from the Web of Science (WoS) database. The reason behind this choice is that “WOS is a premier worldwide database of papers” [44] which includes the most “authoritative and high-impact academic journals”. Furthermore, many bibliometric analyses and literature reviews have been based on the WoS database [6,30,31,44,45,46].

The process followed to construct the data set consists of several steps. Firstly, to avoid possible bias and optimize the search strings, an exhaustive search was performed to identify the equivalent terms for each concept related to the research topic commonly used in literature. Thus, we chose several journals known for publishing articles on topics related to CSR reporting, human resources, and non-financial reporting (e.g., Journal of Cleaner Production, Sustainability, Journal of Business Ethics; International Journal of Human Resource Management, Social Responsibility Journal, Corporate Social Responsibility and Environmental Management, Journal of Intellectual Capital; Human Resource Management Review) and we looked for articles related to the subject under investigation. Based on such articles, a list of the keywords that are commonly used to characterize the articles related to the research topic was elaborated.

Once the keywords were identified, in a second phase we carried out a search for scientific publications in the WoS database by using combination of the words/keywords showed in Table 1. Although this initial search strategy seems rather large and inclusive, it allowed us to obtain all papers potentially related to our research subject without overlooking any possible topic [30].

This search returned 461 works. To ensure quality control, we only consider those works published in peer-reviewed journals [45,47,48]. Thus, we excluded book chapters (11 works), conference papers (67 works), reviews (15 works), and special issue editorials (3 works). Similarly, early access articles (3 works) were excluded to ensure consistency so that the final date of all papers corresponds to the period 2000–2019 (given that in some journals the time elapsed until the final publication of the article is very long).

After applying these filters, the sample was composed of 362 articles, which, in a third phase, were carefully read and separately analyzed by each author to identify the pertinent papers. Thus, each of the authors independently examined the papers and summarized their main characteristics and afterwards the results of this analysis were compared. This procedure allows us to avoid biases and ensure an adequate soundness level [37]. In this analysis, the following criteria were used:

- -

- Papers focused on overall social disclosure were excluded, since this study is specifically focused on the employee-related dimension of social disclosure.

- -

- Papers related to human rights (e.g., compulsory labor, non-discrimination, right to safe and healthy working conditions, etc.) were included because this topic is related to the rights of companies’ human resources.

- -

As a result of this analysis, 64 papers were identified. However, one paper was eliminated because it was written in German. Thus, the final sample consists of 63 papers. Although it is a small sample, its size is comparable to that of the samples used in other bibliographic or bibliometric reviews published recently (for example, Cillo et al. [45]—69 papers, Broccardo et al. [49]—21 papers, and Sáez-Martín et al. [31]—69 papers).

Figure 1 summarizes the selection process of the papers.

3.2. Data Analysis Procedure

VOSviewer version 1.6.15 was used to carry out the analysis of the data. VOSviewer is a software developed by Nees Jan van Eck and Ludo Waltman from the Center for Science and Technology Studies (CWTS) of Leiden University which pays attention to the graphical representation of bibliometric maps in an easy-to-interpret way [50].

Additionally, an analysis of the papers was carried out by synthesizing and critically analyzing their main characteristics (e.g., sample, method, findings, theoretical basis).

4. Findings

4.1. Scientific Production on Employee-Related Disclosure

Our analysis shows that relatively few studies specifically focused on employee-related disclosure have been published over the last two decades, compared to the large number of studies on environmental disclosure and/or CSR disclosure [6]. This evidence confirms prior statements regarding the limited research attention given to employee-related disclosure in literature (e.g., [7,9,10]).

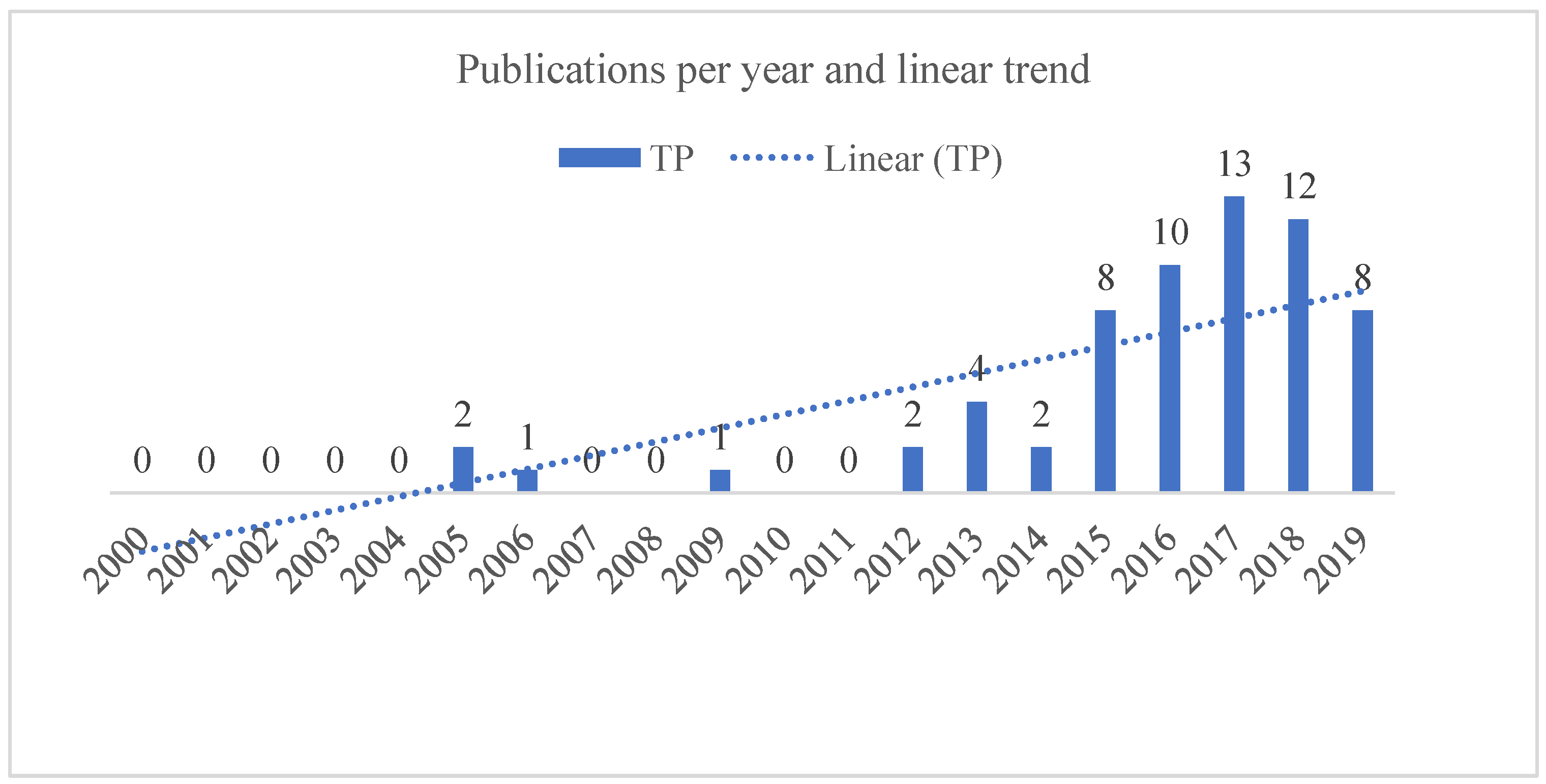

Figure 2 depicts the chronological evolution of the publications on employee-related disclosure over the last two decades. As can be seen, the first papers on the subject were published in 2005. These papers were written by Grosser and Moon [35] (published in Journal of Business Ethics) and Kawashita and colleagues [51] (published in Journal of Occupational Health). The most prolific year was 2017, with 13 published articles, followed by 2018 (12 papers) and 2016 (10 papers).

In terms of the temporal evolution of publications on employee-related disclosure, as shown in Figure 2, between 2005 and 2012 there was an irregular trend of some years having no publications (e.g., 2007, 2008, 2010, 2011). From 2014 to 2017 there was a noticeable increase in the number of publications, slightly decreasing in the following years. A potential explanation of this increase can be found in the Directive 2014/95/EU, as well as in the Agenda 2030 and the SDGs, which fostered interest in these issues by both companies and researchers [37].

Most papers were published during the last 8 years (59 papers representing 93.6% of the total published papers), although the highest interest in the study of employee-related disclosure among scholars concentrates on a short period around 2017. Accordingly, it can be said that research interest in this topic is current.

Table 2 shows the number of publications per journal. In total, 39 journals published papers specifically focused on employee-related disclosure, 33.33% of them belonging to the category Business, Finance (Accounting). The journals with more articles published on the subject are Pacific Business Journal of Business (ESCI), and Social Responsibility Journal (ESCI), with four papers each, followed by Accounting, Auditing & Accountability Journal (JCR), Asian Journal of Accounting and Governance (ESCI), Corporate Social Responsibility & Environmental Management (JCR), and Safety Science (JCR), with 3 papers each. With 20 papers in total, these six journals concentrate 31.75% of the publications on the subject. Ten journals have 2 publications, whereas the remaining 23 journals have only 1 publication.

