When making investment decisions, companies need to be able to compare various investment opportunities. Which ones offer the best value? The first sections of this chapter describe how companies can make such comparisons on a purely financial basis, using the basic investment decision rules of payback period; internal rate of return (IRR); discounted cash flow (DCF); or net present value (NPV) to calculate financial value (FV). We then dive deeper in the calculation of social value (SV) and environmental value (EV). Even with these values known, the big question remains: how to balance them? What decision rules should be followed? We present three approaches to combining NPV with social (S) and environmental (E) factors: (1) the constrained PV (with S & E as a budget); (2) the expanded PV (with SV & EV in monetary values); and (3) the integrated PV (with SV & EV explicitly balanced). In all three approaches F, S, and E all weigh in and can be prioritised—ideally informed by the company’s purpose and value creation profile.

Overview

When making investment decisions, companies need to be able to compare various investment opportunities. Which ones offer the best value? The first sections of this chapter describe how companies can make such comparisons on a purely financial basis. We start out with the basic investment decision rules of payback period and internal rate of return (IRR). Next, we discuss the technique of net present value (NPV) to calculate financial value (FV).

Chapter 5 showed the steps we need to take for calculating social value (SV) and environmental value (EV). Even with these values known, the big question remains: how to balance them? What decision rules should be followed? The NPV approach can be combined with S and E in three ways: (1) the constrained PV (with S & E as a budget); (2) the expanded PV (with SV & EV in monetary values); and (3) the integrated PV (with SV & EV explicitly balanced). In all three approaches F, S, and E all weigh in and can be prioritised—ideally informed by the company’s purpose and value creation profile.

Anzeige

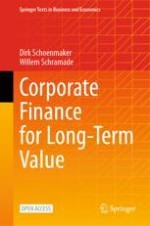

Many companies are keen to integrate SV and EV in their decision making, but struggle to do so in a formalised way. They know that SV and EV are crucial for their purpose, mission, and licence to operate. But their decision-making tools and systems are still geared towards FV only. This chapter provides companies with the basic tools to change this (Fig. 6.1).

4 blocks are labeled sustainable unaware, E S G integrated or inward view, impact or outward view, and integrated value. They have the circles labeled F V, E, and S leading to F V, E V and S V, and F V + E V + S V= I V respectively. They also list a few chapters in the first and the fourth block.

Fig. 6.1

Chapter overview

×

Learning Objectives

After you have studied this chapter, you should be able to:

Calculate the net present value (F) of projects

Apply the payback period and internal rate of return methods

Analyse the interactions between F, S, and E in projects

Apply a balanced approach in integrated present value calculations

Assess the advantages and shortcomings of the different investment decision rules

6.1 Calculating Financial Value by Means of NPV

Managers need an investment decision rule to evaluate projects. Which projects add value to the company and which do not? And if more profitable projects are available, which one should be chosen if capital is scarce? The technique of discounted cash flow (DCF), also known as net present value (NPV), was introduced in Chap. 4. In this chapter, we discuss NPV as a decision-making tool: how to compare the attractiveness of investment opportunities? In Sect. 6.2, we contrast the NPV method with alternatives such as the internal rate of return (IRR) and the payback period criterion. As argued in Chap. 4, future cash flows need to be discounted to take into account the time value of money.

The basic idea is that cash flows are discounted at their opportunity cost of capital (the best available return on an investment of similar risk—see Chap. 4). Suppose that a company is buying new equipment X that requires an initial investment of 100 now and will produce incremental (extra) cash flows of 25 per year for the next 7 years; the opportunity cost of capital r is assumed to be 10%. Table 6.1 provides the cash flow profile, the discount factors \( \frac{1}{{\left(1+r\right)}^n} \) , the present value of the cash flows \( PV=\frac{CF_n}{{\left(1+r\right)}^n} \) , and the NPV calculation—as sum of the present values—of the purchase of equipment X.

Table 6.1

NPV calculation of equipment project X

Year

2022

2023

2024

2025

2026

2027

2028

2029

Cash flow

–100

25

25

25

25

25

25

25

Discount factor

1.00

0.91

0.83

0.75

0.68

0.62

0.56

0.51

PV(Cash flow)

–100.0

22.7

20.7

18.8

17.1

15.5

14.1

12.8

NPV

21.7

Anzeige

Since the present value of future cash flows is higher than the initial investment outlay, the NPV is positive. That means that the purchase of the new equipment is financially attractive. The NPV rule states that investment projects with a positive net present value should be undertaken:

However, it might still not be undertaken if alternatives are better. So, let’s consider buying a rival equipment version Y, which requires an investment of 50, then produces three incremental cash flows of 20 per year and subsequently four cash flows of 5 per year. Like the original equipment project X, this project has a discount rate of 10%. The NPV calculation is shown in Table 6.2.

Table 6.2

NPV calculation of equipment project Y

Year

2022

2023

2024

2025

2026

2027

2028

2029

Cash flow

–50

20

20

20

5

5

5

5

Discount factor

1.00

0.91

0.83

0.75

0.68

0.62

0.56

0.51

PV(Cash flow)

–50.0

18.2

16.5

15.0

3.4

3.1

2.8

2.6

NPV

11.65

Like the first project X, equipment project Y has a positive NPV. Which one is better? Project X has the higher NPV, so if the choice is either project X or project Y, the choice will be to do project X. However, in terms of capital intensity, project Y is more attractive; it offers a slightly better NPV per euro invested: 23.3 cents (=11.65/50) versus 21.7 cents (21.7/100). So, if project Y can be duplicated (and this is a big ‘if’), then doing it twice is superior to doing project X once, since its NPV is 23.3 (see Table 6.3). If capital is readily available, both projects can be done. Example 6.1 gives you an opportunity to calculate the NPV of a hypothetical data centre project for Microsoft.

Table 6.3

Doing equipment project Y twice

Year

2022

2023

2024

2025

2026

2027

2028

2029

Cash flow

–100

40

40

40

10

10

10

10

Discount factor

1.00

0.91

0.83

0.75

0.68

0.62

0.56

0.51

PV(Cash flow)

–100.0

36.4

33.1

30.1

6.8

6.2

5.6

5.1

NPV

23.3

Investments can also be valued in different ways, by looking at the security’s market price (if available) or by means of relative valuation. This involves deriving a project’s or a security’s value from the value of similar investments—see Chap. 9.