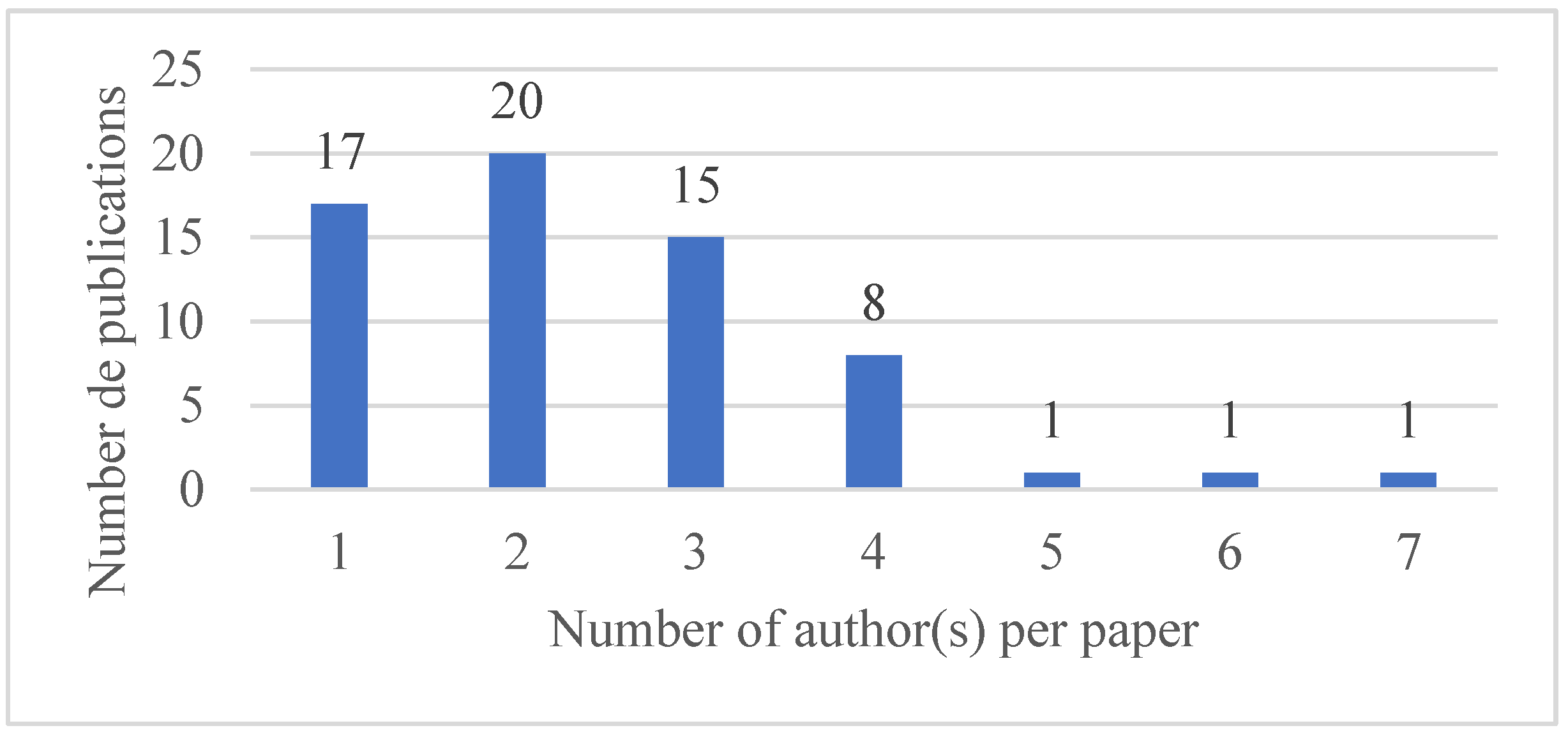

In total, 129 authors were identified. The author with more publications on employee-related disclosure is F.R. Cahaya (3 papers). There are 21 authors who have two publications, whereas the remaining authors have only published 1 paper on this subject. The number of authors per paper varies between 1 and 7 authors. The average number of authors per paper is 2.41. As shown in Figure 3, it is evident that there are far fewer single authored publications than papers published by multiple authors. Specifically, there are 17 single authored publications, whereas 46 papers were written by multiple authors. This trend towards collaboration between scholars researching on employee-related disclosure is maintained throughout the analyzed period.

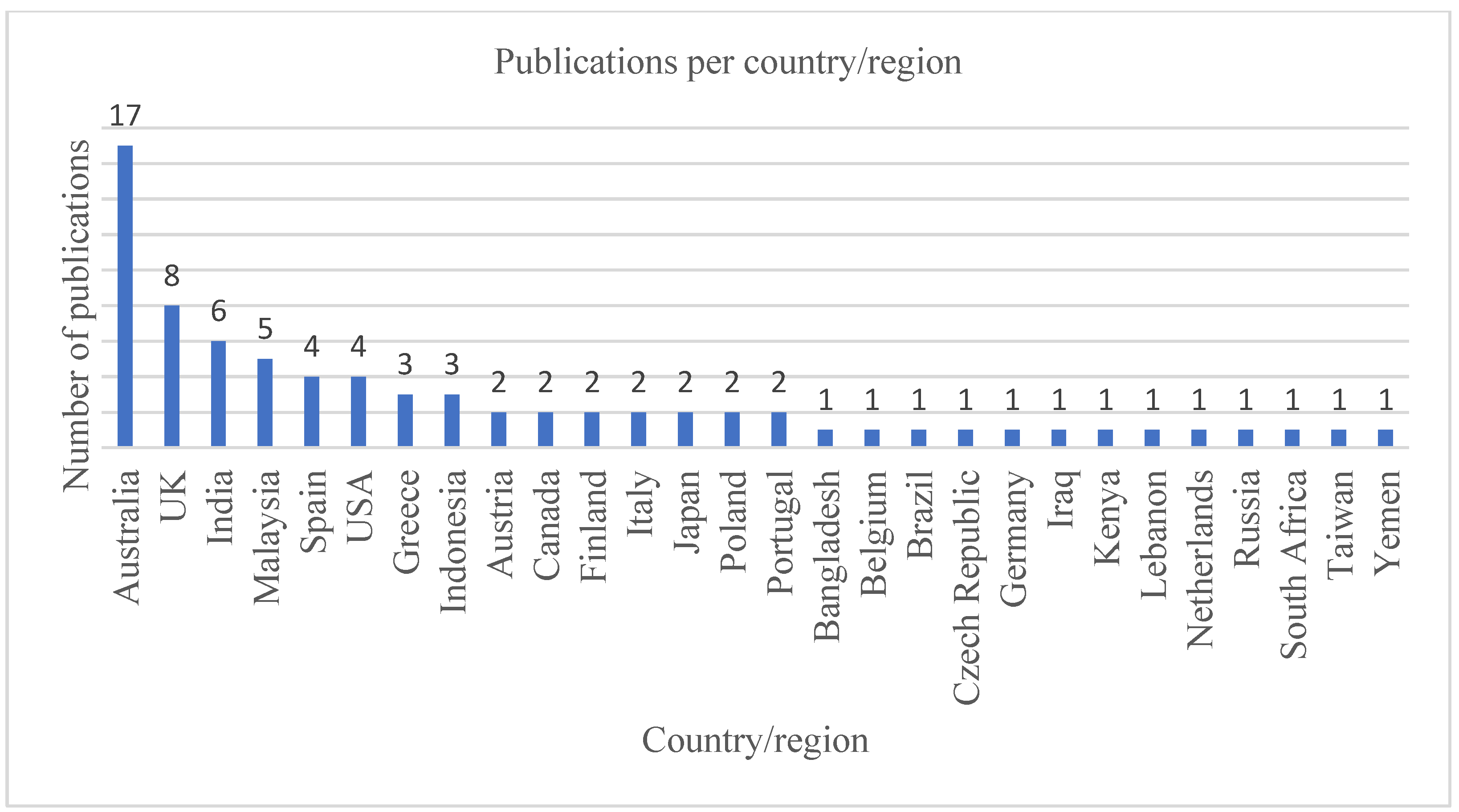

Figure 4 depicts the distribution of the papers on employee-related disclosure per country. In total, we found 28 countries with at least 1 publication. As can be seen, Australia stands out as the country with the highest number of publications on employee-related disclosure, followed by the UK (8 papers). As noted by Cahaya et al. [10] and Li et al. [21], most published studies on employee-related disclosure focus on developed countries (both Anglo-Saxon countries and European countries, as well as Japan). However, interestingly, there are three developing countries (India, Malaysia, and Indonesia) among the countries with a higher number of publications on employee-related disclosure, which could indicate a growing research concern about working conditions and labor-related human rights in developing countries, characterized by relaxed labor standards and a low-cost workforce [14]. Two plausible explanations of this result could be the increasing number of journals specifically focused on Asian countries’ issues indexed on the WoS database (e.g., Asian Journal of Accounting and Governance; Asian Review of Accounting; Asia Pacific Journal of Human Resources; Pacific Business Review International) and the increasing collaboration between scholars from emerging countries and scholars from countries with a well-established research tradition (e.g., [10,52]). On the other hand, Latin America is the region with fewer published papers, with only one paper focused on a country from this region (Brazil).

Another aspect to note is that there are no Scandinavian countries (i.e., Denmark, Norway, Sweden, Finland, and Iceland) among the countries with a higher number of publications on employee-related disclosure despite the fact that these countries have been pioneers in the development of intellectual capital management and reporting models, and are characterized by being greatly interested in social issues [8]. Likewise, the USA ranks sixth in number of publications on employee-related disclosure, despite the fact that, together with the UK and Canada, the USA has a greater number of journals indexed in WoS database, and is considered one of the most “performant” countries, in terms of papers [53]. In this sense, this limited research attention to employee-related disclosure by US scholars could be a reflection of the scant interest of US firms in this kind of disclosures as prior research has showed [54].