Example 6.1: Calculating the NPV of a Data Centre Project

Problem

Consider: Microsoft wants to open a new data centre that has an initial investment outlay of €1.2 billion now; positive cash flows of €50 million in years 1 and 2; and positive cash flows of €500 million in years 3, 4, and 5 when the data centre is fully exploited. The cost of capital of the project is 12%; this is the minimum amount for the data centre to be acceptable to Microsoft and is also referred to as the ‘required rate of return’ or ‘hurdle rate’. The cost of capital reflects the ‘cost’ that Microsoft needs to pay for its capital.

Given the above information, what is the NPV of the data centre project? How much higher/lower would the initial investment outlay have to be (keeping everything else the same) to arrive at an NPV of 0?

Solution

In € millions, the project’s cash flows (CFs) are as follows:

Year

0

1

2

3

4

5

Cash flow

–1200

50

50

500

500

500

With a cost of capital of 12%, the discount factors are as follows:

Year

0

1

2

3

4

5

Discount factor

1.00

0.89

0.80

0.71

0.64

0.57

Multiplying the CFs by the discount factors of the same year results in the following present values (PVs) of CFs:

Year

0

1

2

3

4

5

PV(Cash flow)

–1200

45

40

356

318

284

Summing those PVs of CFs gives an NPV of –€158.1 million. So, the data centre project should not be accepted.

The initial investment outlay would have to be €158.1 lower to arrive at an NPV of 0. After all, since the investment outlay happens now, its discount factor is 1 and every euro reduction in investment outlay translates to an increase in NPV of equal size.

The data centre project will only be accepted with a positive NPV (NPV > 0) according to Eq. (5.1). So, the initial investment should be at least €158.1 lower to be accepted.

6.2 Other Investment Decision Rules

Projects can also be prioritised in ways other than by means of NPV. Two frequently used methods are (1) the payback rule and (2) the IRR (internal rate of return) rule.

6.2.1 Payback Rule

The payback rule has been in use for a long time. It is quite simple: only do an investment if its cash flows pay back its initial investment within a pre-specified period (which is set by company management). The payback period is the number of years needed to earn back the initial investment. In the example of Table 6.1, the payback time of the equipment project is 4 years, since the cash flows of 2023, 2024, 2025, and 2026 are 25 each and add up to 100, which cancels out the investment of 100. Whether that meets the payback rule depends on the payback period pre-specified by management: yes, if the threshold is 4 or more years, and no, if the threshold is set at 2 or 3 years.

The obvious advantage of the payback rule is its ease of use. However, it has serious flaws:

The pre-specified payback period is usually arbitrary

The payback period does not account for the time value of money

It makes cash flows beyond the cut-off point irrelevant, which does not stimulate long-term investment

6.2.2 IRR Rule

The IRR rule is more sophisticated than the payback rule. It says that one should take an investment opportunity if the IRR exceeds the opportunity cost of capital. IRR is the abbreviation of internal rate of return, and it is the discount rate at which a project’s NPV equals zero. This calculation is done with the same information as in an NPV calculation, but without the discount rate, which is left as the variable to be solved for setting the NPV to 0. Table 6.4 illustrates the calculation problem for the earlier equipment project X (from Table 6.1).

Table 6.4

Applying the IRR to equipment project X

Year

2022

2023

2024

2025

2026

2027

2028

2029

Cash flow

–100

25

25

25

25

25

25

25

Discount factor

1

\( \frac{1}{{\left(1+r\right)}^1} \)

\( \frac{1}{{\left(1+r\right)}^2} \)

\( \frac{1}{{\left(1+r\right)}^3} \)

\( \frac{1}{{\left(1+r\right)}^4} \)

\( \frac{1}{{\left(1+r\right)}^5} \)

\( \frac{1}{{\left(1+r\right)}^6} \)

\( \frac{1}{{\left(1+r\right)}^7} \)

PV(Cash flow)

–100

?

?

?

?

?

?

?

NPV

0

With a bit of trial and error (or using the IRR formula in Excel), it is found that r = 0.163, i.e. the IRR is 16.3% in this case. The attraction of the IRR is that it gives an indication of safety: the more the IRR exceeds the cost of capital, the clearer it seems to be value for money. But that may be misleading, since it does not mean much for capital light projects (i.e. projects that do not need much capital). Moreover, the IRR implicitly assumes that interim cash flows can be reinvested at the same return until the end period.

In effect, the IRR is not useful in comparing projects of different sizes. If a small and a large project both have an IRR above the cost of capital, then which one is best? It is not clear. Moreover, the IRR does not give uniform outcomes if cash flows flip signs (i.e. cash flows after the initial investment are alternately positive and negative, like for project A in Table 6.5). Table 6.5 contrasts the cash flows of projects A and B. Figure 6.2 shows the NPVs of these two projects at various discount rates. The IRR is supposed to be found at the unique discount rate for which the NPV is 0. However, for project A, there are actually two points at which the NPV line crosses the x-axis because of the alternating positive and negative cash flows during the project. Hence, there is no unique solution.

Table 6.5

Cash flows for projects A and B

Year

2022

2023

2024

2025

2026

2027

2028

2029

CF project A

–200

110

110

110

–60

110

110

–300

CF project B

–150

30

30

30

30

30

30

30

A line graph plots N P V with no I R R and N P V with clear I R R versus discount rates for projects A and B. For Project A, the N P V with no I R R initially increases to 10% and then declines. For project B, the N P V with clear I R R follows a decreasing trend.

Fig. 6.2

IRR for projects A and B

×

Example 6.2 asks you to calculate the payback period and IRR for Microsoft’s data centre project.

Example 6.2: Calculating Payback Period and IRR of a Data Centre Project

Problem

Consider the Microsoft data centre project described in Example 6.1. With a cost of capital of 12%, its NPV was found to be negative. What does that imply for the data centre’s IRR: should it be higher or lower than 12%? Please calculate the data centre’s IRR and payback period.

Solution

The IRR of a project is the discount rate at which the project has an NPV of 0. Most often (barring exceptions such as shown in Table 6.5), a project’s NPV falls as its discount rate rises. So, if a project’s NPV is negative at a 12% cost of capital, then its IRR will typically be below 12%. This can be checked by inserting alternative discount rates and seeing how the NPV changes. The table below illustrates that and shows that the NPV of the data centre project falls if the discount rate rises from 12 to 13% and rises if the discount rate is lowered:

Discount rate (%)

NPV

13

–192

12

–158

11

–123

10

–86

9

–47

8

–6

7

36

At a discount rate somewhere between 8 and 7%, the NPV turns positive. In fact, with a bit of trial and error it is found that the IRR is just over 7.85%. Because the project IRR is lower than the cost of capital of 12%, the IRR rule suggests that the data centre project should be rejected.