4.2. Research Subtopics

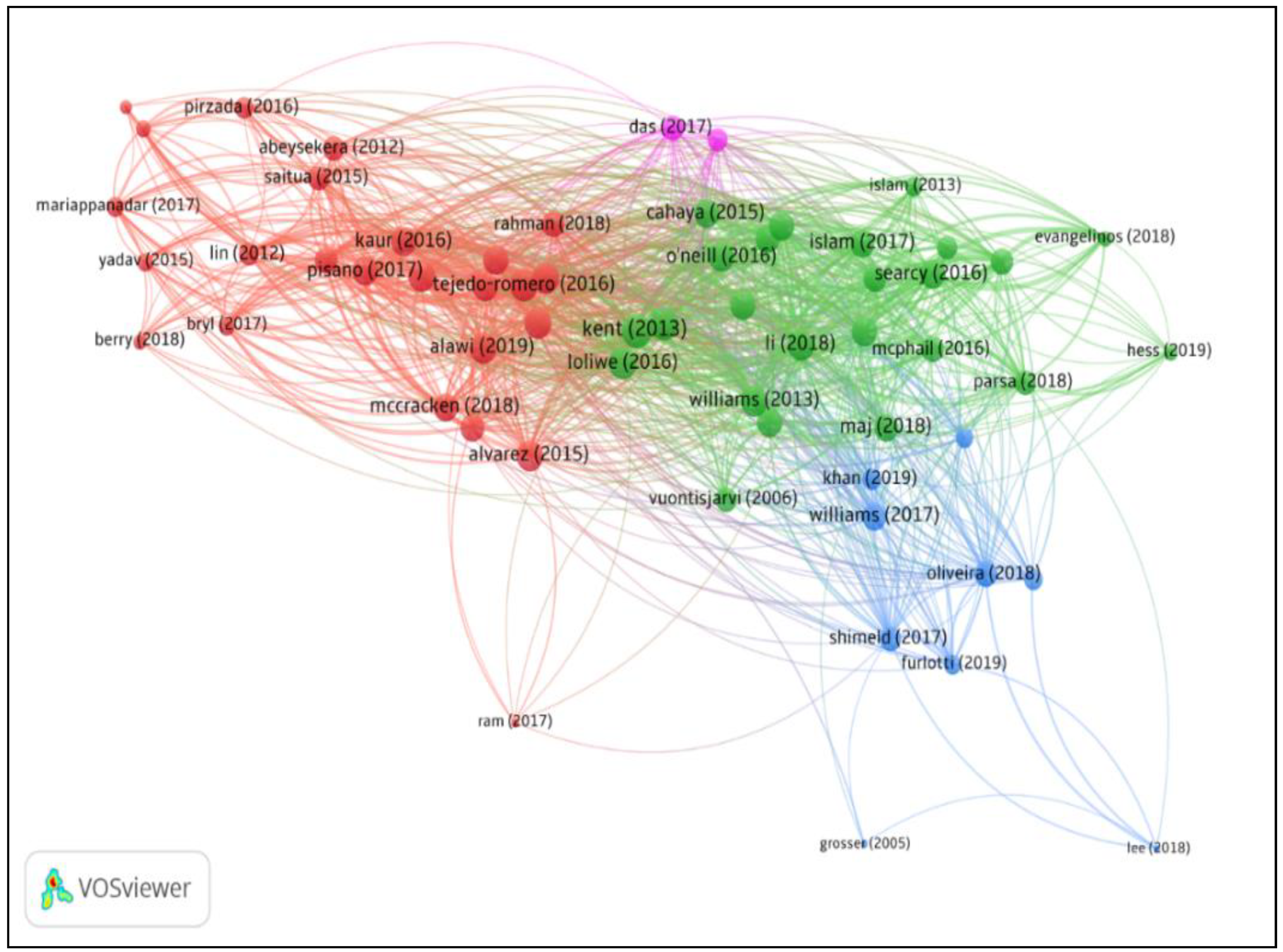

The identification of research subtopics implies using the bibliographic coupling analysis, which employs the number of citation couplings to “quantitatively measure the degree of static connection between the two manuscripts” [55] (p. 271). This analysis ponders the total links. It should be noted that 2 out of the 63 publications in the network are not connected to each other, i.e., the papers written by de Roo [56] and Kawashita and colleagues [51]. Thus, the largest set of connected papers consists of 61 publications. Figure 5 depicts the bibliographic coupling analysis of the publications on employee-related disclosure, based on total links.

As shown in Figure 5, the bibliographic coupling analysis generated three main clusters (each one represented by a different color: red, green, and blue). In this regard, according to van Eck and Waltman [50] (p. 1062), the “clusters that are located close to each other tend to be strongly related in terms of citations, while clusters that are located further away from each other tend to be less strongly related”. Furthermore, “the curved lines between the clusters also reflect the relatedness of clusters, with the thickness of a line representing the number of citations between two clusters” [50] (p. 1063).

Additionally, in purple, we identify two papers carried out by Das [42]) and Frangieh and Yaacoub [57], which were published in the journals Pacific Business Review International and Social Responsibility Journal. Although the fact that two articles address the same topic is not enough to talk about a cluster, it is worth pointing out that both papers analyze human resource disclosures in corporate reports stressing their variety and the associated lack of overall comparability. Specifically, they compare the degree of application of the ILO’s labor standards and human resource management practices among companies based on their employee-related disclosures, as well as the characteristics of such disclosures to detect common trends and discrepancies and, consequently, such papers use an international sample.

For each cluster, we identified the following research subtopics:

Cluster 1 (color red)—Extent, quality, and drivers of human resource disclosures: It is made up of 26 papers that analyze the quantity and/or quality of human resource (HR) disclosures in corporate reports and seek to identify the internal and external factors that influence the level/quality of HR disclosure, mainly from a stakeholder perspective. Thus, papers in this cluster assess the status (extent and/or quality) of employee-related disclosure in a country or region, or the association between the level of disclosure and several organizational and institutional characteristics (such as company size, ownership structure, firm strategy, industry affiliation, organizational culture, national legal system, etc.). Research interest in this subtopic could be explained by the influence of prior studies on environmental disclosure, as well as the desire of knowing the actual state-of-art with regard to employee-related disclosure.

Within this cluster, the articles with the most links are those from Tejedo–Romero and Araujo [58], Tejedo–Romero and Araujo [59], Petera and Wagner [60], Bordunos and Kosheleva [61], Alawi and Belfaqih [62] and Alvarez [63]. Furthermore, in this analysis, we verify that Rahman et al.’s [64] article is also strongly linked with the subtopic corresponding to Cluster 2.

In total, 19 papers belonging to this cluster were written by multiple authors, whereas there are 7 single authored publications. The authors with more papers published on this subtopic are Tejedo-Romero, Araujo, and Rahman, with 2 papers each. The Pacific Business Review International is the journal with more publications on this subtopic (3 papers), followed by the Business Research Quarterly, Social Responsibility Journal, Asian Review of Accounting, and Asian Journal of Accounting and Governance (with 2 papers each).

The first article on this subtopic was published in 2009, and the year with more publications related to this subtopic was 2017 (7 papers). Almost all of the papers belonging to this cluster were published between 2015 and 2019 (only three papers were published before 2015), and more than a half of them were published during the last three years (2017, 2018, and 2019). Accordingly, it can be said that research interest in this subtopic is very current.

The most analyzed countries in this cluster are India (5 papers), Spain (4 papers), and Australia (3 papers), whereas the authors most involved in this subtopic belong to organizations (universities) from Australia (5 papers), Spain (4 papers), India (4 papers), and Malaysia (4 papers).

Table 3 shows the papers belonging to this cluster ordered by total links (i.e., the link between papers), including the journal in which the papers have been published, and the studied country or region.

Cluster 2 (color green)—OHS disclosures, human rights disclosures and employee-related disclosures as a legitimization tool: It is made up of 23 papers. Overall, this group of papers assesses the extent to which companies disclose information on OHS issues (e.g., policies aimed at achieving a good and safe working environment and the well-being of the employees, accidents, injury rates, employees exposed to pollution), as well as human rights (e.g., employment conditions, social protection, avoidance of forced or compulsory work, work-family balance). Furthermore, papers belonging to this cluster analyze voluntary disclosure of employee-related information by companies as a means to maintain/repair legitimacy (e.g., in response to adverse publicity or to incidents) or to send a signal to influence external perceptions about the appropriateness of their human resource management practices.

Research interest in this subtopic could be a response to increasing concerns on working conditions and labor rights in global value chains [14], as well as the relevance acquired by social movements for the promotion of civil rights, equality, and social justice [80]. Similarly, this research line has also been boosted by the interest in knowing the underlying reasons behind employee-related disclosure, in light of the use of CSR disclosure as a tool to improve the image and reputation of companies and the increase in “CSR-washing” practices [81].

Within this cluster, the articles with more links are Vuontisjärvi [8], Kent and Zunker [9], Kent and Zunker [82], Loliwe [39], and Li et al. [21]. In total, 17 papers were written by multiple authors, whereas there are 6 single authored publications. The author with the most papers published on this subtopic is Cahaya, with 3 papers, whereas 14 authors have published 2 papers on this subtopic (Adams, Brown, Dixon, Islam, Kent, Muller-Camen, Nikolaou, Neumann, Parsa, Porter, Searcy, Roper, Tower, and Zunker). The journals that have published more articles belonging to this cluster are Accounting, Auditing & Accountability Journal and Safety Science (both with 3 papers), followed by Australian Accounting Review (2 papers).

As in Cluster 1, almost all of the papers belonging to this cluster were published between 2015 and 2019, and almost half of them were published during the last three years (2017, 2018, and 2019). The year with more publications related to this subtopic was 2016 (5 papers), although the first paper on these issues was published ten years early (in 2006). The most analyzed countries are Australia (5 papers), Indonesia (3 papers) and Finland (3 papers), whereas 5 articles used an international sample. The authors who are more interested in this subtopic belong to organizations from Australia (10 papers), UK (5 papers), and Indonesia (3 papers).

Table 4 shows the papers belonging to this cluster ordered by total links, including the journal in which the papers have been published, and the studied country or region.

Cluster 3 (color blue)—Diversity reporting: This cluster consists of 10 articles which analyze voluntary human resource disclosures related to diversity and equal opportunities (e.g., employment of women, minorities, and people with disabilities). Research interest in this subtopic could be a response to increasing social concerns on non-discrimination and equal opportunities, as well as the social movements to advance in the recognition and protection of minority rights.

The oldest paper in the sample belongs to this cluster (i.e., the article written by Grosser and Moon published in 2005 [35]. Again, almost all of the papers in this cluster were published between 2015 and 2019, and most of them were published during the last three years (2017, 2018, and 2019). The year with more publications related to this subtopic was 2018 (3 papers). Furthermore, as in Cluster 2, Australia is the most studied country by the papers belonging to this cluster.

In total, 8 papers were written by multiple authors, whereas there are 2 single authored publications. Williams [93], Maj [43], Oliveira et al. [94], Shimeld et al. [95], and Hossain et al. [96] are the articles with more links within this cluster. The journal Corporate Social Responsibility and Environmental Management stands out in this research subtopic, with 2 publications.

Table 5 shows the papers belonging to this cluster ordered by total links, including the journal in which the papers were published, and the studied country or region.

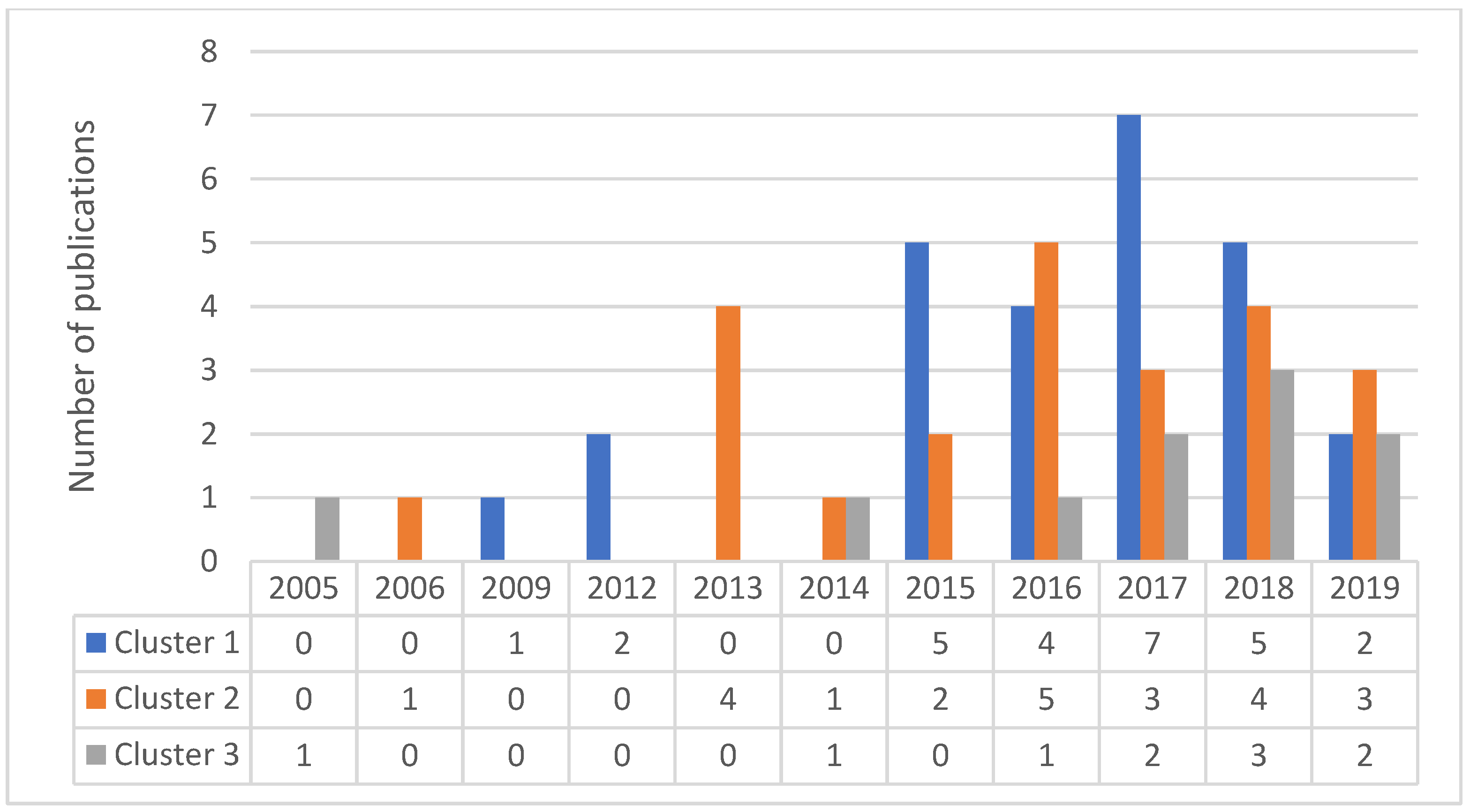

Table 6 and Figure 6 show the temporal evolution of the publications in each cluster. As can be seen, in all clusters most of the papers have been published during the last four years (69.231% in Cluster 1, 65.217% in Cluster 2, and 80% in Cluster 3) and a high percentage of papers have been published in the last three years (69.231% in Cluster 1, 65.217% in Cluster 2, and 80% in Cluster 3). Furthermore, in the case of Cluster 3, half of the articles have been published in the last two years. Thus, it could be said that research interest in all subtopics is very current.

Additionally, when we look at the most recent publications (i.e., those corresponding to 2019), we find that Cluster 1 has 2 articles published in this year (which supposes 7.692% of the total publications in this cluster), Cluster 2 have 3 publications (13.043%) and Cluster 3 have 2 publications (20%).

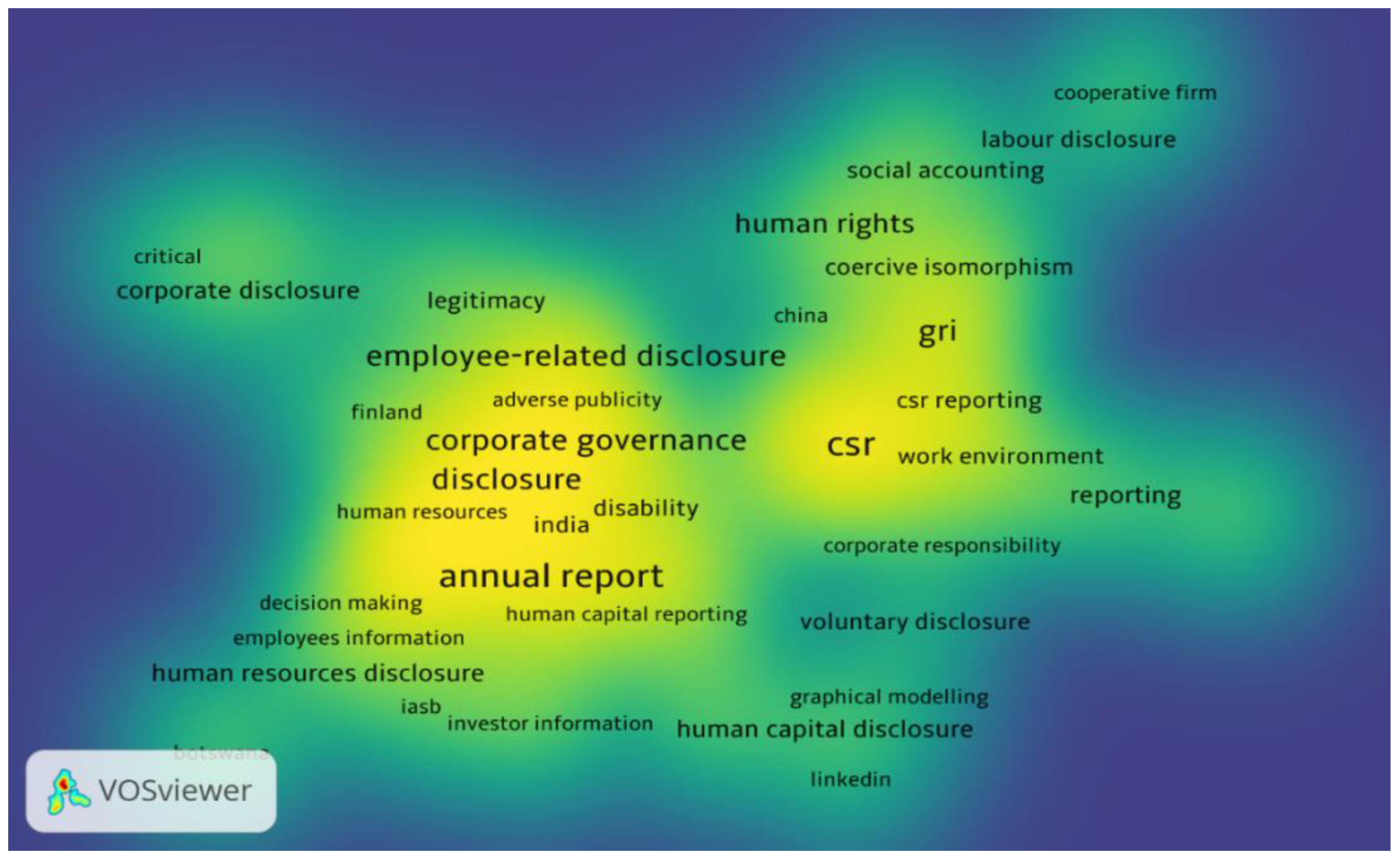

Figure 7 shows the frequency of the major keywords based on the co-occurrence analysis. The most frequent keywords are CSR (total link strength: 49), human capital (total link strength: 50), annual reports (total link strength: 48), content analysis (total link strength: 40), corporate governance (total link strength: 32), disclosures (total link strength: 32) employee-related disclosure (total link strength: 27), and GRI (total link strength: 23).

4.3. Impact of the Published Articles on Employee-Related Disclosure

The influence or impact of the published articles on employee-related disclosure is determined based on citations analysis. As units of analysis, we consider the documents (articles), sources (journals), authors, organizations (authors’ affiliation) and countries.