The payback period is found by taking the cumulative positive CFs in each year (i.e. the sum of the positive CFs up until and including that year), and comparing them with the initial investment outlay, as done below:

Year

0

1

2

3

4

5

Cash flow

–1200

50

50

500

500

500

Positive CFs

50

50

500

500

500

Cumulative positive CFs

50

100

600

1100

1600

Investment outlay paid back?

No

No

No

No

Yes

Since the cumulative CFs only exceed (or at least equal) the investment outlay in the 5th year, the payback period of the data centre project is 5 years. To be precise, we can calculate the fraction of the year: the exact payback period is then 4 years and 2.4 months (=100/500 * 12 months).

6.2.3 NPV Versus IRR and Payback

Let’s consider the three methods for the same investment opportunities. Table 6.6 compares the results of the three investment options from Sect. 6.1. As seen previously, equipment project X beats equipment project Y on NPV, but doing project Y twice is best. On IRR and payback, project Y is actually preferred over project X. And doing project Y once or twice delivers the same IRR. This comparison highlights yet another advantage of NPV over IRR or payback period: NPVs can be added up.

Table 6.6

Comparing investment opportunities by method

Method

Project X

Project Y

Project Y twice

Preferred project

NPV

21.7

11.6

23.3

Project Y twice

IRR

16.3%

19.6%

19.6%

Project Y or Project Y twice

Payback rule

4

3

3

Project Y or Project Y twice

The key argument behind the preference for NPV is that it is a direct measure of value created for shareholders (in monetary terms), and that we assume that the objective of the financial manager is to maximise shareholder value (see Chap. 3). We thus want to have the highest NPV, as opposed to the highest IRR (whereby we may end up with a lower NPV).

However, such comparisons only tell us something about the financial value of projects and their ranking. They do not tell us anything about their desirability in social and environmental terms. Moreover, there may be problems with the way people apply them.

6.3 Behavioural Effects on Investment Decisions

In the above discussion of decision rules, it was implicitly assumed that people behave rationally, making unbiased estimates of cash flows and using the correct discount rate. In practice, however, that may not be the case. There is plenty of academic evidence that people often behave irrationally, including in corporate investment decisions. For example, corporate managers are found to sacrifice long-term value in earnings management (Graham et al., 2005). Misvaluation due to such irrational behaviour by corporate managers is called ‘internal errors’, as opposed to ‘external errors’, which is misvaluation due to irrational behaviour by participants in financial markets. There are two main categories of internal errors that can be distinguished: overconfidence and excessive optimism.

Overconfidence means that managers underestimate the risk involved in their investments, resulting in a lower discount rate or hurdle rate for the project. This is a widespread problem. Ben-David et al. (2013) find evidence that most executives underestimate risk, both in the stock market and in their own company’s prospects. This is reflected in narrow confidence intervals: realised market returns are within the executives’ 80% confidence intervals only 36% of the time. The authors find that underestimation of risk results in more aggressive corporate policies: companies with more overconfident managers invest more and use more debt finance. In addition, Malmendier and Tate (2005) find that overconfident managers overestimate their company’s ROIC (Return on Invested Capital) and find external finance too costly.

Excessive optimism involves the overestimation of cash flows. This too is a widespread problem. For a US sample, Graham et al. (2013) find that 80% of CEOs and 66% of CFOs are much more optimistic than average people. Overoptimistic managers invest more when cash is ample since they overestimate the perceived NPVs of projects. But they invest less when external equity is required since the perceived financing costs are too negative (see Chap. 15 on capital structure). In other words, they think they are giving away shares too cheaply (for example, selling shares for €60 while they think their value is €90) and that the losses on the shares are larger than the gains (i.e. the NPV) of the investments to be made.

Example 6.3 illustrates the difference between overconfidence and excessive optimism with a calculation example.

Example 6.3: Calculating Changes in Value Due to Managerial Overconfidence and Excessive Optimism

Problem

Suppose three managers have to assess the same project. Table 6.7 gives their individual estimates of project risk and expected cash flows (CFs), as well as an unbiased assessment of project risk and CFs.

Table 6.7

Project assessment with managerial overconfidence and excessive optimism

Unbiased assessment

Manager A assessment

Manager B assessment

Manager C assessment

Project risk

8%

7.5%

8%

7.5%

Perpetual CF

200

200

220

220

Let’s consider the following questions:

1.

What is the unbiased project value?

2.

How much do managers A, B, and C think the project is worth?

Solutions

Question 1. From Eq. (4.6) (see Chap. 4), we get the unbiased project value for a perpetual stream of cash flows: PV = CF/r = 200/0.080 = 2500.

Question 2. The estimated value for each manager:

Manager A: 200/0.075 = 2666.7

Manager B: 220/0.080 = 2750.0

Manager C: 220/0.075 = 2933.3

Table 6.8 gives an overview of the value effects. It is clear that manager A’s overconfidence (resulting in a lower risk assessment) and manager B’s excessive optimism (resulting in higher CF projection) both lead to a higher estimated project value. Manager C’s combination of the two biases leads to the highest overvaluation.

Table 6.8

Value effects of managerial overconfidence and excessive optimism

Unbiased assessment

Manager A assessment

Manager B assessment

Manager C assessment

Unbiased project value

2500

2500

2500

2500

Estimated project value (with bias)

2500

2667

2750

2933

Overconfidence and excessive optimism often go hand in hand, making them hard to distinguish from each other. So, the source and type of such aggressive corporate policies is not always clear. But there are ways to spot overconfident and excessively optimistic CEOs who conduct aggressive corporate policies: premature liquidation of options, i.e. managers that liquidate options prematurely to finance private transactions (e.g. a new mansion; Malmendier & Tate, 2009); earnings misses and earnings management, which are visible in abnormal accruals (Hribar & Yang, 2016); and excessive press coverage (Malmendier & Tate, 2009). Box 6.1 provides the example of overconfident managers at Enron.

It is also found that CEOs with private pilot licenses (Cain & McKeon, 2016) and those with military experience (Malmendier et al., 2011) tend to be more aggressive. Conversely, female CEOs tend to be less aggressive (Faccio et al., 2016; Huang & Kisgen, 2013), as are CEOs with large cash holdings (Dittmar & Duchin, 2016) and those with deep recession experience (Malmendier et al., 2011).