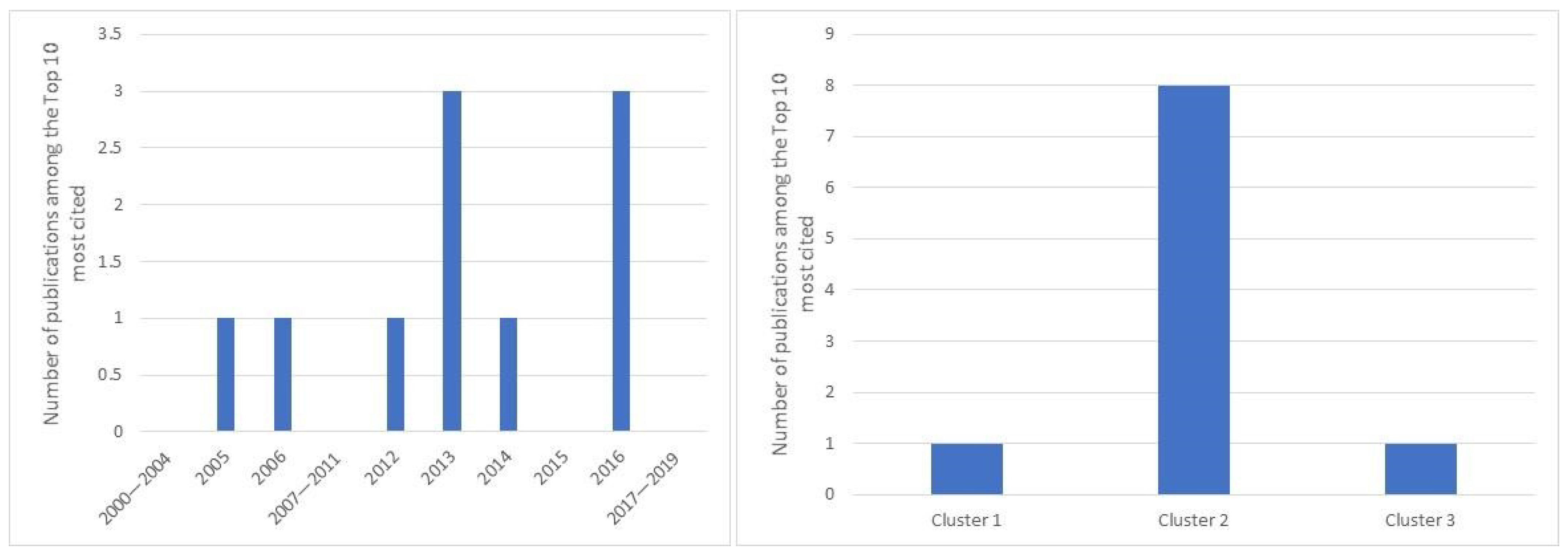

Table 7 shows the top 10 articles on employee-related disclosure in terms of number of citations. As can be seen, the most cited article, with 106 citations, was written by Vuontisjärvi [8] with the title “Corporate social reporting in the European context and human resource disclosures: An analysis of Finnish companies”. It was published by Journal of Business Ethics in 2006 and belongs to Cluster 2 (OHS disclosures, human rights disclosures, and employee-related disclosures as a legitimization tool). The following papers in terms of number of citations are those written by Ehnert et al. [23] and Grosser and Moon [35], with 78 and 69 citations, respectively. The first one, published by the International Journal of Human Resources Management, also belongs to Cluster 2 and analyzes the human resource reporting practices by the world’s largest companies, whereas the latter belongs to Cluster 3 (Diversity reporting). This paper studies the inclusion of gender equality criteria within CSR reporting, and was published by Journal of Business Ethics.

It is worth pointing out that the number of papers written by multiple authors is significantly greater than the number of single authored articles (8 versus 2), although most of the top 10 papers in terms of number of citations were written by two authors (5 papers). The author Carol A. Adams stands out with two papers which are among the top 10 most cited publications. Two journals stand out with more papers among the top 10 in terms of number of citations: Accounting, Auditing & Accountability Journal (3 papers) and Journal of Business Ethics (2 papers).

Furthermore, it should be noted that the two earliest papers of the sample are among the top 10 most cited publications, although there are also three relatively recent articles (published in 2016). Regarding the research subtopics, 80% of the top 10 most cited papers belong to Cluster 2 (OHS disclosures, human rights disclosures and employee-related disclosures as a legitimization tool). Figure 8 depicts the temporal distribution of the top 10 most cited publications as well as their distribution by clusters.

Finally, Table 8 shows the top 10 most cited journals, authors, and countries. As can be seen, the journals with more citations are Journal of Business Ethics (n = 175), derived from 2 articles published in 2005 and 2006—Grosser and Moon [35] and Vuontisjärvi [8]; International Journal of Human Resource Management (n = 91), due to 2 papers published in 2014 and 2016—Kulkarni and Rodrigues [97] and Ehnert et al. [23]; and Accounting, Auditing & Accountability Journal (n = 90), derived from 3 publications, 2 articles published in 2013 to 1 article published in 2016— Kent and Junker [9], Williams and Adams [83], and McPhail and Adams [90]. The remaining journals in Table 8 have less than 50 citations (between 13 and 33 citations). Furthermore, it should be noted that the most cited journals have published articles related to Cluster 2.

As regards the most cited authors, T. Vuontisjärvi clearly stands out (n = 106), with a single authored paper published in 2006 in Journal of Business Ethics, followed by M. Muller–Camen (n= 85), S. Parsa (n= 85), I. Roper (n= 85), with 2 multi-authored papers, published in 2016 in the International Journal of Human Resource Management and in 2018 in Accounting Forum. The remaining top 10 most cited authors have between 43 and 78 citations. Moreover, most of these authors researched on issues related to OHS disclosures, human rights disclosures, and employee-related disclosures as a legitimization tool (Cluster 2). In addition, we found that there is no relationship between the number of citations and the h-index. The authors with the best H-index are J. Moon and C.A. Adams.

It should be noted that, although Australia is the country with the highest number of published articles on employee-related disclosure (n = 17), the UK has a higher number of cited articles (n = 280). Moreover, interestingly, although Austria and Finland are not among the countries with a large number of publications, the 2 papers produced in each country have been highly cited. Conversely, in spite of the relatively high number of publications on employee-related disclosure in some developing countries, such as Malaysia (5 papers) and Indonesia (3 papers), the number of citations that the articles from these countries have received is not significant. Two plausible reasons could explain this issue. Firstly, the average quality attributed to the papers from such countries, compared to those from leading research countries, such as UK and Australia, can limit their citation by other researchers. Secondly, most papers from these countries were published in journals with less research impact (ESCI), which may have also contributed to the low number of citations that they have received.

5. Discussion

A brief summary of the main characteristics of the analyzed papers is provided in Appendix A (i.e., theoretical framework, methodology, sample, objective and main findings). As can be seen, most papers are based on empirical studies, whereas only five papers carried out a theoretical analysis or a literature review. Among the empirical studies, most of them use as research methodology the content analysis technique, which confirms that content analysis of corporate reports is the research method preferred by researchers in social and environmental reporting [100]. Overall, this analysis is focused on annual reports (30 papers), followed by the content analysis of CSR/sustainability reports (13 papers), whereas some studies combine the analysis of several corporate reports (annual reports, sustainability/CSR reports, and integrated reports) with information disclosed on companies’ websites (7 papers), 1 paper analyzes the management report [69] and 1 paper analyzes disclosures released via LinkedIn [64]. Additionally, two papers carry out a “critical discourse analysis” of annual reports i.e., [86,90]. Interviews and surveys are used to a lesser extent (4 papers). In most studies, the type of indicators used to assess the information related to employees are those contained in the GRI’s guidelines/standards e.g., [10,13,18,63], whereas one study uses the ILO’s indicators e.g., [42].

Most empirical studies analyze listed firms (29 papers), although some papers focus on top companies according to the Forbes or Fortune lists or the largest companies (15 papers). Other papers analyze companies belonging to specific sectors (e.g., real state, mining, financial, manufacturing) or specific types of firms (e.g., multinationals, CSR leaders). Five papers are focused on banks and financial entities. The majority of papers (45 papers) are focused on a single country, whereas 6 papers analyze two or more countries, and 7 papers adopt an international perspective. Most studies (34 papers) consider data corresponding to one year, whereas 21 papers analyze data from several years. As regards the focus, some studies look at employee-related disclosures in a general way, while others focus on specific topics such as human capital, OHS, human rights, or diversity.

From a theoretical viewpoint, many studies (14 out of 63) are based on a combination of theories commonly used in CSR research (i.e., agency theory, stakeholder theory, legitimacy theory, institutional theory, signaling theory, and agenda setting theory), while most studies rely on a single theory, standing out stakeholder theory (12 papers), followed by institutional theory (7 papers), and legitimacy theory (6 papers). Nevertheless, in the case of papers belonging to Cluster 2, legitimacy theory is the most used theoretical framework. Other theories used by a minority group of papers are critical theory (2 papers belonging to Cluster 2), gender schema theory (2 papers belonging to Cluster 3), resource dependence theory, prospect theory, Marxist feminist theory, social identity theory and social exchange theory (one paper each). Furthermore, several papers lack a theoretical framework (13 out of 63).

As regards the findings, the studies found that the overall level of employee-related disclosure is low, with an increasing or irregular tendency over time. Furthermore, authors observed that not all items/categories got the same attention by firms. As regards disclosure quality, studies also document a low quality level as a consequence of the lack of consistency and comparability of disclosures, the predominance of narrative disclosures, or the bias towards positive/favorable information. Authors attribute this low disclosure quality to the lack of regulation, as well as low stakeholder pressure.