Box 6.1: Signs of Overconfident Managers at Enron

Energy company Enron went bankrupt in 2001, the largest corporate bankruptcy in US history up until that point. The company went bankrupt after a massive accounting scandal was exposed. Several signs of overconfident managers could be spotted at Enron:

The arrogance of its CEO, Jeff Skilling, was hard to miss: he boasted about his smartness; posted large pictures of himself in the Enron annual report; made wild claims (e.g., ‘perception is reality’). And he was known to be a compulsive gambler

The company had a self-deceiving accounting system: Skilling introduced mark-to-market accounting, which was approved by the auditors and allowed Enron to basically make up its profits (‘hypothetical future value’)

Group processes: employees evaluated each other on a scale of 1–5, where the 1s got huge bonuses and the 5s (15%) were fired—which gave unhealthy incentives in voting

The company had a macho culture with wild motorcycle expeditions and parties with strippers at the office at night and

There was no decent capital budgeting process. For example, the company built a power plant in India without seriously assessing local electricity demand

In addition to excessive optimism and overconfidence, managers may suffer from other behavioural biases. For example, availability bias means that people overweigh available and intuitive information. In confirmation bias, people are looking for support of their opinion, while the more useful thing to do is to look for falsification, i.e. evidence that you might be wrong. Variants on this are wishful thinking, self-attribution, and escalation of commitment. The latter involves people hanging on to projects that should be stopped.

Managers also make behavioural errors in the shape of heuristics. These are rules of thumb that help them to take short-cuts, which may or may not be helpful. An example is the ‘one discount rate fits all’ heuristic: instead of adjusting the discount rate to reflect the risk of the project at hand, managers tend to use one single company discount rate.

6.4 Integrated Investment Decision Rules

Chapter 5 showed how to calculate SV and EV. The next question is how to integrate them in investment decision rules. Chapters 2 and 3 described how a company’s purpose and value creation profile can inform its prioritisation among the types of value. That is the top-down company view. But how to prioritise at the investment project level? The same priorities should hold, but they need to be applied in investment decision rules.

This section therefore develops three ways to prioritise at the investment project level, by combining the PV (present value) approach with S and E:

1.

The constrained PV includes S and E in their own units as a budget constraint to the NPV on purely financial value (FV)

2.

The expanded PV expresses S and E in monetary values (SV and EV) and shows these in addition to the NPV on FV

3.

The Integrated PV goes further by explicitly balancing FV, SV, and EV in a formula

Table 6.9 provides an overview of the PV approaches. In all three approaches, F, S, and E all weigh in and can be balanced. Ideally the balancing is informed by the company’s purpose and value creation profile (see Chap. 2). So if a company is, say, value destructive on E, it should put extra weight on improving E; and if E is central to its purpose, it will also weight E more heavily. The next sub-sections explain the approaches. Box 6.2 discusses how investment decisions are made in practice.

It is important to note that investment decisions (as part of the capital budgeting process that makes a list of investment projects to be done) do not start with an NPV analysis. Instead, several steps are typically taken before an NPV analysis is conducted. See Fig. 7.2 in Chap. 7. S and E issues are increasingly identified before any financial evaluation takes place. Advanced companies adopt high standards and targets for S and E issues, which can effectively exclude certain projects due to insufficient performance on the social and environmental fronts. For example, these companies might have a target of eliminating child labour in their supply chain or a target of being net zero on carbon by 2030.

6.4.1 Constrained PV

In the constrained PV method, S and/or E function as a budget constraint to the standard NPV on F. Typically, such budgets are informed by the company's purpose, strategy, and context. Suppose a medical technology company has the goal of being carbon neutral and wants all of its investment projects to contribute to that goal. The company can choose from three projects, which are listed in Table 6.10 along with their characteristics.

Table 6.10

Comparing projects on constrained PVs

Project

Investment, € millions

NPV F, € millions

CO2 emitted, millions

CO2 stored, millions

NPV ≥ 0?

Contribution to CO2 emissions ≤0?

A

70

–50

0

1

No

Yes

B

100

200

0.2

0

Yes

No

C

20

250

0.2

0

Yes

No

Project A with a negative NPV is an investment in carbon capture and storage. Project B with a large upfront investment has a positive NPV, but uses a carbon-intensive technology. Finally, project C has a smaller upfront investment and a higher NPV and uses a similar carbon-intensive technology.

Project A is valuable in terms of meeting the company’s target of becoming carbon neutral. However, it has a negative standard NPV and hence fails on the constrained PV—which wants both a positive NPV and to have S and E within budget. Projects B and C also fail on the constrained PV criterion, but for the opposite reason of project A: whereas B and C have positive standard NPVs, they fail on reducing the company’s emissions. Hence, all three projects should not be done on a stand-alone basis.

But what about combining projects? Given that project A has opposite strengths to projects B and C, they might be value creative in combination. Table 6.11 shows the characteristics of such combinations.

Table 6.11

Comparing combinations of projects on constrained PVs

Project

Investment, € millions

NPV F, € millions

CO2 emitted, millions

CO2 stored, millions

NPV≥0?

Contribution to CO2 emissions ≤0?

A + B

170

150

0.2

1

Yes

Yes

A + C

90

200

0.2

1

Yes

Yes

Both combinations meet the constrained PV criterion: projects A+B and projects A+C make a net positive contribution to reducing the carbon footprint and have a positive standard NPV. However, they are not the same: the combination of projects A+C is better on standard NPV than the combination of projects A+B. The combined projects are equal on E (the carbon footprint). We can also compare the combination of projects A+C to project B. The combined projects A+C are equal to project B on NPV, but they outperform project B on E.

Another issue is that these combinations are effectively netting the pros and cons of individual projects: project C is harmful to E; and project A has a negative standard NPV. To what extent netting should be allowed is debatable, both in investment decision-making and in reporting. Some netting can be a good thing in that it justifies doing projects that are individually problematic but net positive on aggregate. This enables decision-makers to avoid decision paralysis. However, netting should not be used to make half-hearted decisions. In our example, project A’s carbon capture and storage (with negative NPV) is meant to offset the effects of carbon-intensive projects.

The comparison is further complicated by including S. Since the example concerns a medical technology company, it makes sense to consider the quality life years added by projects A, B, and C. Table 6.12 shows the projects’ profiles.

Table 6.12

Quality life years added per project and combination of projects

Project

Quality life years added

Contribution to health effects ≥0?

A

–

Yes

B

2500

Yes

C

4000

Yes

A + C

4000

Yes

The good news is that two out of three projects add quality life years. For projects B and C, the numbers are quite high, since they relate to the medical technology company’s core business of improving health. Project A, which is essentially an environmental project, brings no health effects. But how to compare these? If the budget constraint is to be positive (or more precisely non-negative), then all three projects meet the criterion. Then again, more quality life years saved is better. So how to account for that? We get one step closer to doing so by means of the expanded PV.

6.4.2 Expanded PV

The expanded PV expresses S and E in monetary values to arrive at SV and EV (as explained in Chap. 5) and then shows these in addition to the standard NPV. For the above-mentioned projects A, B, and C, this can be done by applying a shadow price to both CO2 (at €200 per ton) and quality life years added (at €110,000 per quality life year added). The shadow prices are taken from Sect. A.1 of Chap. 5. Tables 6.13 gives the results.

Table 6.13

Comparing projects on expanded PVs

Project

Investment, € millions

NPV F, € millions

E in own units

net CO2 reduction, millions of tons

EV (€ millions)

net CO2 reduction at 200 Euro/ton

S in own units

quality life years added

SV (€ millions)

quality life years added at 110k euro/life

A

70

–50

1.0

200

–

0

B

100

200

–0.2

–40

2500

275

C

20

250

–0.2

–40

4000

440

A + C

90

200

0.8

160

4000

440

Note: The table shows the present value (PV) of financial flows in the third column (NPV F = FV), environmental flows in the fifth column (EV), and social flows in the seventh column (SV). To keep the exposition simple, a zero discount rate is used for calculating the PV of EV and SV

Table 6.13 shows that, while project A has a zero SV and a negative FV, it has a high EV. In contrast, it is now clearer that projects B and C have negative EV, but high FV and even higher SV. Moreover, the combination of projects A and C now looks much better than that of the individual projects: the combination is strongly positive on all three value dimensions.

So by going from S and E to SV and EV, the comparability of projects and project combinations has gone up. However, it did require adding a shadow price which may be hard in other cases (such as biodiversity). And which shadow price to use? On the one hand, one could argue that the €200/ton shadow price of CO2 is high. versus the current market price (of about €100/ton in early 2023). On the other hand, it is very low versus estimates by scientists on what is needed to reach net zero. And the €110,000 shadow price on a quality life year effectively gives SV a high weight vs. EV. The above example is also quite simplistic, as other types of SV and EV (such as health and safety; and biodiversity) are not included. It also ignores potential loss of life from environmental degradation.

Moreover, while we did consider SV and EV at the same level as FV, we did not explicitly prioritise among the three types of value. That is what we do in an Integrated PV, abbreviated as IPV.

6.4.3 Integrated PV (IPV)

In the integrated PV (IPV), SV and EV are not only separately calculated (as in the expanded PV), but also added and weighted, along with the NPV, to arrive at an integrated value creation number. In its simplest form, we sum all types of value at equal weights. The simple integrated present value decision model then becomes:

$$ IPV= FV+ SV+ EV>0 $$

(6.2)

The application of the integrated present value decision model is similar to the net present value rule in Eq. (6.1). Companies should only undertake projects that have positive integrated value. Among projects with positive integrated value, the company should first undertake the project with the highest integrated value. But as explained below, a company should avoid conducting projects whereby a positive FV outweighs negative SV and EV. Table 6.14 gives this simple IPV for the above-mentioned projects.

Table 6.14

Integrated PVs when equally weighting FV, SV, and EV

Project

FV

SV

EV

IPV = FV + SV + EV

A

–50

0

200

150

B

200

275

–40

435

C

250

440

–40

650

A + C

200

440

160

800

Note: The table shows the present value (PV) of financial flows in the second column (FV), social flows in the third column (SV), environmental flows in the fourth column (SV), and the integrated present value in the fifth column (IPV)

Table 6.14 calculates integrated value by simply summing FV, SV, and EV. But integrated value can also be calculated not just by adding values, but also by balancing them (Schramade et al., 2021). For example, SV might get a higher weight if the company has a mission focused on S or if its SV value creation profile is negative. We can apply different regimes, with b denoting the weighting of SV; and c denoting the weighting of EV. We only need two parameters to design relative weights for all three value dimensions, because the effective weight for FV is 1. The equation for calculating the IPV is as follows:

The IPV model acknowledges the interrelationships between the different types of value and allows a structured balancing of stakeholder interests. Chapter 3 argues that the current corporate governance regime is characterised by very small weighting of social and environmental value: b = c = 0.1. This is quite close to the shareholder model, whereby FV is prioritised over SV and EV. The weights should be set by the company’s board (see Chap. 3). The board’s choice of weights depends not only on a company’s purpose and mission, but also on the speed of internalisation of negative impacts. Companies may want to improve their competitive position by including social and environmental value in their business model ahead of expected internalisation of negative impacts (see Chap. 5). The IPV model allows companies to choose their degree of sustainability. Here, we explore the intermediate case (b = c = 0.5) and the full case (b = c = 1) of including SV and EV.

Table 6.15 lists several projects. Project K is profitable and has negative social and environmental impact. Project L is less profitable, with positive social impact and negative environmental impact. Project M is again less profitable with improved social impact, but still negative environmental impact.

Table 6.15

Integrated PVs with intermediate and full weighting of SV and EV

Project

FV

SV

EV

IPV = FV + 0.5 * SV + 0.5 * EV

IPV = FV + SV + EV

K

50

–50

–20

15

–20

L

30

30

–40

25

20

M

10

60

–40

20

30

From a financial perspective using the NPV rule (b = c = 0), the company chooses project K with the highest FV. Using the IPV rule, the company selects project L in the intermediate case (b = c = 0.5) and project M in the full case (b = c = 1) as the project with the highest IPV. This hypothetical list of projects shows that the weighting of SV and EV matters. Project M has the highest combined SV and EV (+20 = 60 – 40) in comparison with project K (–70) and project L (–10). Box 6.3 illustrates the operation of the IPV decision model with a real-world example of Shell, a major oil company.1 By applying the NPV model, Shell continued its current oil and gas activities. Using the IPV model, by contrast, would stimulate Shell to invest in green activities, making its business model more future-proof.