Many studies aimed to identify the determinants or drivers of employee-related disclosures. In particular, the effect of firm size [23,24,60,64,70,71,87], industry membership [9,17,23,24,52,74,84], government ownership [41,59,70], and board independence [6,41,94] on employee-related disclosures has been analyzed by a high number of studies, which found that such factors are associated with the level or quality of employee-related disclosures. Moreover, many other factors that influence environmental reporting also have an effect on the extent of employee-related disclosures. In this sense, the potential drivers that have been considered by the studies can be separated into four categories (in order of importance):

- -

- Firm-level drivers: this group of factors includes several firm-specific characteristics such as firm size, industry membership, organizational culture, market capitalization, cross-listing, profitability, economic performance, internationalization, and employee power.

- -

- Governance-level drivers: this group of factors includes both corporate governance mechanisms and the firm’s ownership structure. Among the corporate governance mechanisms, special attention is given to the attributes of the board of directors (e.g., board size, board diversity, board independence, and board activity), whereas the drivers related to the firm’s ownership structure include managerial ownership, employee ownership, state ownership, and ownership concentration.

- -

- Country-level drivers: refer to institutional pressures at the country level derived from the national government environment, the country’s level of economic development, national culture, regulatory context, or the country’s level of human rights risks.

- -

- Report-level drivers: refer to whether the firm elaborates non-financial reports.

6. Complementary Analysis

Given the relatively few studies specifically focused on employee-related disclosure that have been published in journals indexed on the WoS database over the last two decades (63 papers), the search was repeated by using the Scopus database. In this case, after applying the same filters that were used in the case of the main analysis, we identified 17 additional papers (Table 9).

In this case, the publications are concentrated between 2004 and 2013, although most of them (10 out of 17) correspond to the last three years of such a period (i.e., 2011, 2012, and 2013). The lack of papers published between 2014 and 2019 should be highlighted as it contrasts with the results of the main analysis in which 84.13% of the papers (i.e., 53 out of 63) were published in such a period.

Nevertheless, some characteristics of this new group of papers are similar to those of the papers included in the main analysis. The number of papers written by multiple authors is significantly greater than the number of single authored articles (11 versus 6). Most papers are empirical studies (16 out of 17), the majority of which adopt the content analysis of annual reports as research method (9 papers) and are focused on listed firms (9 papers). Most papers analyze a single country (13 papers) whereas 3 papers adopt an international perspective. Specifically, 6 papers focus on developing countries—India (2 papers), Brazil, Indonesia, Sri Lanka, and South Africa (1 paper each)—and 7 papers focus on developed countries—Germany and the UK (2 papers each) and Australia, Spain and Sweden (1 paper each).

Although the bibliographic coupling analysis was not used with these papers, after reading them, 12 papers could be identified with Cluster 1, 4 papers could be identified with Cluster 2, and 1 paper would be related to Cluster 3. Thus, similar to the main analysis, most papers belong to Cluster 1.

7. Concluding Remarks

In this study, a bibliometric analysis was carried out on the papers specifically focused on employee-related disclosure published from 2000 to 2019 in journals indexed on the WoS database by assessing the impact of authors, journals, countries/regions, organizations and topics, as well as their temporal evolution in order to systematize the existing research.

We found 63 articles specifically focused on employee-related disclosure, most of them published between 2015 and 2019 (80.95%), 2017 being the most prolific year in terms of the number of published papers. Thus, on the one hand, our analysis shows that relatively few studies specifically focused on employee-related disclosure have been published over the last two decades, compared to the large number of studies on environmental disclosure and/or CSR disclosure [6], which confirms prior statements regarding the limited research attention given to employee-related disclosure in literature (e.g., [1,10,11]). However, on the other hand, we have observed a positive trend in terms of growth of the scientific production on this subject and it could be said that research interest in this topic is current.

We also found that the journals that have published more papers on this subject are Pacific Business Review International and Social Responsibility Journal, followed by Accounting, Auditing & Accountability Journal, Asian Journal of Accounting and Governance, Corporate Social Responsibility and Environmental Management and Safety Science. Although a relatively high number of authors have shown interest in employee-related disclosure, they have not been particularly fruitful, as less than 20% of them have produced more than one paper. Moreover, the number of single authored articles is significantly lower than the number of papers elaborated by multiple authors. F.R. Cahaya is the author with more publications on this subject. Furthermore, Australia is the country that stands out in this research subject.

Bibliographic coupling analysis allowed us to identify three clusters or research subtopics: (1) extent, quality and drivers of human resource disclosures, (2) OHS disclosures, human rights disclosures and employee-related disclosures as a legitimization tool, and (3) diversity reporting. In all clusters, most of the papers have been published during the most recent years of the analyzed period (2016, 2017, 2018 and 2019), confirming that employee-related disclosure is a topic of current interest to researchers. The subtopic with more publications is the first one, although the most cited papers belong to Cluster 2, which ranks second in number of publications.

With regard to the impact of the research, although the majority of the papers were written by multiple authors, the most cited article is a single authored paper written by T. Vuontisjärvi and published in 2006 in Journal of Business Ethics. This journal also has the highest number of citations. Furthermore, the most cited publications were written by authors with affiliation to European organizations.

Additionally, several characteristics of the studies on employee-related disclosure can be highlighted. Most studies are quantitative, using the content analysis technique to analyze corporate reports. Overall, this analysis has been focused on annual reports, CSR/sustainability reports or both. Interviews and surveys are used to a lesser extent. Most empirical studies analyze listed firms from a single country and consider data corresponding to one year. From a theoretical viewpoint, studies on employee-related disclosure have been based on a variety of theories commonly used in CSR research, such as agency, stakeholder, legitimacy, signaling and agenda setting.

Many studies aimed to identify the determinants or drivers of employee-related disclosures. In this sense, many factors that influence environmental reporting also have an effect on the extent of employee-related disclosures. In particular, the effect of firm size [23,24,60,64,70,71,87], industry membership [9,17,23,24,52,74,84], government ownership [41,64,94], and board independence [41,59,70] on employee-related disclosures has been analyzed by a high number of studies.

In conclusion, we could state that the last five years have witnessed an increase in interest among scholars in studying employee-related disclosure as a specific topic of research. Interest in this subject can be explained by the strategic role of a company’s human resources [9,61] and, on the other, it has been stimulated by increasing concerns in working conditions, labor rights and equal opportunities.

However, this research subject is still far from reaching the level of research on environmental reporting and important issues remain to be resolved, both theoretically and empirically. On the one hand, research could be expanded in each of the clusters identified in this study by addressing new issues. Thus, for example, in cluster 1, new organizational and contextual variables could be analyzed by studying their effect both on the overall extent and/or quality of employee-related disclosure and on each of the categories/types of employee disclosures. Similarly, the scope of study in Clusters 2 and 3 could be extended to an international sample instead of focusing on one specific country or region in order to identify trends and drivers of such disclosures. On the other hand, it would be interesting to establish connections among clusters; for example, by identifying under what organizational and contextual characteristics, the employee-related disclosure practices converge/diverge. Furthermore, researchers could also delve more deeply into the effect of employee-related disclosure on the financial and non-financial performance of companies.

To sum up, the growing social awareness in relation to issues related to this subject (for example, employment of women and minorities, social protection, working conditions, etc.) and resulting demands of accountability on companies can promote the development of research in this area [21]. In this sense, by depicting the current status of research on employee-related disclosure, this study’s findings provide a reference frame that could guide researchers regarding the direction of future studies on this subject.

This study is not exempt from limitations. We have included only the WoS database as a source of data collection. Other databases, like Google Scholar and Scopus, should also be considered to analyze research on employee-related disclosure. In order to address this limitation, future studies could extend the sample of research articles by selecting more databases to develop comparative studies based on different databases. Future research may also perform a qualitative analysis to bring about more in-depth knowledge about this research area.

Author Contributions

The whole article is the result of a joint project and shared effort: Conceptualization, A.P.M., B.A.-G. and C.A.-G.; methodology, A.P.M., B.A.-G. and C.A.-G.; validation, A.P.M. and B.A.-G.; formal analysis, A.P.M., B.A.-G., C.A.-G. and M.G.-R.; investigation, A.P.M., B.A.-G., C.A.-G. and M.G.-R.; resources, A.P.M., B.A.-G., C.A.-G. and M.G.-R.; data curation, A.P.M. and B.A.-G.; writing—original draft preparation, A.P.M., B.A.-G. and C.A.-G.; writing—review and editing, A.P.M., B.A.-G. and C.A.-G.; visualization, A.P.M., B.A.-G., C.A.-G. and M.G.-R.; supervision, A.P.M. and B.A.-G.; project administration A.P.M. and B.A.-G. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Xunta de Galicia, grant number GI-2016 (Proxecto de Investigación Consolidación 2020 GPC GI-2016 -Creación de valor sostenible en las organizaciones—CVSO).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Main Characteristics of the Papers

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Cluster 1: Extent, Quality, and Drivers of Human Resource (HR) Disclosure.