Box 6.3: Shell Lost in Transition

Oil company Shell has a negative environmental value because of the carbon emissions of its main products, oil and gas. This negative environmental value outweighs its positive financial value (profits). Investment in green energy companies, with simultaneous divestment of the exploration of new oil and gas, can reduce this negative value. An opportunity to do that was provided by the possible acquisition of Eneco, an energy utility company with a green strategy, in 2019.

With the IPV model, Shell would have arrived at a relatively high valuation of Eneco, because Eneco would reduce Shell’s negative environmental value (which outweighs its positive financial value). However, Shell applied the traditional NPV model, resulting in a low valuation of Eneco. As a result, Japan’s Mitsubishi was able to acquire Eneco with a higher bid, and Shell continued to focus its investments on oil and gas exploration.

Upgrading Legacy Investments

The IPV rule optimises all new investments based on the company’s preferences b and c for SV and EV, respectively. But what about past projects with negative SV and EV? Are there legacy investments that locked the company into carbon-intensive production processes and products or negative social practices? They need to be upgraded with new investments, even if it means that the standard NPV of these investments is negative (De Adelhart Toorop et al., 2023).

In the Appendix, we develop an extended IPV model, in which negative values should ‘hurt’ more than positive values of the same size. This gives companies an incentive to phase out negative (social and environmental) impacts, thus creating positive value on all three dimensions in the long term. The Appendix provides some company case studies on the working of the extended IPV model.

Limits

There are also limits to the use of the IPV decision model. An important limit is the availability of company data on social and environmental impacts. Mandatory reporting of sustainability data, as envisaged by the International Sustainability Standards Board and the European Union’s Corporate Sustainability Reporting Directive, will advance data availability (see Chap. 17). Another (and related) limit is the advance of impact valuation. Further progress is needed in the valuation practices of social and environmental impact in order to include the quantified impacts in investment decision-making.

6.5 Internalisation

In the previous section FV, SV and EV were calculated independently, which gives the impression that they are also created independently from each other. In practice, the three dimensions are created jointly and with similar drivers. The same processes that allow an airline to make money selling flights also result in GHG emissions, poor (or good) working conditions, and other S and E effects. The effects are related and can affect each other. Improving one of them may have a cost or benefit for the other—now or later, or now and later. This makes that taking a dynamic perspective is very important: do not assume that current conditions will last forever, but acknowledge that they can change in various ways.

Industries, companies, and products that are currently loss-making because they do not get paid for the positive externalities they generate, may become profitable as those externalities get priced (internalised). Conversely industries, companies, and products with large negative externalities face the risk of those externalities being (partly) internalised by means of regulation, technology, or customer behaviour. The example of the car industry was mentioned in Chap. 2: emission limits (regulation) and the arrival of Tesla (technology & customer behaviour) forced automobile makers to start switching from cars with internal combustion engines to electric vehicles and incur the high costs required to adapt.

Let us illustrate internalisation with the IPV examples presented in Table 6.16. The company applies an intermediate regime (with b = c = 0.5) for its IPV calculations. Project X has a positive IPV of +45, while projects Y and Z have negative IPVs of –15 and –35, respectively. Only project X would be undertaken.

Table 6.16

IPV of various projects

Project

FV

SV

EV

IPV = FV + 0.5 * SV + 0.5 * EV

X

80

–20

–50

45

Y

–20

–30

40

–15

Z

–40

–50

60

–35

There is a possibility that the government imposes a carbon tax of €150, which amounts to 75% of the environmental value (based on the shadow carbon price of €200 per ton). In this internalisation scenario, FV absorbs 75% of EV due to carbon taxation (assuming that all EV is related to carbon emissions). Table 6.17 shows how FV changes. The (partial) internalisation of EV makes project X financially less attractive, but still value creative. More importantly, the internalisation means that projects Y and Z become financially viable on a stand-alone basis. This happens regardless of the regime at the company, as shown in Table 6.17, which gives the new FVs and the IPVs for the intermediate regime (with b = c = 0.5) from Table 6.16.

Table 6.17

Internalisation scenario: FV absorbs 75% of EV

Project

FV (old)

SV

EV

FV (new) = FV (old) + 0.75 * EV

IPV with internalisation

IPV without internalisation

X

80

–20

–50

42.5

7.5

45

Y

–20

–30

40

10

15

–15

Z

–40

–50

60

5

10

–35

Note: This table is based on Table 6.16 and shows the internationalisation scenario for IPV with intermediate weighting: IPV = FV + 0.5 ∗ SV + 0.5 ∗ EV

Carbon taxes or prices enter the valuation twice—for calculating FV and EV. The taxation incentivises the company to change behaviour and switch to low-carbon or carbon-neutral technologies reducing the negative EV. In the case of the company reducing carbon emissions, FV improves (by avoiding costly carbon taxes) and EV improves (by reducing carbon emissions). This then should not be seen as double counting. Table 6.17 shows that projects Y and Z become more attractive due to their improved FV and positive EV, and project X becomes less attractive due to its reduced FV and negative EV.

So, even the manager who gives EV an intermediate weighting (with c = 0.5) is now interested in doing projects Y and Z, in which FV derives from its high EV. However, the manager’s interest will depend on the probability of this happening. Table 6.18 shows how the expected IPV of project Y increases with the probability of internalisation. This is not to be confused with the probability of transition (Chap. 2). The probability of internalisation is a narrower concept that estimates to what extent externalities are likely to be translated into FV effects, driven by transition processes.

Table 6.18

Expected IPV of project Y under varying probabilities of internalisation

IPV with internalisation

Probability of internalisation (%)

IPV without internalisation

Probability of no internalisation (%)

Expected IPV

15

0

–15

100

–15

15

10

–15

90

–12

15

20

–15

80

–9

15

30

–15

70

–6

15

40

–15

60

–3

15

50

–15

50

0

15

60

–15

40

3

15

70

–15

30

6

15

80

–15

20

9

15

90

–15

10

12

15

100

–15

0

15

Table 6.18 can be read as follows: In our example, the probability of internalisation means the probability of the government imposing a carbon tax of €150. Looking at the top rows, this probability of internalisation in column 2 is quite low (0%, 10%, etc.). The counterpart is the probability of no internalisation in column 4. Note the two probabilities add up to 100% by definition. The expected IPV is the weighted average of the IPV with internalisation and the IPV without internalisation, with the respective probabilities as weights. For example, in the case of a probability of internalisation of 20%, the expected IPV is −9 = 15 ∗ 20 % − 15 ∗ 80%.

At a probability of 50% or higher, the expected IPV of project Y turns positive in Table 6.18. Of course, this is a stylistic example. In the real world, internalisation can happen in many different ways (e.g. over different time horizons), making the calculation much more difficult. However, a rough calculation like this one can be very helpful in assessing the attractiveness of projects and in helping to make better decisions. In Chap. 7, we provide some real-life examples and calculations with the IPV decision model.

6.6 Conclusions

The previous chapters described the importance of balancing the various types of value; how that affects corporate governance; and how to discount future flows. This chapter takes the necessary next step: how to calculate those types of value.

When making investment decisions, companies need to be able to compare various investment opportunities. Which ones offer the best value? The first sections of this chapter describe how companies can make such comparisons on a purely financial basis. We start out with the traditional technique of net present value (NPV) to calculate financial value (FV). Next, we discuss the contrast with other investment decision rules such as payback period and internal rate of return (IRR).

Chapter 5 showed the steps to be taken for calculating the social and environmental value in monetary terms, i.e. SV and EV. Even with these types of value known, the big question remains how to balance them. What decision rules should be followed? The NPV approach can be combined with S and E in three ways: the constrained PV (with S & E as a budget); the expanded PV (with SV & EV in monetary values); and the Integrated PV (with SV & EV explicitly balanced).

In all three approaches, F, S, and E all weigh in and can be prioritised—ideally informed by the company’s purpose and value creation profile. It is important to take a dynamic perspective to these types of value: internalisation can happen, thereby shifting EV or SV to FV in positive or negative ways. This chapter showed how this can be done when quantities are given. But to make it more practical, the next chapter goes further by discussing the fundamentals of getting the right data and line items to estimate value flows per year.

Key Concepts Used in This Chapter

Constrained PV (present value) includes S (social) and E (environmental) factors in their own units as a budget constraint to the NPV on financial value

Excessive optimism involves the overestimation of cash flows

Expanded PV (present value) expresses S (social) and E (environmental) factors in monetary values (SV and EV) and shows these in addition to the NPV on financial value

Integrated PV (IPV) calculates and explicitly balances FV, SV, and EV in a formula

Internal rate of return (IRR) says that one should take any investment opportunity in which the IRR exceeds the opportunity cost of capital

Investment decision rules are decision rules for investment projects; examples of such rules are NPV, IPV, payback rule, and IRR

Materiality indicates relevant and significant information

Materiality assessment aims to determine which S (social) and E (environmental) factors are sufficiently important for consideration in SV and EV

Monetisation of social value (SV) and environmental value (EV) means to express them in monetary terms

Net present value (NPV) is the present value of cash inflows and cash outflows

Payback rule states that one should only do an investment if its cash flows pay back its initial investment within a pre-specified period

Payback period is the number of years needed to earn back the initial investment

Overconfidence means that managers underestimate the risk involved in their investments

Shadow prices reflect the ‘true scarcity’ of resources to stay within planetary boundaries or the ‘true price’ of human rights breaches to stay within social boundaries; shadow prices are based on welfare theory

Quantification of social and environmental factors means to express them in their own units

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Appendix: Extended IPV Model with Company Case Studies

This Appendix introduces an extended version of the IPV model of Sect. 6.4 and provides company case studies on applying this model.

A.1 Extended IPV Model

In Sect. 6.4, the IPV model was introduced as follows:

$$ IPV= FV+b\cdot SV+c\cdot EV>0 $$

(6.4)

The IPV rule optimises all new investments based on the company’s preferences b and c for SV and EV, respectively. But what about past projects with negative SV and EV? Old investments, that locked the company into carbon-intensive production processes and products or negative social practices, need to be upgraded with new investments (De Adelhart Toorop et al., 2023).

This implies that negative values should ‘hurt’ more than positive values of the same size. Discouraging, but not banning, negative effects on one of the value dimensions is possible with parameter d > 1 for negative values. Companies then have an incentive to phase out negative (social and environmental) impacts and thus create positive value on all three dimensions in the long term. The extended IPV decision model then becomes:

The superscript +/– stands for a positive/negative value, respectively. For FV, we get either an overall positive value FV+ or an overall negative value FV−, since cash flows are fungible (i.e. they can be netted). For SV and EV, we can get both positive and negative values at the same time. Clothes, for example, can contribute to consumer well-being SV+, while being produced under poor labour conditions SV− (see calculations for Inditex in Chap. 11). It is important to account for positive and negative social and environmental values separately. This prevents netting of positive values, such as customer well-being, and negative values, such as poor labour conditions.

We propose to start with a parameter for negative value of one and a half: d = 1.5. Companies that aim to phase out a negative value faster will set the weight of d higher. In the long run, the weight of d may go to infinity, which is de facto a ban on negative social and environmental externalities.

A.2 Company Case Studies

We provide some company case studies on the working of the extended IPV model, which may lead to different decisions on corporate investments. To analyse potential differences, the extended IPV model in Eq. (6.5) is applied to two hypothetical companies: an oil company and a medical technology company. The simple IPV model with adding up of the three value dimensions (with a weight of 1 for all three value dimensions) is also presented as benchmark.

Table 6.19 shows the valuation creation profile of the companies. The value profile of the oil company is typical for the sector: moderately profitable (FV = 3), but with major environmental externalities due to carbon emissions (EV = − 15) and some social externalities in the supply chain (SV = − 2). The company has no explicit purpose and thus applies equal weights across the value dimensions (b = c = 1), which already goes well beyond how the typical oil company is currently managed (with values for b and c close to zero). A simple adding up delivers a negative value profile (IV = − 14). Using the extended IPV model, however, delivers a larger negative annual value creation profile (IV = − 22.5), as the negative impact of the polluting oil company counts 1.5 times (d = 1.5).

Table 6.19

Value creation profile of an oil and a medtech company

Value dimensions and parameters

Company 1: Oil

Company 2: Medtech

FV

3

8

SV

–2

15

EV

–15

–2

Annual value creation by simple adding up

–14

21

b

1

1.6

c

1

1

d

1.5

2

FV+

3

8

b ∙ SV+

0

24

c ∙ EV+

0

0

d ∙ FV−

0

0

d ∙ b ∙ SV−

–3

0

d ∙ c ∙ EV−

–22.5

–4

Annual integrated value creation

–22.5

28

Note: This table shows the value creation profile of two companies based on three value dimensions (FV, SV, EV). The oil company has equal weights for the value dimensions (b = c = 1), while the medtech company has higher weights for SV (b = 1.6) than for EV (c = 1) and FV (1). In the extended IPV model (rows 7–12), negative values count 1.5 times (d = 1.5) for the oil company and double for the medtech company (d = 2) in the value creation. The top rows show annual value creation by a simple adding up of the three values (rows 1–3)

The medtech company is strong on its mission of health care (SV = 15) and profitable (FV = 8), but does generate negative environmental externalities (EV = − 2), albeit much smaller than those of the oil company. The medtech’s purpose is reflected in the higher weight for SV (b = 1.6) than for EV (c = 1) and FV (1 by definition). The medtech company wants to phase out its negative values as fast as possible (d = 2). The extended IPV model shows a large positive value creation profile (IV = 28), due to the higher parameter for its social mission. A simple adding up gives a smaller positive value profile (IV = 21).