| Author(s) | Objective | Theory | Method | Sample | Period | Findings |

|---|---|---|---|---|---|---|

| Abeysekera (2012) | To analyze the influence of two board attributes on human capital (HC) disclosure | Resource dependence theory | Content analysis of annual reports | The top 30 listed firms on the Colombo Stock Exchange | 1998–2006 | The number of independent directors on the remuneration committee and firm size positively affect HC disclosures |

| Absar (2016) | To analyze the quantity and characteristics of HC disclosures | Stakeholder theory | Qualitative content analysis of the annual reports and interviews | The top 20 Bangladeshi and Indian listed companies | 2010/2011 | The overall level of HC disclosure is low and they mostly contain general and positive information. Stakeholders stress the need of higher credibility |

| Alawi and Belfaqih (2019) | To assess the quality of HR disclosures and identify its drivers | Stakeholder theory | Content analysis of annual reports and sustainability reports | 12 Qatari firms from industrial and real estate sectors | 2013–2015 | The quality level of HR disclosure is low and it is influenced by the ratio of employee expenses to total expenses |

| Álvarez (2015) | To assess the extent to which companies comply with disclosure recommendations regarding employees | Legitimacy theory and stakeholder theory | Content analysis of annual reports | 105 Spanish listed firms | 2004 | More attention is paid to social issues about employees than to the ones related to intellectual capital |

| Berry and Jones (2018) | To analyze HC disclosures | - | Qualitative content analysis of the annual reports | 11 Australian volunteer-based emergency services organizations | 2015 and 2016 | Although disclosures recognize the role of volunteers, the HR sections of reports focus on paid staff |

| Bordunos and Kosheleva (2019) | To analyze the effect of HR management systems on the extent, quality, and content of employee-related disclosures | Institutional theory and legitimacy theory | Thematic and content analysis of annual reports | 18 top Russian banks | 2016 | The extent, quality and content of HR disclosures varies among banks. Specific patterns of HR disclosures information are related to different firm characteristics |

| Bowrin (2018) | To analyze the extent and drivers of HR disclosures | Agency theory, signaling theory, stakeholder theory, and legitimacy theory | Content analysis of annual reports, CSR reports, sustainability reports, integrated reports, employee newsletters, and other web-based media | 117 listed firms and selected state enterprises from 6 African and Caribbean countries) | 2011/2012 | The overall level of HR disclosures is low. Organizational culture, firm size, industry membership, national governance environment and foreign influence affect the level of HR disclosure. |

| Bryl and Truskolaski (2017) | To analyze the extent, quality, and drivers of HC disclosures | - | Content analysis of annual reports and other publicly available corporate documents | 30 listed firms on the Warsaw Stock Exchange and 30 listed firms on the Deutsche Börse (Frankfurt) | 2015 | German firms report better than Polish ones. The level of economic development of the country and industry membership affect the level and content of HC disclosures |

| Kansal and Joshi (2015) | To analyze the extent of HR disclosures | Stakeholder theory | Content analysis of annual reports | 82 top firms listed on the Bombay Stock Exchange | 2000–2009 | The overall level of HR disclosures is low, although it increases over the period |

| Kaur et al. (2016) | To analyze the extent and determinants of HR disclosures | - | Content analysis of annual reports | 20 listed Indian firms | 2010/2011 | The overall level of HR disclosures is low or moderate with significant variation among industries. Market capitalization, government ownership, cross list America, the presence of separate HR directors committee, board independence and profit after tax positively affect HR disclosure |

| Lin et al. (2012) | To analyze the effect of HC disclosure on firm performance | Stakeholder theory and signaling theory | Content analysis of annual reports | 660 listed Taiwanese firms | 2006 | HC disclosure positively affects firm performance. Firm size and knowledge intensity moderate such a relationship |

| Maheshwari et al. (2017) | To determine the extent of HR disclosures | - | Content analysis of annual reports | 100 Indian firms listed in S&P BSE 100 | 2009–2014 | A high percentage of companies (85%) disclose HR information. HR disclosures show an increasing trend |

| Mariappanadar and Kairouz (2017) | To examine the relationship between HC disclosure and investors’ investment decisions | Prospect theory and behavioral finance theory | Questionnaire | 250 individual investors in any of the 8 large banks within the Australian Banking Sector Corporation (ABSC) | 2010 | HR capital disclosure has different impacts on investors’ investment decisions |

| McCracken et al. (2018) | To examine the effect of HC reporting regulations on the extent of disclosure | Institutional theory (implicit) | Content analysis of annual reports | The 100 Financial Times Stock Exchange (FTSE) companies | 2012/2013 and 2014/2015 | Regulations on HC disclosure affect the level of disclosure |

| Motokawa (2015) | To analyze the relationship between voluntary HC disclosures and firm profiles | An “integrated” theory of integrated agency theory, stakeholder theory, legitimacy theory, and signaling theory | Content analysis of annual reports | 253 listed firms on the Tokyo Stock Exchange | 2012/2013 | The number of employees and the average salary are positively associated with the amount of voluntary HC disclosures |

| O’Donnell et al. (2009) | To analyze HC reporting and propose an industry-specific reporting model | - | Interviews | Stakeholders (the CEO, managers, directors, and investors) of 3 listed firms belonging to the biotechnology industry | - | HC reporting is in an initial phase, with a focus on operational rather than strategic issues and general rather than industry-specific disclosures. |

| Petera and Wagner (2017) | To analyze the extent and drivers of HR disclosure | Stakeholder theory and legitimacy theory | Content analysis of annual reports | The 50 largest firms in Czechia | 2014 | The level of HR disclosure is low and varies among firms. Quotation and firm size affect the level of HR disclosure |

| Pirzada (2016) | To review of literature on HR disclosure practices | - | Literature review | - | - | - |

| Pisano et al. (2017) | To analyze the relationship between ownership concentration and HC disclosure | Agency theory | Content analysis of information disclosed via LinkedIn | 150 non-financial listed firms from Italy, France, and Germany | 2014 | Ownership concentration negatively affects HC disclosure |

| Rahman et al. (2017) | To analyze the drivers of HC disclosures | Stakeholder theory | Content analysis of annual reports | 48 Malaysian firms | 2010–2014 | Unionization and government ownership as well as firm size positively affect HC reporting |

| Rahman et al. (2018) | To compare OHS disclosure in two countries (Malaysia and the UK) | Stakeholder theory | Content analysis of annual reports | 40 Malaysian listed firms and 40 UK listed firms | 2014 | The OHS reporting practices in both countries are similar. Overall, Malaysian firms report slightly more than the UK ones, although UK firms’ disclosures show higher quality. |

| Ram (2017) | To examine the evolution of HR disclosure practices | - | Content analysis of annual report | Two Indian companies belonging to the mining industry | 2003/2004–2011/2012 | The disclosure level is low and shows an irregular tendency over time, although it decreases from 2003/2004 to 2011/2012 |

| Saitua et al. (2015) | To examine the extent to which HC disclosures comply with regulation on information transparency | Legitimacy theory (implicit) | Content analysis of management report | 23 Spanish listed firms | 2005–2009 | The disclosure level increased initially and then decreased. Firms show a positive image through disclosures. The disclosure pattern is irregular |

| Tejedo-Romero and Araujo (2016) | To analyze the extent and characteristics of HC disclosures | Legitimacy theory and stakeholder theory | Content analysis of annual reports | 23 Spanish listed firms | 2004–2008 | The overall level of disclosure is low. The most disclosed topics are related to employee training and development |

| Tejedo-Romero and Araujo (2018) | To identify the effect of board characteristics on the level of HC disclosure | Agency theory | Content analysis of CSR reports | 23 Spanish listed firms | 2008–2014 | Board gender diversity and board activity positively affect disclosure. A quadratic U-shaped relationship among disclosure and board size board independence, and the ownership concentration; and an inverted U-shaped relationship between disclosure and managerial ownership were observed |

| Yadav and Gite (2015) | To analyze HR disclosure practices | - | Content analysis of the annual reports | 11 Indian commercial banks | 2013/2014 | The overall level of disclosure is moderate. There are no significant differences among public, private and foreign commercial banks |

Table A2.

Cluster 2: OHS Disclosures, Human Rights Disclosures, and Employee-Related Disclosures as a Legitimization Tool.

Table A2.

Cluster 2: OHS Disclosures, Human Rights Disclosures, and Employee-Related Disclosures as a Legitimization Tool.

| Author(s) | Objective | Theory | Method | Sample | Period | Findings |

|---|---|---|---|---|---|---|

| Cahaya et al. (2015) | To analyze the influence of the government on the level labor disclosures | Institutional theory | Content analysis of annual reports | 31 listed firms on the Indonesia Stock Exchange | 2007 and 2010 | The overall level of labor disclosures increases about 8.68% from 2007 to 2010. Government plays an “ambiguous” role |

| Cahaya et al. (2017) | To identify the drivers of voluntary OHS disclosures | Institutional theory | Content analysis of annual reports | 223 listed firms on the Indonesia Stock Exchange | 2007 | Only 30% of firms provide OHS disclosures. Industry membership and internationalization positively affect OHS disclosures |

| Cahaya and Hervina (2019) | To identify the drivers of voluntary human rights disclosures | Stakeholder theory | Content analysis of annual reports | 75 listed firms on the Indonesia Stock Exchange | 2012 | Board size and firm size positively affect human rights disclosures |

| Dixon et al. (2019) | To identify the forces that influence work environment disclosures | Institutional theory | Interviews | 20 CSR managers in Canadian large firms recognized as high CSR performers | The level of disclosure was low due to its voluntary nature and the lack of institutional pressures from the reporting environment. Firms use disclosures to obtain legitimacy | |

| Ehnert et al. (2016) | To compare the level of environmental and HR disclosure, and to identify the organizational attributes that drive the latter | Stakeholder theory | Content analysis of sustainability reports | 138 firms belonging to the Forbes top 250 global companies | 2009 | The overall level of HR disclosure is not lower than that of environmental disclosure. Firm size and industry membership as well as the firm’s origin country (liberal market economies versus coordinated market economies) affect HR disclosure |

| Evangelinos et al. (2018) | To assess the quality of OHS disclosures and to compare | Legitimacy theory | Content analysis of CSR reports | 40 firms from the Forbes World’s Biggest Companies belonging to certain industries | 2014 | Variations in the comprehensiveness of OHS disclosures were found both between and within industries. Chemical firms show a high sensitivity to OHS issues. Western companies scored higher than Middle Eastern and Asian firms |

| Hess (2019) | To examine the potential for transparency programs to improve firms’ human rights performance | Institutional theory and legitimacy theory | Theoretical analysis and review | - | - | Several problems are identified (e.g., the human rights metrics often lack validity or are based upon data that is most easily collected, rather than most important; selective disclosure is documented). A model grounded in regulatory pluralism is recommended |