Table 6.20 summarises the investment projects available for the oil company. Projects 1 and 2 have positive impact on the social side (+2) and the environmental side (+2), respectively, but make financial losses (–1). Project 3 generates a profit (+1) with no externalities. We first analyse the choice of projects on a stand-alone project base, i.e. irrespective of the company’s current value creation profile. The NPV rule would select project 3 with the highest financial value, which is positive (+1). Punishing negative values in the extended IPV model leads also to project 3, which has no negatives. The simple adding up sees no difference among the projects, they all create a value of +1.

Table 6.20

Change in value creation by an oil company

Value dimensions and parameters

Oil company profile

Project 1

Project 2

Project 3

Company after project 1

Company after project 2

Company after project 3

FV

3

–1

–1

1

2

2

4

SV

–2

2

0

0

0

–2

–2

EV

–15

0

2

0

–15

–13

–15

Annual value creation by simple adding up

–14

1

1

1

–13

–13

–13

Improvement

1

1

1

b

1

1

1

1

1

1

1

c

1

1

1

1

1

1

1

d

1.5

1.5

1.5

1.5

1.5

1.5

1.5

FV+

3

0

0

1

2

2

4

b ∙ SV+

0

2

0

0

0

0

0

c ∙ EV+

0

0

2

0

0

0

0

d ∙ FV−

0

–1.5

–1.5

0

0

0

0

d ∙ b ∙ SV−

–3

0

0

0

0

–3

–3

d ∙ c ∙ EV−

–22.5

0

0

0

–22.5

–19.5

–22.5

Annual integrated value creation

–22.5

0.5

0.5

1

–20.5

–20.5

–21.5

Improvement

2

2

1

Note: This table shows the value profile of an oil company which has the choice of three projects. The last three columns show the value profile of the oil company after the project (1, 2, or 3). The oil company has equal weights for the value dimensions (b = c = 1), while negative values count 1.5 times (d = 1.5). The annual integrated value creation is obtained by adding the adjusted values in rows 7–12. The improvement is relative to the original company profile in the first column. The top rows show annual value creation by simple adding up of the three values in rows 1–3

The second step is to analyse the projects with regard to the company’s value profile. The last three columns in Table 6.20 illustrate that the extended IPV model would favour selection of project 1 and/or 2, as these projects (partly) repair the value destruction on the social and environmental side. In terms of the value matrix of Chap. 2, the oil company is a quadrant 1 type, value destructive company, which can improve its value profile by doing financially loss-making projects that generate positive impact. The oil company can, for example, select a project from a set of renewables investments to improve its EV and SV profile by varying degrees. Box 6.3 in Sect. 6.4 illustrates the operation of the IPV decision model with a real-world example of Shell, a major oil company.

Table 6.21 provides the details of the investment projects available for the medtech company. The set-up of the projects is identical to those of the oil company. Again, projects 1 and 2 have positive impact on the social side (+2) and the environmental side (+2), respectively, but make financial losses (–1). Project 3 generates a profit (+1) with no externalities. The extended IPV model leads to the selection of project 1, due to the medtech’s healthcare mission with a higher weight for SV (b = 1.6). In this way, the company makes use of the comparative advantage of its purpose (Edmans, 2020).

Table 6.21

Value creation by a medtech company

Value

dimensions/parameters

Medtech company profile

Project 1

Project 2

Project 3

Company after project 1

Company after project 2

Company after project 3

FV

8

–1

–1

1

7

7

9

SV

15

2

0

0

17

15

15

EV

–2

0

2

0

–2

0

–2

Annual value creation by simple adding up

21

1

1

1

22

22

22

Improvement

1

1

1

b

1.6

1.6

1.6

1.6

1.6

1.6

1.6

c

1

1

1

1

1

1

1

d

2

2

2

2

2

2

2

FV+

8

0

0

1

7

7

9

b ∙ SV+

24

3.2

0

0

27.2

24

24

c ∙ EV+

0

0

2

0

0

0

0

d ∙ FV−

0

–2

–2

0

0

0

0

d ∙ b ∙ SV−

0

0

0

0

0

0

0

d ∙ c ∙ EV−

–4

0

0

0

–4

0

–4

Annual integrated value creation

28

1.2

0

1

30.2

31

29

Improvement

2.2

3

1

Note: This table shows the value profile of a medtech company which has the choice of three projects. The last three columns show the value profile of the medtech company after the project (1, 2, or 3). The medtech company has a higher weight for SV (b = 1.6) than for EV (c = 1) and FV (1), while negative values count double (d = 2). The annual integrated value creation is obtained by adding the adjusted values in rows 7–12. The improvement is relative to the original company profile in the first column. The top rows show annual value creation by simple adding up of the three values in rows 1–3

Analysing the projects from perspective of the company’s value creation profile produces a different outcome. Table 6.21 shows that project 2 is selected, as this project repairs the value destruction on the environmental side (integrated value improvement of 3). The second choice is project 1 with the added value coming from the company’s mission (integrated value improvement of 2.2). In terms of the value matrix of Chap. 2, the medtech company is a quadrant 1 company (albeit quite close to quadrant 2), which can improve its value creation profile by doing financially loss-making projects that generate positive impact. With project 2, the company is able to erase its negative environmental value and thus move to quadrant 2.

In contrast, the simple IPV model with adding up sees no difference between the projects, while the net present value rule would select project 3 which has the highest financial value (both on a stand-alone and a company basis).

These case studies show that similar projects can have a different value for different companies and situations. The value depends on a company’s purpose (b, c) and its starting position, where a potential negative value dimension is weighted heavier (d). The extended IPV decision model leads to different investment decisions than both the standard NPV rule (always project 3) and the simple IPV model with a simple adding up of the three value dimensions (indifferent between projects).