| Islam and Jain (2013) | To analyze the extent and characteristics of workplace human rights disclosures | Legitimacy theory | Content analysis of the annual reports, social responsibility reports and corporate websites | The 18 major Australian retail and garment manufacturing companies | 2009/2010 | The overall level of disclosure is low. Many items were not disclosed. |

| Islam et al. (2017) | To identify the drivers of voluntary human rights disclosures | Legitimacy theory | Content analysis of the annual reports, social responsibility reports and corporate websites | The top 50 Australian mineral companies | 2010/2011 | The country’s level of human rights risk affects the level of human rights disclosures |

| Kent and Zunker (2013) | To identify the drivers of voluntary employee disclosures | Legitimacy theory, media agenda setting theory, and signaling theory | Content analysis of annual reports | 970 listed firms on the Australia Securities Exchange Limited | 2004 | Corporate governance mechanism, adverse publicity, and industry membership positively affect employee-related disclosure |

| Kent and Zunker (2017) | To identify the drivers of voluntary employee disclosures | Stakeholder theory | Content analysis of annual reports | 970 listed firms on the Australia Securities Exchange Limited | 2004 | Employee power (measured by employee share ownership and employee concentration), the quality of corporate governance (measured by a score based on the board’s attributes, employee recognition in mission statements, and adverse publicity about employees), and economic performance positively affect employee-related disclosures |

| Koskela (2014) | To analyze OHS reporting in different industries | Legitimacy theory | Content analysis of CSR reports | 3 Finish large firms | 2007–2011 | The level of OHS disclosure is low. More similarities than differences in OHS reporting among the companies were observed |

| Li et al. (2018) | To analyze the effect of episodes of employee-related distress on employee-related disclosure | Legitimacy theory and media agenda setting theory | Content analysis of CSR reports | The 4 largest electronic manufacturing services Chinese firms | 2008–2013 | The companies responded to the media coverage on employee-related incidents in different ways in terms of the volume of disclosure |

| Loliwe (2016) | To analyze the characteristics and drivers of voluntary employee disclosures | Stakeholder theory | Content analysis of annual reports | 20 firms listed on the Johannesburg Stock Exchange belonging to the wholesale and retail sector | 2005–2009 | BEE rating is positively associated with employee-related disclosure, whereas managerial ownership is negatively associated with employee-related disclosure |

| Mäkelä (2013) | To critically analyze narrative employee reporting | Critical theory | Critical discourse analysis of annual reports, CSR reports, and CEO’s letters | The 25 largest Finnish firms | 2008 | From the ideology perspective, employee-related disclosures are influenced by the neoliberal and unitarist ideologies |

| Mathuva (2015) | To analyze the drivers of employee disclosures | Legitimacy theory and signaling theory | Content analysis of annual reports | 212 Kenyan savings and credit cooperatives | 2008–2013 | Corporate governance and asset quality positively affect employee-related disclosure, whereas the return on assets negatively affects employee-related disclosure |

| McPhail and Adams (2016) | To critically analyze human rights disclosures | Critical theory | Critical discourse analysis of annual reports, social responsibility reports, and websites | 30 Fortune 500 firms belonging to different industries | 2007/2008 and 2011/2012 | Corporate constructions of human rights are broad |

| O’Neill et al. (2016) | To examine the level and drivers of OHS disclosure | Stakeholder theory and legitimacy theory | Content analysis of annual reports | The largest 50 firms listed on the Australian Stock Exchange | 1997–2009 | Industry membership affect the level and type of OHS disclosures |

| Parsa et al. (2018) | To critically evaluate employee-related disclosure | Legitimacy theory | Content analysis combined with more detailed text analysis of GRI-indexed sustainability reports | 131 transnational corporations listed on the Forbes 250 index | 2011 | Disclosure was motivated by enhancing corporate legitimacy. Firms failed to adhere to the GRI guidelines, which undermines the materiality and comparability of disclosures |

| Searcy et al. (2016) | To analyze the disclosure of quantitative indicators on work environment | Institutional theory | Content analysis of CSR reports | 50 listed firms on the Toronto Stock Exchange and 50 CSR leaders | 2012 | CSR leader disclose a wider amount and variety of indicators than listed firms. Higher emphasis on regulated issues was observed. |

| Tsalis et al. (2018) | To assess the effect of several institutional factors on the quality and the content of the OHS disclosures | Accountability and institutional theory | Analysis of CSR reports by using a scoring system | 134 international firms | 2015/2016 | The quality of the OHS disclosures was very low and is influenced by industry membership, the continent in which companies operate and the OHSAS certification |

| Vuontisjärvi (2016) | To assess the quantity and characteristics (nature) of HR disclosures | Content analysis of annual reports | 160 large Finish firms | 2000 | Disclosures lacked overall consistency and comparability. Quantitative indicators were disclosed by few firms. Not all issues received the same attention | |

| Williams and Adams (2013) | To examine whether employee-related disclosures promote transparency and accountability toward employees | Stakeholder theory, legitimacy theory and political economy theory | Content analysis combined with more detailed text analysis of annual reports | A large UK bank (NatWest) | 1980–1995 | Considerations other than transparency and employee accountability influence employee-related disclosures |

Table A3.

Cluster 3: Diversity Reporting.

| Cluster 3: Diversity Reporting | ||||||

|---|---|---|---|---|---|---|

| Author(s) | Objective | Theory | Method | Sample | Period | Findings |

| Furlotti et al. (2019) | To examine the relationship between the fact that a woman occupies top positions and gender disclosure policies | Gender schema theory | Content analysis of CSR reports | 182 companies listed on the Milan Stock Exchange | 2010–2015 | Women in the position of board chairperson are positively associated with gender policy reporting, whereas women in the position of CEO do not influence gender reporting |

| Grosser and Moon (2005) | To critically analyze how gender equality in the workplace issues are integrated into CSR and the role of stakeholders | Stakeholder theory (implicit) | Theoretical analysis and review | - | - | Several reporting frameworks/guidelines on gender issues were examined. The relatively late and slow progress in gender issues reporting may be related to the lack of ways to stakeholder pressure in this regard |

| Hossain et al. (2016) | To analyze the quantity and quality of gender disclosures | Marxist feminist theory | Content analysis of sustainability reports | 40 Global Fortune firms | 2013 | The level of gender disclosure is low. Disclosures are incomplete and narrative in nature (low quality) |

| Khan et al. (2019) | To assess the quality of disability disclosures | Stakeholder theory | Content analysis of sustainability reports | 274 UK firms | 2015 | Corporate disclosures on disability issues are very low. |

| Kulkarni and Rodrigues (2014) | To examine the characteristics and drivers of disability disclosures | Institutional theory | Content analysis of annual reports | 91 large Indian firms | 2009/2010 | Almost half the sample firms report about disability. Firm age and public/private ownership are associated with disability reporting |

| Lee and Parpart (2018) | To examine how CSR reports depict gendered identities | Gender schema theory | Content analysis combined with more detailed text analysis of CSR reports | 15 South Korean multinational firms listed among the Fortune Global 500 companies | 2015/2016 | The narrative structures of CSR reports reflect the Korean male hegemony |

| Maj (2018) | To analyze the scope and determinants of diversity reporting | Stakeholder theory (implicit) | Survey | 102 firms listed on the Warsaw Stock Exchange | 2016 | The development of non-financial reports is positively associated with the disclosure about diversity |

| Oliveira et al. (2018) | To analyze the influence of country’ institutional and cultural characteristics on gender-related disclosure | Institutional theory (implicit) | Content analysis of annual reports, sustainability reports, integrated reports, reference forms, etc. | 150 Latin-American firms that signed the Declaration of Support for WEP | 2016 | Some characteristics of national culture (i.e., high power distance, individualism, and femininity) negatively affect gender reporting, while the country’s level of economic development and the pressure of unions positively influence gender reporting |

| Shimeld et al. (2017) | To analyze the influence of the issuance of the ASX Corporate Governance Principles and Recommendations on diversity reporting | Agency theory | Content analysis of annual reports | 120 listed firms on the Australia Securities Exchange Limited (ASX) | 2009 and 2012 | The disclosure recommendations have little impact as the changes are superficial |

| Williams (2017) | To analyze the process to change/review the ASX Corporate Governance Principles and Recommendations on diversity reporting | - | Documentary review | - | - | The need of a change in the ASX council’s mindset is stressed to support the inclusion of diversity in the business world |

Table A4.

Remaining Papers.

| Remaining Papers | ||||||

|---|---|---|---|---|---|---|

| Author(s) | Objective | Theory | Method | Sample | Period | Findings |

| Das (2017) | To measure the diversity in labor reporting practices | - | Content analysis combined with more detailed text analysis of annual reports | 49 cooperative firms from the insurance sector | 2014 | Most firms disclose a minimum amount of labor-related information |

| de Roo (2015) | To analyze the effect of the Directive 2014/95/EU on HR disclosure | - | Theoretical analysis | - | - | Despite its shortcomings, the Directive 2014/95/EU on non-financial information can favor HR reporting |

| Frangieh and Yaacoub (2019) | To examine and compare disclosures on socially responsible HR practices | Social identity theory and social exchange theory | Content analysis of reports and websites | 23 of the 25 firms listed on the World’s Best Multinational Workplaces | Most disclosures refer to employee-oriented HR management practices | |

| Kawashita et al. (2005) | To analyze OHS disclosures | - | Content analysis of CSR reports | 416 Japanese listed firms on the Tokyo Stock Exchange | 2004 | About half of the sample companies disclose information on OHS. Manufacturing firms disclose more OHS information than non-manufacturing ones |

References

- Lee, M.D.P. A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead. Int. J. Manag. Rev. 2008, 10, 53–73. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]